Verano Holdings (VRNO) announced strong first-quarter financial results on Tuesday. The report included the acquisition of AltMed using pro format consolidated basis accounting as if completed on January 1, 2021. Verano is a U.S. multi-state cannabis operator based in Chicago with a portfolio encompassing 14 states.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Verano’s revenue came in at $143 million for the quarter ended March 31, an increase of 117% year-on-year. Net income amounted to $126 million in Q1 2021, compared to a net income of $72 million in Q1 2020. The net income includes the impact of biological assets. Excluding the impact, net income was $8 million in the first three months of 2021. The multi-state cannabis operator achieved Adjusted EBITDA of $75 million in the first quarter. Its 52% margin positions Verano as an industry leader.

The company reported cash and cash equivalents of $112 million and working capital of $329 million. Total debt excluding lease liabilities totaled $34 million.

Verano CEO and Founder George Archos said, “Our strong first-quarter performance was foundational in nature and sets the tone for what we expect to be a transformational year. We anticipate considerable quarter-over-quarter growth in 2021 as we begin to realize the impact of accretive acquisitions we’ve made over the last few months, in addition to broad expansion of cultivation capacity and organic retail growth.”

“I am very pleased with our accomplishments to date, particularly how well we’ve executed on our growth strategy. We’ve expanded our retail footprint and production capacity in core markets where we’ve identified substantial near- and long-term upside,” added Archos. (See Verano Holdings stock analysis on TipRanks)

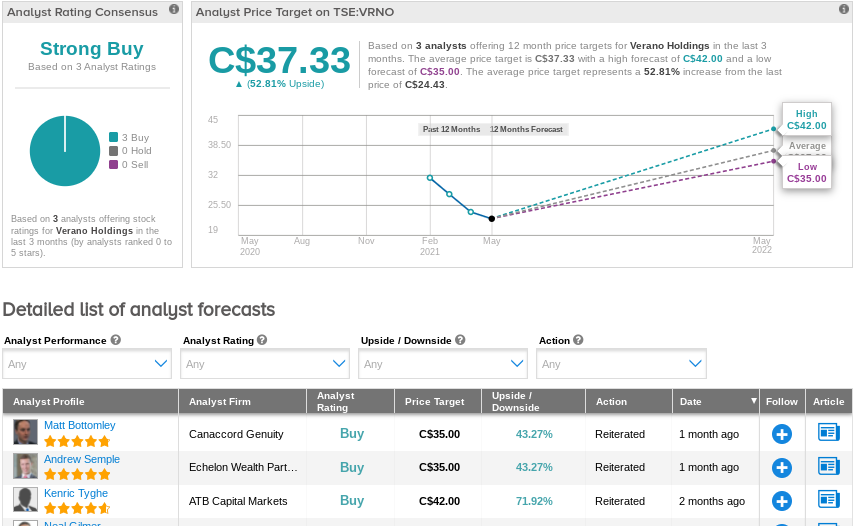

On March 31, ATB Capital Markets analyst Kenric Tyghe maintained a Buy rating on VRNO and a C$42.00 price target for 72% upside potential.

In his February 28 coverage initiation, Tyghe said, “Verano is positioned through 2021 to build on its leadership position in Illinois and establish itself as a top-three operator in several states, including Florida. While Verano has a presence in 14 markets, we believe its six core markets—Illinois, Florida, Arizona, Pennsylvania, New Jersey, and Maryland—are some of the most catalyst-heavy states in the market through our forecast window.”

Overall, consensus on the Street is that VRNO is a Strong Buy based on 3 Buys. The average analyst price target of C$37.33 implies 53% upside potential to current levels. Shares have fallen more than 20% over the past three months.

Related News:

MediPharm Labs Reports a Dismal First Quarter

HEXO to Acquire 48North Cannabis for C$50M

Curaleaf to Acquire Los Sueños Farms for $67M; Shares Jump 3%