Vodafone Group announced an offer to buy out all of Kabel Deutschland Holding’s (KDG) minority shareholders for about €2.1 billion ($2.5 billion), which would put an end to a lengthy legal battle.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Specifically, Vodafone (VOD) will offer Kabel Deutschland shareholders €103 for each outstanding share. Following the completion of the offer, the British telecom operator will own at least 93.8% of the outstanding share capital of Kabel Deutschland. The cash consideration for the buyout will be funded from Vodafone’s existing cash resources, the company said.

Vodafone said that minority shareholders, representing about 17.1% of Kabel Deutschland’s share capital, had already accepted the offer. Among the shareholders are activist hedge fund Elliott Advisers (UK) Limited and UBS O’Connor LLC. Back in 2013, Vodafone bought a 76.8% stake in the German cable company via a voluntary public takeover offer.

Kabel Deutschland minority shareholders, including Elliott, appealed against a 2019 decision by a German court, which ruled that the mandatory cash offer made by Vodafone to minority shareholders in the takeover was adequate.

“As a result of the agreement to tender their shares in KDG [Kabel Deutschland] to Vodafone, the accepting shareholders will withdraw their appeal from the court of appeal in Munich. Elliott has also agreed to certain confidentiality and other restrictions, including commitments not to take further legal action against Vodafone,” according to the Vodafone statement.

Vodafone said that if all KDG minority stockholders tender their shares, the company’s reported net debt as of September 30, 2020 would increase from €44 billion to €46.1 billion. However, the offer is not expected to impact its current credit ratings, the company said. (See VOD stock analysis on TipRanks)

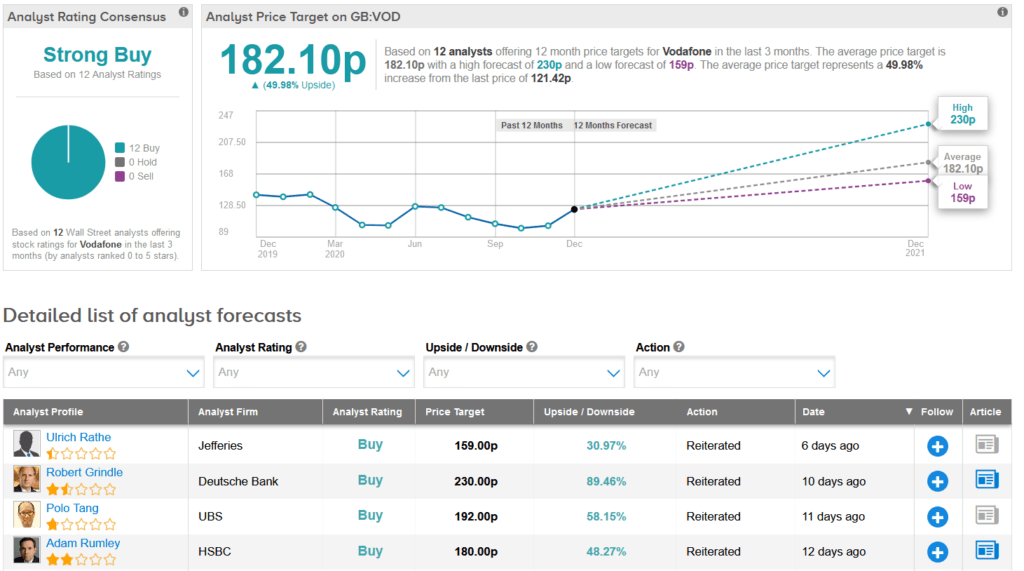

On Dec. 10, HSBC analyst Adam Rumley lifted the stock’s price target to 180p from 177p and maintained a Buy rating. Rumley is optimistic as service revenues are showing resilience in the face of COVID-19 pressures and believes operations and cost savings remain well on track.

The rest of the Street is firmly in line with Rumley’s bullish outlook. The Strong Buy analyst consensus boasts 12 back-to-back Buy ratings. Meanwhile, the average price target stands at 182.10p and implies 50% upside potential over the coming year.

Related News:

Beacon to Divest Interior Products Business to American Securities for $850M

Apple Sets 2024 Target For Vehicle Production – Report

ConocoPhillips Announces New Oil Discovery; Street Sees 25% Upside