VMware reported better-than-expected 2Q results on Thursday driven by strong sales of Subscription and SaaS products as organizations accelerated their cloud plans amid the COVID-19 pandemic.

VMware’s (VMW) 2Q revenues increased 9% to $2.88 billion and surpassed analysts’ expectations of $2.8 billion. Its adjusted EPS grew 18% to $1.81 year-over-year and beat Street estimates of $1.45. The enterprise cloud company’s Subscription and SaaS division’s revenues climbed 44% year-over-year and accounted for 22% of the total revenue.

VMware CEO Zane Rowe stated that “We plan to accelerate certain product initiatives through the remainder of the year, which will further support customers’ digital transformations and grow our Subscription and SaaS product offerings.” (See VMW stock analysis on TipRanks).

Ahead of its earnings, on August 24, Monness analyst Brian White reiterated his Hold rating on the stock and expected that the company would meet his revenue and earnings expectations. White said, “With this crisis driving accelerated digital transformation initiatives, we expect the next-gen pieces of VMware’s portfolio to benefit from this phenomenon.”

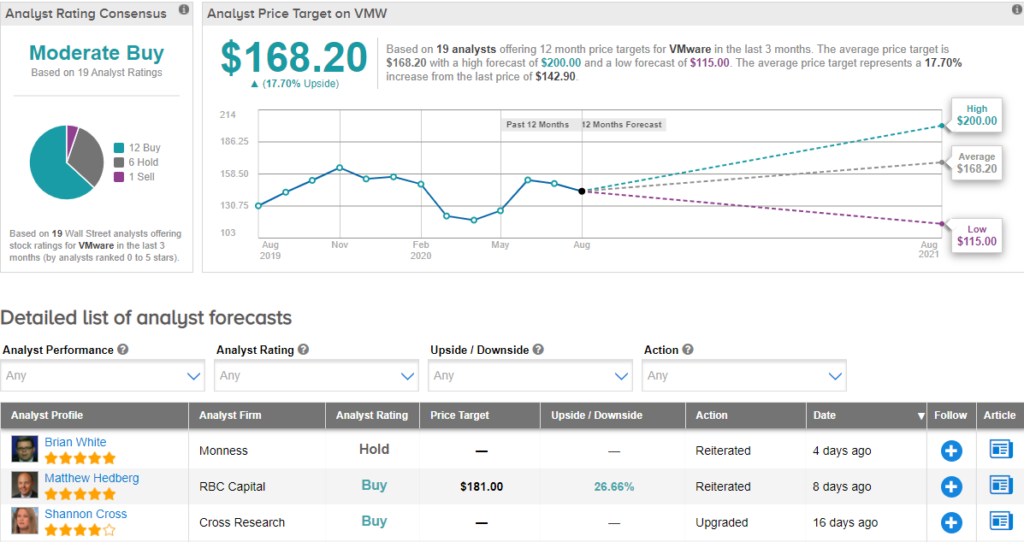

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 12 Buy, 6 Holds, and 1 Sell. With shares down about 6% year-to-date, the average price target of $168.20 implies an upside potential of about 17.7% to current levels.

Related News:

Oppenheimer Lifts Marvell’s PT Ahead Of 2Q Earnings

BMO Lowers Palo Alto’s PT After 4Q Beats Estimates

NetApp Leaps 11% In After-Hours On Strong 1Q Results