Despite Amazon (AMZN) reaching new highs, I’m still adding to my position. The company’s Q4 results showcased strong retail growth, rising demand for AWS, and a significant surge in free cash flow. With strategic investments in AI-driven technology and a disciplined approach to capital expenditures, Amazon continues strengthening its industry-wide online retail dominance.

AMZN currently has several critical factors fueling the bullish momentum that has seen the stock appreciate 35% in 12 months. With its retail market dominance growing quarter on quarter while its valuation remains attractive, I’m confidently reiterating my bullish rating on AMZN stock.

Retail Division Shines Despite Headwinds

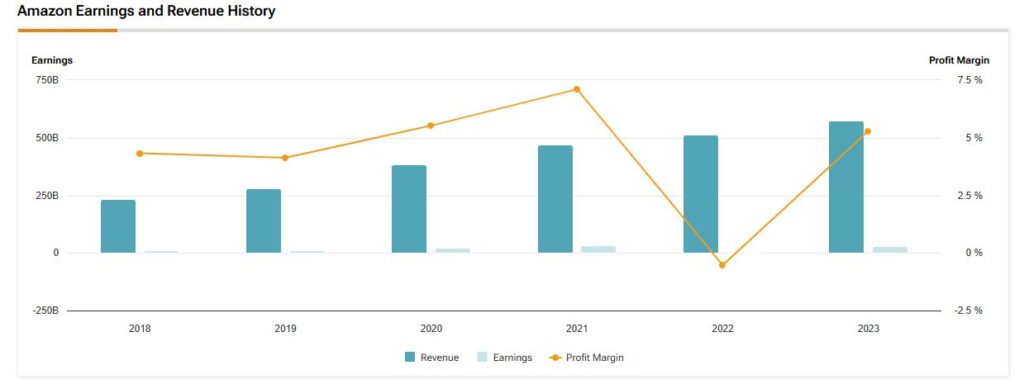

I was especially impressed by how well Amazon’s retail division held up in Q4 2024. North American retail revenue climbed 10% year-over-year to $115.6 billion, while International revenue rose 9% to $43.4 billion. Given persistent inflation and more cautious spending, it’s clear that Amazon still manages to win customers even in more challenging times. That level of strength speaks volumes about the company’s grip on the market, in my view.

I’ve also noticed that Amazon’s meticulous focus on cost efficiency has begun paying off significantly. The North American segment’s operating margin rose to 8% from 6.1% a year ago. Meanwhile, the International segment swung from an operating loss of $0.4 billion in Q4 2023 to a profitable $1.3 billion this quarter. This positive development can be attributed to better inventory placement and an expanded network of same-day delivery sites, among other factors, driving tangible margin gains.

Moreover, it was impressive to see Amazon fulfilling more than 9 billion orders with same-day or next-day shipping in 2024 alone. That focus on speed helps lower per-unit costs while strengthening customer loyalty. As Amazon continues refining its fulfillment network, I expect it to become an even bigger part of people’s daily shopping habits. That kind of convenience and efficiency should keep boosting top-line retail growth for the foreseeable future.

AWS Powers Continued Expansion

Amazon Web Services (AWS) remains the leading growth engine for AMZN, even as the broader cloud computing market becomes increasingly competitive. In Q4, AWS revenue jumped 19% year-over-year to $28.8 billion, fueled by the ongoing enterprise shift to cloud solutions and the surging demand for AI-driven services.

But besides its impressive top-line growth, I found the segment’s ever-improving profitability much more interesting. AWS’s operating income surged to $10.6 billion from $7.2 billion a year ago, with expanded margins partly stemming from investments in proprietary AI infrastructure. For example, AWS Trainium2 chips offer both cost efficiencies and enhanced performance, solidifying the company’s advantage in AI-powered cloud services at a massive scale.

AWS has also developed its generative AI portfolio, rolling out new features like Amazon Bedrock’s wider foundation models and the AI-driven developer assistant, Amazon Q. It’s still a bit early to tell, but I think these new initiatives make it clear that Amazon is serious about being in the mix on cloud innovation, even as competitors step up their game. In fact, with AWS zeroing in on specialized AI tools, I can see it maintaining its lead in established enterprise markets and the rapidly evolving AI space.

Profitability and Free Cash Flow Soar

Building on AWS’ improving profitability, Amazon’s consolidated operating income soared to a record $21.2 billion in the recent quarter, a 61% increase from last year. Net income nearly doubled to $20 billion ($1.86 per share), compared to $10.6 billion ($1.00 per share) a year ago.

During the same period, trailing 12-month free cash flow reached $36.2 billion, pointing to disciplined spending and a sharp focus on efficiency. This influx of capital puts Amazon in a great spot to keep investing in infrastructure, AI, and fulfillment automation. I’m especially intrigued by how their robotics strategy is playing out on the ground, as shown by the improvements at the Shreveport facility, something management emphasized during AMZN’s earnings call.

AMZN Valuation Entices Investors

Even following the stock’s prolonged rally over the past year, Amazon’s valuation seems compelling given its medium-term free cash flow outlook. Supported by continued top-line growth and widening margins, Amazon will surpass $100 billion in free cash flow by 2027. Evidently, Wall Street analysts project a free cash flow of $53.4 billion, $81.9 billion, and $115.5 billion for FY2025, FY2026, and FY2027, respectively. The AMZN gravy train keeps on rolling.

These estimates translate to P/FCF multiples of 45.5x for FY2024, 29.6x for FY2026, and 21.1x for FY2027. Considering Amazon’s dominant position in retail and cloud, these multiples suggest the stock is on track to grow comfortably into these multiples. From another perspective, Amazon’s forward P/E ratio of 36.5x marks one of its lowest valuations since 2010. This aspect and a projected five-year EPS CAGR of 21.7% reinforce my view that Amazon still has plenty of runway for long-term growth.

What is Amazon’s Stock Prediction for 2025?

Despite Amazon’s extended rally, Wall Street maintains a Strong Buy consensus rating on Amazon. This is based on 45 Buy, one Hold, and zero Sell ratings assigned over the past three months. Currently, AMZN stock carries a price target of $268.71 per share, which indicates a 15% upside potential.

Notably, since AMZN published its Q4 results, five analysts have reiterated their Buy ratings, with each analyst expecting double-digit growth in AMZN stock in 2025:

AMZN Climb Has Further Upside

From vigorous retail fundamentals and robust AWS growth to sustained free cash flow expansion and attractive valuation, Amazon stands out as a market leader well-positioned for continued success. I remain confident in AMZN as a long-term investment, even at elevated share prices. Its resilience, persistent AI innovations, and reliable profitability profile highlight a company at the forefront of the tech and e-commerce landscape with extensive potential upside in 2025.

Questions or Comments about the article? Write to editor@tipranks.com