Visa (V) delivered excellent quarterly results last week, closing Fiscal 2024 with accelerated revenue and EBITDA growth driven by higher consumer spending and ongoing international expansion. The company also aggressively ramped up its share repurchases, with the pace of buybacks picking up considerably of late. I believe that these two catalysts indicate upside potential for the payments giant at its current price levels and support a bullish outlook on Visa’s stock even as it trades at all-time highs.

Visa’s Accelerating Revenue and EBITDA Growth

One of the most compelling highlights from Visa’s fiscal Q4 results—and a key driver behind my bullish outlook on the stock—is its accelerating revenue growth. Visa’s top-line growth hit 11.7%, up from 9.6% in the previous quarter and 10.6% in the same period last year. This rise was driven by robust consumer spending and expansion in new markets.

Specifically, payments volume grew by 8%, with a substantial contribution from cross-border transactions, which rose 13%, excluding intra-European activity. Moreover, Visa’s CEO, Ryan McInerney, highlighted the company’s focus on expanding its consumer payment offerings and growth within non-consumer payments, driving global adoption, especially during major events like the Summer Olympics. Another instance I found interesting is that Visa renewed a critical partnership with Cantaloupe (a leading provider of self-service commerce), which should add significant new transaction potential and strengthen Visa’s foothold in the automated retail sector.

Visa’s EBITDA growth was similarly strong, rising 11.9% year-over-year, representing an acceleration from the prior quarter’s 8.7% growth rate and last year’s 11.5%. This was driven not only by increased revenue but also by mindful cost management, as operating costs rose by a below-revenue growth rate of 7%. The absence of provision for litigation expenses from last year also boosted this figure. Simultaneously, this was another period of Visa flexing its ability to maintain incredible margins, with its operating margin expanding by 15 basis points year-over-year to a highly impressive 66.12%.

Surging Buybacks Reflect Management’s Confidence

Another notable bullish catalyst for Visa recently has been its surge in share buybacks, which I believe signals management’s enthusiasm for the company’s future prospects relative to the stock’s present valuation. In Fiscal Q4 alone, Visa repurchased a record $5.8 billion worth of shares, totaling $16.7 billion for the year. This marks a considerable increase from the $11.6 billion and $12.1 billion repurchased in Fiscal 2022 and 2023, respectively. The rise in repurchases likely reflects Visa’s revenue acceleration, supporting a positive outlook for its long-term growth.

Considering the company’s current valuation at about 26 times the consensus EPS of $11.20 for Fiscal 2025, I believe today’s repurchases will likely prove to be highly accretive, benefiting shareholders as Visa’s EPS continues to snowball.

Key Drivers for Future Growth

To further explore Visa’s future growth potential backing this thesis, note that the company is leveraging several strategic initiatives aimed at boosting its expansion beyond organic growth drivers like increased consumer spending and inflation, which naturally drive its net revenue over time. One such catalyst is Visa’s focus on expanding new payment flows, especially through Visa Direct, which registered a 38% year-over-year transaction growth during Fiscal Q4. In fact, Visa Direct continues to gain global traction across various industries, including remittances and business-to-business (B2B) payments.

In addition, Visa is aggressively investing in value-added services such as advisory and fraud prevention, which I reckon have deepened existing client relationships and attracted new partners, growing its service ecosystem. Finally, another meaningful growth driver I think is worth mentioning is the rise in cross-border transactions. Earlier, I mentioned that cross-border transactions increased by 13% in Fiscal Q4, and given that global tourism levels continue to hit new records by the quarter, I believe this to be a notable growth catalyst in the coming years—especially since Visa collects above-average fees for such transactions.

Wall Street anticipates that Visa’s EPS will grow at a compound annual growth rate (CAGR) of 11.8% over the next five years, driven by a combination of organic expansion and strategic acquisitions. This outlook aligns well with management’s decision to ramp up buybacks today—a catalyst that bolsters my bullish outlook on the stock.

Is Visa Stock a Buy?

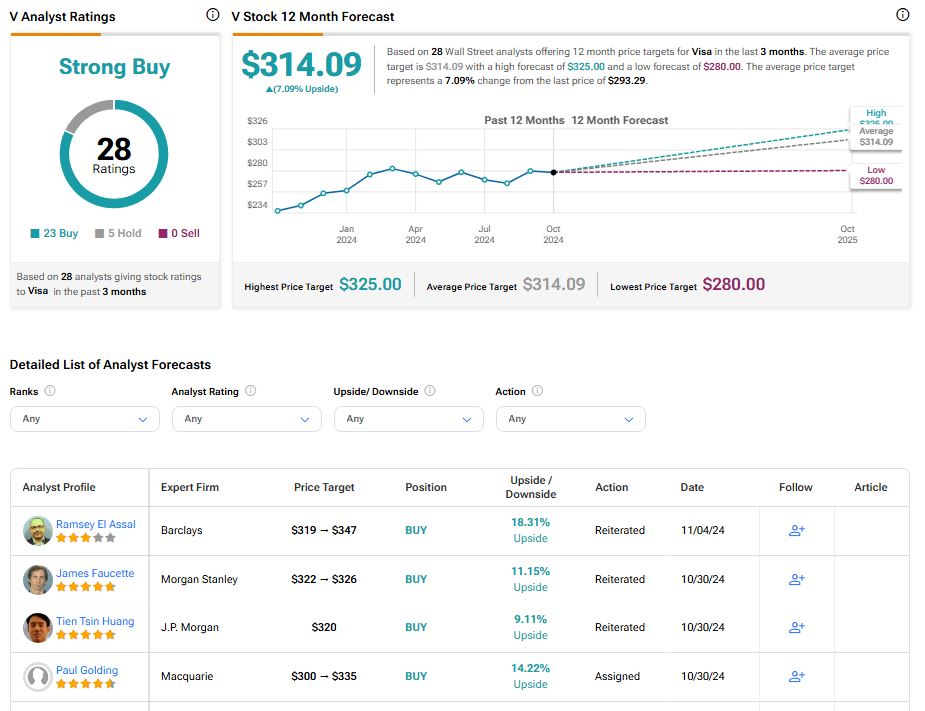

Looking at Wall Street’s view on Visa, the stock features a Strong Buy consensus rating based on 23 Buys and five Holds assigned in the past three months. At $314.09, the average Visa stock price target suggests 7.09% upside potential.

If you have yet to choose which analyst you should trust if you want to trade Visa stock, consider Sanjay Sakhrani from KBW. He stands out as the most accurate and profitable analyst covering this stock over a one-year timeframe, delivering an impressive average return of 19.40% per rating with a flawless 100% success rate.

Conclusion

Summing up, Visa’s accelerating revenue growth, EBITDA growth, and aggressive buyback strategy signal strong future prospects for the payment giant. With consumer spending, cross-border transactions, and Visa Direct driving significant gains, I believe the company is well-positioned for sustained double-digit EPS growth, which aligns with Wall Street’s medium-term estimates. Along with continued investments in value-added services and international partnerships, I view Visa’s current valuation as a solid foundation for future upside.