Mobileye Global’s (MBLY) stock has been climbing since yesterday when it announced a partnership with Valeo (VLEEY) and Volkswagen Group (VWAGY). According to a joint statement, the collaboration seeks to integrate Mobileye’s Surround ADAS platform with Valeo’s sensor technology into a single, unified system for Volkswagen’s next-generation vehicles.

By consolidating multiple ECUs, MBLY’s approach enhances efficiency, improves system performance, and enables over-the-air updates to meet evolving safety standards. The Israel-based tech company is best known for its advanced driver-assistance systems, which are standard in new cars. Mobileye’s EyeQ system also provides ADAS capabilities by processing data from other sensors and cameras.

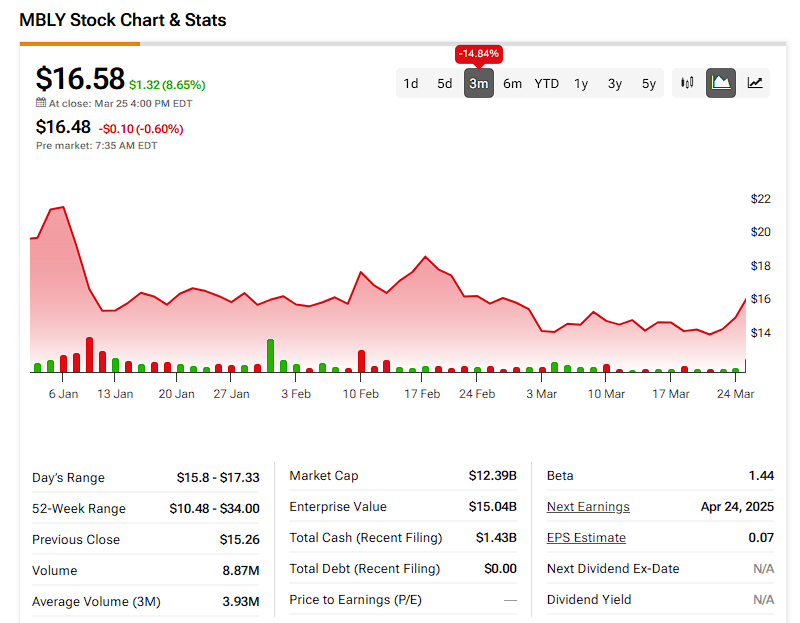

Volkswagen is one of the largest global automobile makers, and its upcoming vehicle portfolio will now feature Mobileye’s ADAS. In response to the news, Mobileye’s stock perked up 9%. However, upon closer inspection, while the collaboration is a breath of fresh air for Mobileye, it may not be enough to lift it out of the smog that has enveloped its 2025 so far, leaving me bearish on the stock.

ADAS Market Growth Encounters Intense Competition

The global advanced driver-assistance systems (ADAS) market is expected to grow at a CAGR of 12.2% to reach $68 billion by 2030, with two significant tailwinds driving the market. For starters, ADAS, including features like blind spot monitoring and automatic emergency braking, once considered a luxury, are becoming standard features in cars.

