Visa Inc. has made a strategic investment in UK payments issuer processor Global Processing Services (GPS). Financial terms of the deal weren’t disclosed.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Visa’s (V) strategic investment is intended to boost GPS’ global expansion, following its launch of new and innovative fintechs and digital banks in Europe and South East Asia, including Revolut and Starling Bank. As an issuer processor GPS supports fintechs, digital banks and e-wallet providers on their growth journey. Following the investment, GPS, which is also backed by UK growth private equity firm, Dunedin, will be one of Visa’s preferred processors globally.

“GPS is an example of how we continue to invest in, and partner with, companies that provide valuable capabilities to the ecosystem and have potential to advance the payments industry,” said Kevin Jacques at Visa Ventures. “The business has a strong balance sheet, engaging leadership and growth across key regions, and we believe it will continue to be an important enabler for payments processing.”

GPS is certified by Visa and Mastercard to process and manage any credit, debit or prepaid card transaction globally. Visa is a global payments industry leader with a vast presence in over 200 countries.

In recent months, Visa has been entering into strategic partnerships to expand in key growth areas. It has partnered with UK-based fintech Conferma Pay to integrate Visa virtual cards in the Conferma Pay mobile app. The collaboration will allow companies to provide virtual Visa commercial cards to employees’ digital wallets, enabling tap-to-pay and simplify expense reimbursement. In January, Visa announced a $5.3 billion agreement to acquire fintech Plaid, which has products that enable consumers to share their financial information with many apps and services such as Acorns, Betterment, Chime, Transferwise and Venmo.

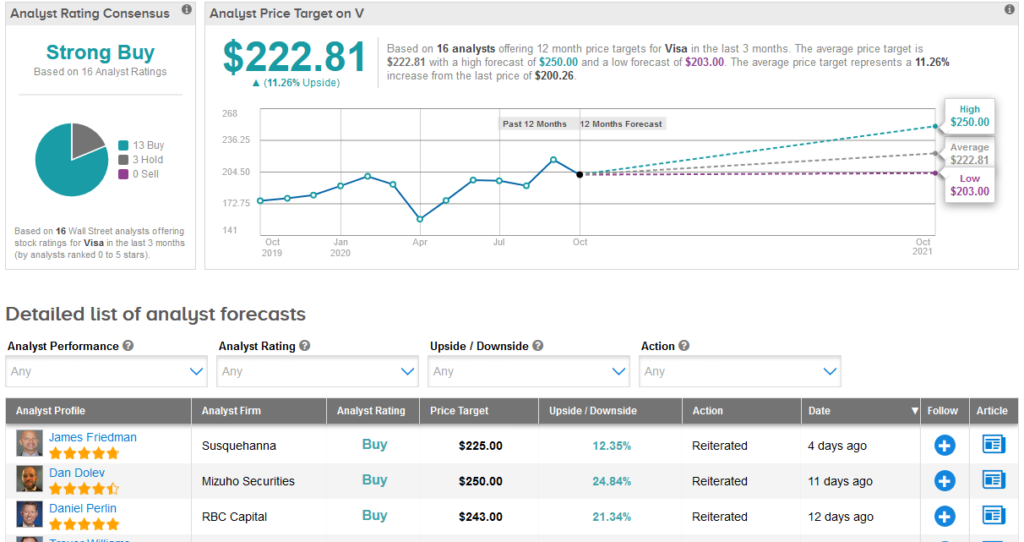

Mizuho Securities analyst Dan Dolev this month reiterated a Buy rating on the stock and his Street High $250 price target (25% upside potential), saying that a travel comeback in 2021 could boost EPS by as much as 10%.

“Although exact timing is unpredictable, our proprietary online travel agency tracker may offer a silver lining, pointing to a modest positive inflection in search trends for prominent travel websites in late September & early October,” Dolev wrote in a note to investors. “Assuming 25-75% of lost 2020 travel volume returns in 2021, this could translate into approximately 5-10% further EPS growth for Visa.” (See V stock analysis on TipRanks)

The rest of Street has a bullish outlook on the stock. The Strong Buy analyst consensus breaks down into 13 Buys and 3 Holds. With shares up 6.6% this year, the average analyst price target of $222.81 implies upside potential of another 11% over the coming year.

Related News:

Uber Seeks ‘Strategic Alternatives’ For Elevate Biz- Report

GTT In $2.15B Deal To Sell Infrastructure Unit To I Squared; Shares Up 7%

First Citizens, CIT To Merge Into $100B US Regional Lender; Shares Spike