Specializing in tax and accounting solutions, Intuit (NASDAQ:INTU) is perhaps best known for its TurboTax software. However, the Internal Revenue Service recently introduced its free tax filing option, which put significant pressure on INTU stock. This move caused concern among investors, fearing the loss of up to one million customers who use the free version of TurboTax. Nonetheless, it appears that investors aren’t looking at the situation three-dimensionally.

It’s understandable why stakeholders would be concerned. Why bother going through a third party when you can file your taxes directly with the source? The company will almost certainly lose its free customers, but so what? Moving forward, that’s not the entrée – that’s not even the appetizer. The real opportunity lies in Intuit’s robust tax preparation services for gig workers, which Wall Street isn’t fully considering. Therefore, I’m taking a contrarian approach and am bullish on INTU stock.

INTU Stock is Likely Down on Optics Rather Than Fundamentals

While the recent drop in INTU stock appears unappealing, that’s really the issue. If you think about it, the narrative against Intuit largely centers on optics rather than fundamentals.

Sure, losing a million customers is never fun. However, the operative word here is “free.” Generally speaking, you get what you pay for. When you’re paying zero dollars, the benefit the underlying service provider accrues largely focuses on brand awareness, higher potential for upselling, and similar dynamics. However, because the price point is zero, it also means that a similarly large entity can potentially disrupt this business model.

In this case, the large entity is the IRS. However, given the trajectory of software tech and the broader momentum of connectivity, it was inevitable that the agency would eventually disrupt Intuit. It looks bad for INTU stock, but again, it’s just the optics. The real meat in this story is the burgeoning gig economy.

According to Business Research Insights, the global gig economy may expand from the valuation of $355 billion reached in 2021 to over $1.86 trillion by 2031. If so, that would imply a compound annual growth rate (CAGR) of 16.18%. It’s possible that the sector could get even bigger.

Fundamentally, the COVID-19 crisis radically shifted the paradigm of how people work – and how they expect to work. However, with more enterprises becoming skeptical about the supposed productivity gains of remote work, return-to-office ultimatums may accelerate the growth of the gig economy, as those who refuse to return back to the office may turn to gig work.

That’s perfect for INTU stock because, guess what? Gig workers, at least in the U.S., are not employees but instead independent contractors. Under this tax category, gig workers are essentially businesses. They must file additional forms along with making quarterly estimated tax payments. They also must keep track of their income and expenses and understand convoluted deduction rules.

It’s a hot mess, and that’s where Intuit will likely shine.

A Relatively Undervalued Investment

Now, however you want to slice and dice it, INTU stock is not undervalued in an objective sense. Right now, the market prices shares at 10.8x trailing-year sales. That’s scorching hot. Intuit falls under the application software sector. This space presently runs an average revenue multiple of 3.8x.

However, forward projections also matter when it comes to the valuation game. Otherwise, you can end up buying a security with a cheap multiple, only to watch it get even cheaper. With INTU stock, it’s difficult to imagine that happening. Again, the underlying gig economy – which should expand Intuit’s addressable market – may expand at a CAGR of 16.18%.

Still, let’s take a look at projected growth for the tax-preparation sector. According to ReportLinker, the global arena may expand from $31.29 billion in 2023 to $38.28 billion by 2027, implying a CAGR of 5.2%. On the high end, Allied Market Research believes the tax advisory ecosystem may expand at a CAGR of 13.2% from 2022 to 2031.

To be sure, various sources will have differing projections, but this gives you a rough idea. For INTU stock, analysts project that Fiscal 2024 revenue will hit $16.18 billion. By 2028, experts are calling for sales of $26.56 billion. In those four years, the CAGR would come out to 12.62%.

On the high side, analysts believe that Intuit’s top line can expand from projected 2024 revenue of $17.1 billion to $29.1 billion. If so, that would imply a CAGR of 14.21%.

So, Intuit should be able to outpace its core market. Further, INTU stock was trading at an average sales multiple of 12.1x during the quarter ended January 31, 2024. It’s not an objectively undervalued play, but it’s relatively discounted.

Is INTU Stock a Buy, According to Analysts?

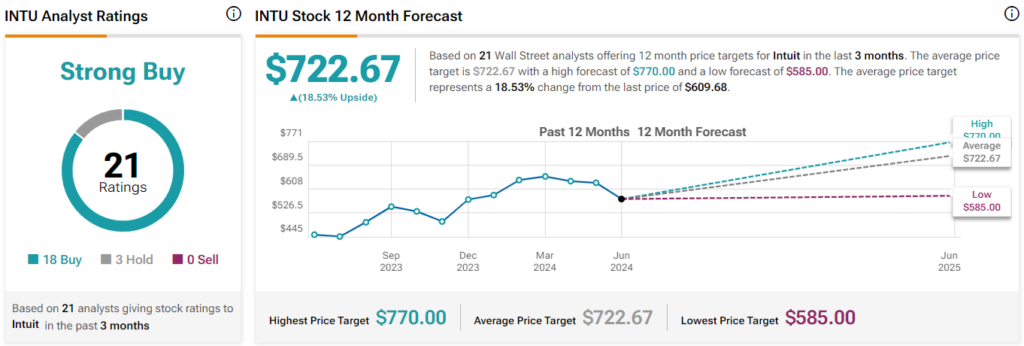

Turning to Wall Street, INTU stock has a Strong Buy consensus rating based on 18 Buys, three Holds, and zero Sell ratings. The average INTU stock price target is $722.67, implying 18.5% upside potential.

The Takeaway: Investors Need to Look at the Bigger Picture

Optically, the present narrative against Intuit doesn’t look good. With the IRS offering a free direct-file program, there seems to be little reason for free users to use Intuit’s TurboTax. However, the burgeoning gig economy should see an increase in paying users. In other words, the sector should expand the software giant’s addressable market. Plus, with the company expected to outpace its core industry, INTU stock seems to be a relatively good deal.