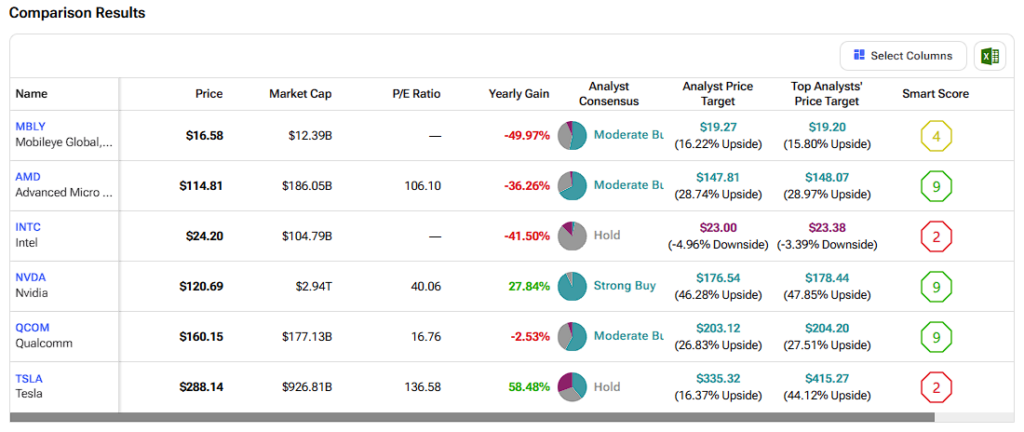

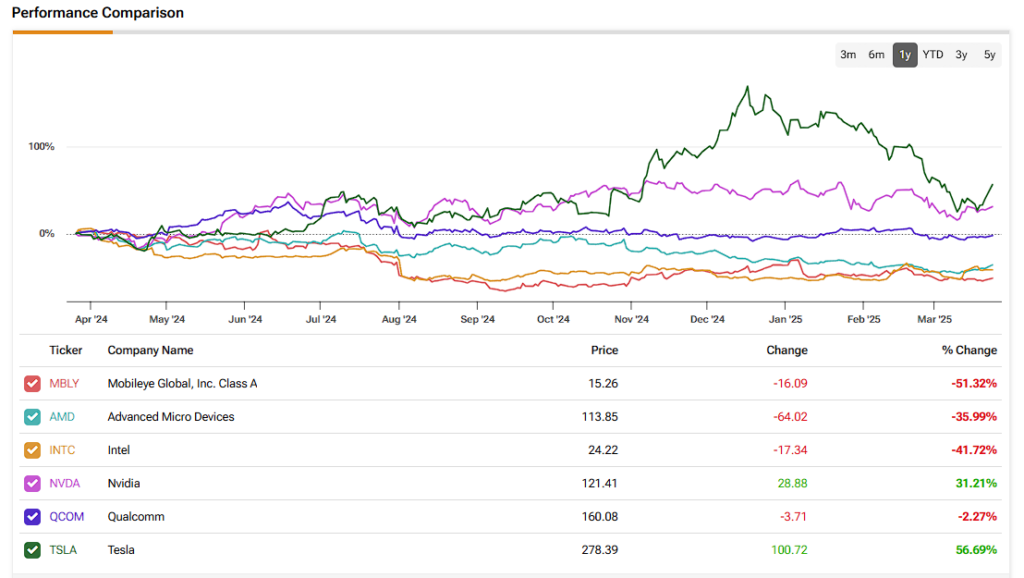

Second, the advent of autonomous vehicles has spurred interest and innovation in safety features. While Mobileye is a recognized leader in this space but not alone. Some car manufacturers (OEMs), like Tesla (TSLA), feature in-house manufactured ADAS. Semiconductor giant NVIDIA (NVDA) offers its own ADAS system too. In fact, just days ago, NVIDIA announced a collaboration with General Motors (GM). Finally, other startups focus on ADAS, including Phantom AI and Wayve.

Q4 Performance Shows Revenue Decline and Margin Pressures

Despite this growing market, Mobileye’s revenues are shrinking. In the fourth quarter of 2024, the company reported revenue of $490 million, a 23% year-over-year decrease.

While Mobileye outperformed adjusted EPS estimates, the considerable drop in revenue and gross margins (54% in Q4 2023 to 49% in Q4 2024) worried the market. The company attributed the results to a “meaningful build-up of inventory of our Tier 1 customers.” Although sporting consistent annual net losses, Mobileye’s balance sheet is extraordinarily asset-heavy, enabling strategic flexibility.

Navigating Customer Concentrations and Technological Challenges

Mobileye’s revenue guidance of between $1.69 billion and $1.81 billion for 2025 can be described as conservative. During the Q4 2024 earnings call, the company stated that its guidance accounts for the possibility that Zeekr, a China-based car manufacturer, might opt for in-house ADAS for its Zeekr 9 model. This follows Zeekr’s 2024 decision to use an in-house system over Mobileye’s SuperVision for its 001 model.

This trend makes financial sense for car manufacturers because it gives them control over the technology and lowers the long-term cost. However, not all car manufacturers are taking this route. Volkswagen is a prime example. Although it is developing its own automated driving technologies (CARIAD), it still collaborates with Valeo and Mobileye for specific ADAS functionalities.

Keep in mind that Mobileye generates most of its revenue from selling EyeQ to OEMs through sales to Tier 1 automotive suppliers (they provide OEMs with significant prefabricated components or systems). Mobileye recognizes its revenues upon shipment, which explains why its revenues are at the mercy of inventory adjustments. In 2024, Mobileye’s top four customers accounted for 74% of total revenue. So, there are significant customer concentration risks to consider as well. If any OEM cuts just one major Tier 1 customer of Mobileye’s, it could result in material revenue loss.

