Verizon (VZ) and AT&T (T) are the two leading telecom companies in the U.S., yet only one stands out as a prudent dividend-seeking investment at today’s market prices. While both share many similarities, from their target markets to their financial and business models, their individual share performance has been starkly different over the past twelve months. Still, I remain bullish on both these telecoms giants as Q4 earnings season looms. Since the devil is always in the details, in this article, I’ll explain why, upon closer inspection, Verizon may be the best pound-for-pound dividend stock in telecoms right now.

VZ & T Are Two Dividend Titans Battling for Yield

As Verizon and AT&T’s bullish thesis is strongly linked to dividends, Verizon currently poses a more enticing dividend yield than AT&T. For dividend-focused investors, many consider the yield to be the most important number to track. After all, the ratio determines how much the investor can crystallize into profit relative to the stock’s current price. However, a strong dividend yield is useless if the stock isn’t providing good capital returns.

As we can see in the chart above, Verizon offers a yield of almost 7%, while AT&T yields just over 5%. Both yields are pretty enticing, especially compared to the core PCE inflation rate, which is currently at 2.8%. However, when you look at the stock performance over the last twelve months, Verizon shares rose modestly ~5%, significantly underperforming the broad market, while AT&T shares jumped ~42% higher. So, as the dividend yield is calculated by dividing the dividend per share by the stock price—the higher the stock price, the lower the yield tends to be.

That said, since 2022, Verizon has increased its annual dividend by 4 cents per year, from $2.57 in 2022 to $2.65 in 2024. Meanwhile, AT&T has kept its dividend flat at $1.08 per share since 2023, a significant decline compared to the $2.08 per share it paid out in 2021. All else being equal, investors are generally better off owning stock in a company capable of growing its dividend payments over time, especially when dividend yields outperform inflation—and Verizon seems to be doing exactly that.

Both AT&T and Verizon Demonstrate Long-Term Dividend Reliability

Since dividend investing is all about the long term, figuring out how sustainable the dividend payments are is essential. In this respect, both Verizon and AT&T have outperformed, which is a further reason why I’m bullish on both stocks.

Verizon has paid out about ~59% of its profits over the past twelve months, while AT&T has distributed less than 50%. As mature companies, neither Verizon nor AT&T is expected to see strong growth in revenue or earnings. Verizon is projected to grow EPS at a CAGR of 2.2% over the next three to five years, while AT&T is looking at a much slower EPS CAGR of just 0.6%. As a simple hypothetical, assuming no share price or interest rate change for the next five years, Verizon would be on target to generate a yield of 7.9%, while AT&T would be expected to fetch 5.1% by 2030.

Analyzing the Sustainability of Verizon and AT&T’s Dividends

Moving on to other metrics that better reflect the sustainability of Verizon and AT&T’s dividends, let’s take a closer look at cash flow generation and balance sheets.

In 2024, Verizon generated $13.83 billion in free cash flow, a decent improvement from $12.91 billion in 2023, though still well short of the $19.68 billion it posted in 2019. The company’s free cash flow over the last twelve months was around 24% higher than paid dividends.

AT&T tells a slightly different story. Although its free cash flow over the past twelve months peaked at just over $20 billion (marginally lower than 2023), it was still more than double the $8.2 billion paid out in dividends. The balance sheet shows Verizon’s net debt of $173.35 billion, representing 45% of its total assets, while AT&T’s is tangibly stronger with $145.35 billion in net debt, which tallies to 37% of its total assets.

While AT&T might appear to have the edge on the balance sheet, I don’t consider the difference to be particularly significant. Much like with AT&T, Verizon’s dividend coverage and balance sheet will be sufficiently solid to support further dividend yield growth.

Verizon & AT&T’s Q4 Earnings Date Approaches Soon

Heading into earnings season, Verizon and AT&T are scheduled to report their Q4 earnings results on the 24th and 27th of January, respectively.

Analysts expect Verizon to report an EPS of $1.09, implying a 1.5% year-on-year growth rate combined with revenues of $35.33 billion, a modest 0.5% increase. For AT&T, market analysts expect an EPS of $0.51, implying a 6.5% decrease year-on-year, backed by revenues of almost $32 billion — a 0.2% downtick. Besides topping estimates, market consensus suggests the main topic of conversation on earnings day will likely be cash flows.

