Verizon (VZ) recently released its third-quarter earnings report, which hasn’t moved the needle much stock price-wise (though it did slightly decline) but generally impressed and satisfied its shareholders. It beat most metric estimates, including Revenue, EPS, and EBITDA margins. The report arrived after VZ stock had done well over the past year, climbing 23.41%. This comes after a rough few years where its stock declined, with the company losing market share to competitors such as AT&T (T) and T-Mobile (TMUS). It also failed miserably when it tried to raise its prices to cover the growing costs, which didn’t go well in terms of retaining its customers.

Additionally, VZ has a huge debt lingering over its shoulders, $169 billion as of now, which puts the company’s future margins in doubt. Nevertheless, the company has deleveraged its debt, and it looks like it is moving in the right direction and has regained its groove – so much so that Tipranks’ Smart Score is giving it a “Perfect 10” rating.

If you wish to read more extensively on Verizon, you can check what Nikolaos Sismanis, our writer at Tipranks, has written about it right here.

For now, though, let’s see what Verizon has done well in the last quarter:

- Verizon’s Q3 Performance and Stock Reaction: Verizon’s stock took a hit after its Q3 earnings report, dipping 7.7% below its 52-week high. Despite this, the stock has remained at 23.41% over the past year. This minor decrease in the stock’s value seems more like a breather after a long rally than a reaction to poor performance. The Q3 results were solid overall, with revenues steady at $33.3 billion and adjusted EBITDA increased by 2.1% reaching $12.5 billion.

- Wireless Services Growth and Customer Acquisition: Verizon’s wireless service revenue increased 2.7% year-over-year, reaching a record $19.8 billion. This growth was fueled by the addition of 81,000 retail postpaid phone customers in the consumer segment and 158,000 in the business segment. Overall, total wireless retail postpaid phone gross adds grew by 5.1% year-over-year to 2.7 million, showcasing Verizon’s ability to attract and retain customers.

- Profitability, Deleveraging, and Dividend Growth: Verizon’s adjusted EBITDA margin improved to 37.5%, up from 36.5% in the same quarter last year. Despite a 16.7% rise in interest expenses, adjusted EPS was $1.19, down 2.5% from the previous year. The company continued to deleverage, reducing net debt to $169.2 billion from $175.8 billion in the previous quarter. Additionally, Verizon increased its dividend by 1.9%, marking a 20-year streak of annual dividend increases, with a current yield of 6.02%.

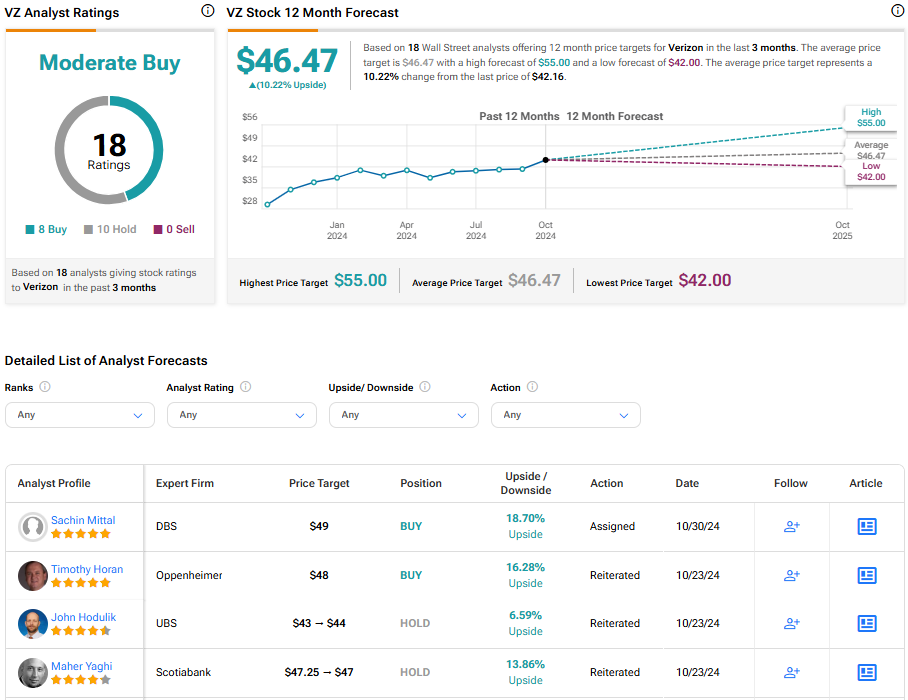

What Is the Price Target for VZ?

According to analysts, Verizon is a Moderate Buy, with Eight Buys, Ten Holds, and Zero Sells. The average price target for VZ stock is $46.47, reflecting 10.22% upside.

Summary

Verizon has had a rough few years, with its stock suffering as a consequence, but in recent years, the company has shored things up and seems to have regained its groove. After VZ’s encouraging Q3 results, the stock reacted slightly negatively, but it doesn’t look like anything related to its operations. In addition, the company has started to deleverage its huge debt and even increased its dividend payments, reflecting its management’s faith in its financial strength.