Is MBLY a Good Buy?

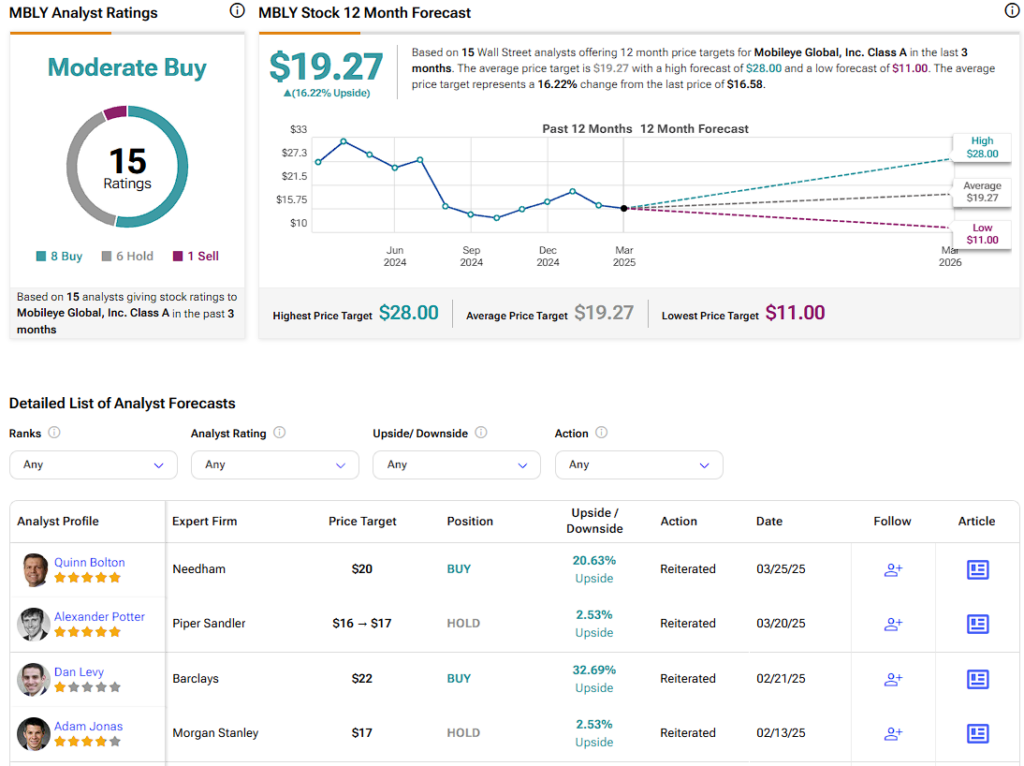

MBLY has a Moderate Buy consensus rating on Wall Street based on eight Buy, six Hold, and one Sell ratings over the past three months. MBLY’s average price target of $19.27 per share implies a 16% upside from its current price.

Analyst expectations softened a bit following Mobileye’s Q4 earnings. For instance, Vijay Rakesh from Mizuho Securities maintained a Hold rating on MBLY but lowered his price target from $17 to $16 per share. Overall, while Wall Street appears more bullish than I am, its increased caution to begin the year echoes my sentiments. Mobileye’s weaknesses and threats (i.e., competition, customer concentration, and inventory adjustments) are rearing their heads.

MBLY Technology Clashes With Market Uncertainty

While the Volkswagen collaboration signals that Mobileye’s ADAS is still in demand, the numbers suggest that the demand, although there, is slowing. The market opportunity is promising but is currently jam-packed with competition, including OEMs embracing vertical integration.

Beyond OEMs, the competition, such as NVIDIA, is formidable, and Mobileye may be unable to innovate at the pace needed to stay ahead in this market. Technology evolves fast, and what is relevant today may become obsolete tomorrow. Granted, Mobileye is making progress in the autonomous vehicle landscape. For instance, the deal with Lyft to introduce “Mobileye Drive equipped, Lyft-ready” taxi fleets in the near future rings with great promise.

However, I suspect that the reality, especially in the early years, may be quite different, with regulatory hurdles, infrastructure readiness, the speed of deployment, competition, and public acceptance all figuring as potential risk catalysts. Given all these factors, I lean bearish on MBLY stock despite the Volkswagen partnership and its speculative position within the autonomous vehicle space.