Vail Resorts (MTN), a renowned network of iconic ski destinations across North America, Switzerland, and Australia, is witnessing a promising rebound after a disappointing warm winter last year. The company has seen a surge in season pass sales from September through December, likely due to improved snow conditions at several key resorts opening early. Recent FY2025 Q1 results beat top-and-bottom-line expectations, driven by increased summer visitation and activities and improved Hotel ADR and RevPAR.

With an ongoing focus on cost management, the company aims to achieve $100 million in cost savings by FY26 by reducing corporate headcount by 14% and centralizing support functions across 42 ski resorts. However, despite all the company’s best efforts, there is no control over erratic weather, which remains a key risk to the stock moving forward. Long-term investors should approach with caution.

Vail Achieves Peak Status

Vail Resorts boasts a diverse portfolio of top-tier ski resorts worldwide, including notable locations like Vail Mountain, Breckenridge, Park City Mountain, Whistler Blackcomb, and others in North America, Switzerland, and Australia.

Adding to the portfolio, Vail Resorts owns the RockResorts brand, managing an array of sophisticated hotels, vacation rentals, and condominiums around its mountain destinations, including the Grand Teton Lodge Company in Jackson Hole, Wyoming.

The firm was recently named “One of America’s Most Admired Workplaces” by Newsweek, suggesting an esprit de corps that helps make it both an employer and service provider of choice.

Vail Sells Fewer Season Passes but Charges More

For the first quarter of Fiscal 2025, the company reported revenue of $260 million, which exceeded analysts’ expectations. These results were driven by winter operations in Australia and summer activities in North America, including pass product sales for the upcoming 2024/2025 North American ski season, which has seen a decrease of roughly 2% in units but an increase of about 4% in sales dollars compared to the same period last year.

The company often runs at a loss in the first quarter, and this year has been no exception, with a net loss of $172.8 million, a slight decrease compared to the $175.5 million net loss in the same period last year. The EBITDA loss was $139.7 million, including $2.7 million associated with a two-year resource efficiency transformation plan and $0.9 million of acquisition and integration-related expenses. This led to earnings per share (EPS) of -$4.61, handily beating street projections by $0.39.

As of the quarter’s end, the company’s total liquidity stood at $1.024 billion, including $404 million in cash, $407 million of U.S. revolver availability under the Vail Holdings Credit Agreement, and $213 million of revolver availability under the Whistler Credit Agreement. The Net Debt was 2.8 times its trailing twelve months EBITDA. The company announced a quarterly cash dividend of $2.22 per share, payable on January 9, 2025.

Finally, management has adjusted its Fiscal 2025 guidance, expecting net income of $240 million to $316 million, compared to the former estimate of $224 – $300 million. This increase primarily comes from a $17 million profit from real estate sales related to the East Vail property. No changes are expected to EBITDA due to these adjustments, with projections remaining between $838 million and $894 million. These projections assume the return of “typical weather” and normal operational costs.

Shares Show Good Momentum but Are Not Cheap

It has been a more challenging year for the company, reflected in its share price decline of 12% over that period. Yet, the most recent quarter has marked a turning point, and the shares have popped up 8.37% over the past three months. The stock trades near the mid-point of its 52-week price range of $165.00 – $236.92 and demonstrates positive price momentum as it trades above all major moving averages. Yet it’s not cheap, with a P/S ratio of 2.39x reflecting a premium to the Consumer Discretionary sector average of 1x.

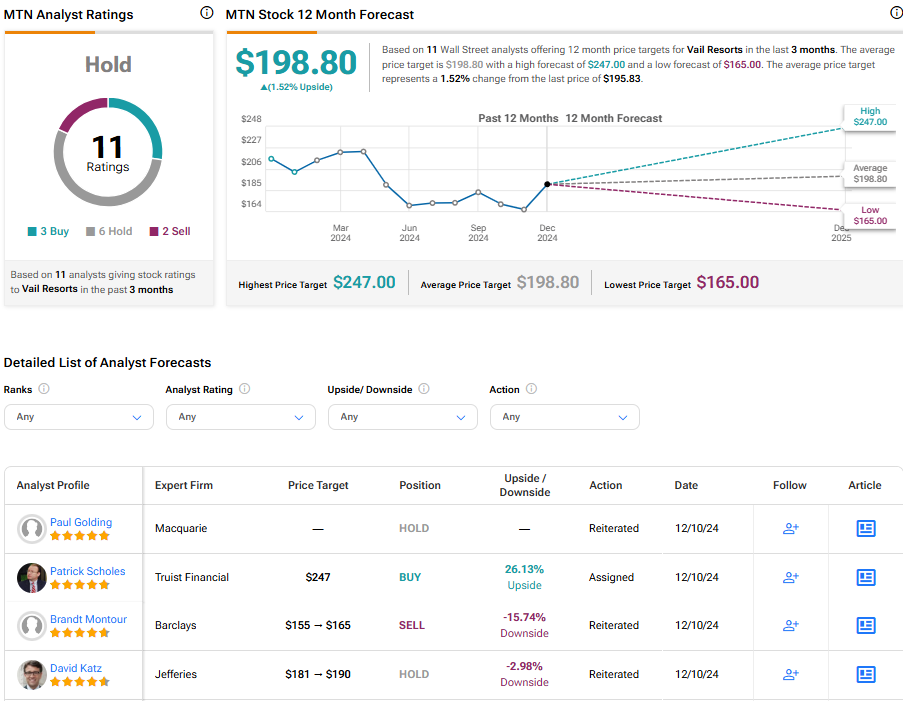

Analysts following the company have taken a cautious outlook on MTN stock. Among the few more bullish in outlook, Mizuho’s Benjamin Chaiken, a four-star analyst according to Tipranks’ ratings, recently raised the price target on the shares to $227 while maintaining an Outperform rating, noting Q1’s results and the attractive setup for the shares moving forward, citing cost savings, easy comparisons to last year’s numbers, and poor investor sentiment.

Overall, Vail Resorts is rated a Hold. The average price target for shares of MTN is $198.80, representing a potential 1.52% change from current levels.

Après-ski on MTN

After enduring a lackluster season last year, Vail Resorts is gaining traction with its promising Q1 results, outperforming top-and-bottom-line estimates, thanks to high summer visitation, better hotel performance, and enhanced snow conditions that have driven a surge in season-pass sales. The company’s commitment to effective cost management, reflected in its goal to realize $100 million in savings by FY26, further illustrates its resilience.

However, investors should remember that the erratic climate remains a significant wildcard that could potentially impact the company’s stock. While Vail Resorts’ recent performance indicates potential for success, unpredictable weather conditions and a high valuation underscore a need for investor caution.