Verizon, while not providing free cash flow guidance, reported Q3 free cash flow from operations of $6 billion, with CapEx at $4 billion. Assuming CapEx and other expenditures range from $4.0 to $4.5 billion (in line with the company’s guidance), I expect Verizon to post free cash flow figures of between $4.5 and $5.0 billion for Q4. Such a print would cover the $2.8 billion required for dividend payments and, in my opinion, would be enough to keep bullish sentiment intact for the medium-long term.

According to regulatory filings and company performance metrics published by AT&T, the telecoms giant expects to post free cash flow of around $17.5 billion for the past financial year, having already reported $12.8 billion in the first three quarters of 2024. Basic arithmetic suggests AT&T expects to lock in somewhere between $4.2 and $5.2 billion in free cash flow when it reports its Q4 2024 figures later this month.

Irrespective of what Verizon and AT&T report later this month, expect a significant increase in market volatility, and if results happen to undershoot analyst expectations, market bulls could look to initiate medium-long term positions at discounted prices as short-term market participants miss the bigger dividend picture behind these two telecoms giants.

Is Verizon Stock a Buy, Sell, or Hold?

At TipRanks, Verizon (VZ) is rated as a Moderate Buy based on five bullish and nine neutral analysts. Importantly, not a single market analyst recommends selling Verizon stock, and neither do I. Currently, the stock carries an average VZ price target of $46 per share, implying almost 20% upside potential compared to current prices.

Is AT&T a Buy, Sell, or Hold?

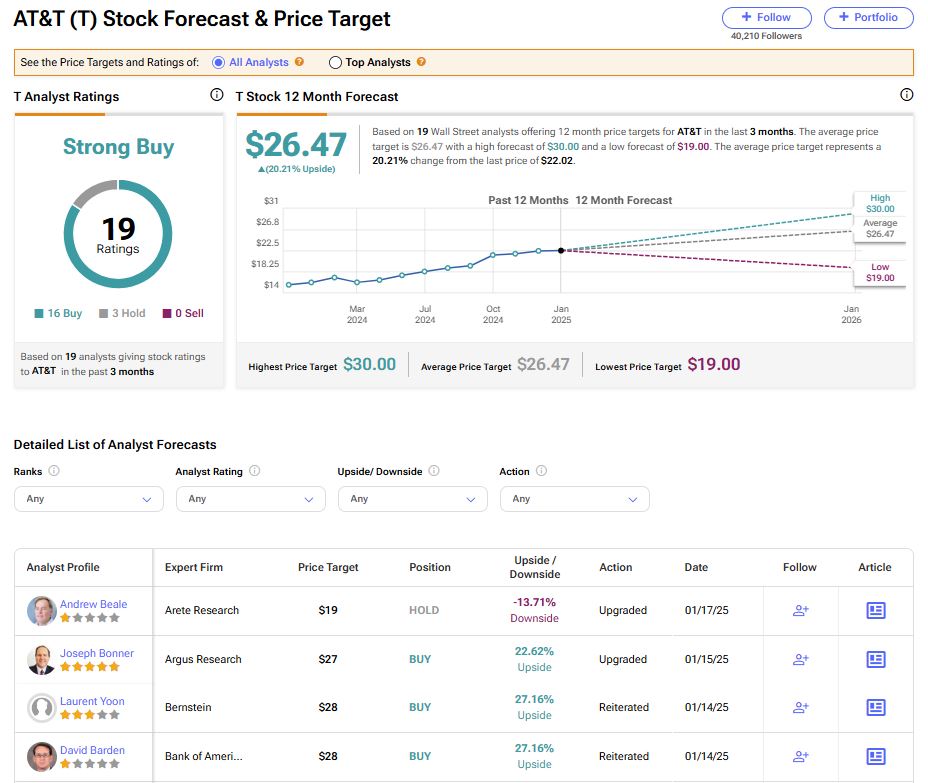

Meanwhile, AT&T is rated as a Strong Buy, based on 19 bullish analysts and just three on the fence. Similarly to Verizon, not a single analyst recommends selling AT&T right now while carrying an average T price target of $26.47 per share, representing more than 20% upside potential.

Key Takeaway

While both Verizon and AT&T are great dividend stocks for any dividend-seeking portfolio, I believe Verizon stands out as a better buy, given current factors. To back up this point, despite having a higher payout, Verizon has been able to grow its dividend without putting its sustainability at risk—while AT&T has the edge over its competitor in terms of financial prudence.

If you have your eye on either of these telecom titans, mark the last week of January in your diaries. Their Q4 performance results could shake up the short-term picture while providing medium-long-term positional opportunities for yield-hungry dividend hunters. Whoever wins this battle may not win the war.