Lockheed Martin’s stock (LMT) has surged by 25% year-to-date, with momentum accelerating in recent weeks. The aerospace and defense giant, known for the F-35 fighter jet, C-130 Hercules transport aircraft, and HIMARS, has attracted bullish sentiment lately due to escalating global tensions. These developments have strengthened its outlook, as rising defense budgets drive a rising order backlog, positioning it for robust revenues and earnings over the medium term. However, the stock’s elevated valuation may pose challenges for further gains and stop it from soaring. For this reason, I am neutral on the stock.

Geopolitical Tensions Rising: Bad for Markets, Great for Lockheed Martin

If you’ve been following global news, you’ve likely noticed the rapid escalation of geopolitical tensions in recent years. Several major conflicts have erupted, with the potential for more on the horizon as global friction continues to intensify. Long-standing conflicts, such as the war in Ukraine and the Israel-Hamas conflict, not only persist but also contribute to a broader sense of global instability.

While geopolitical turmoil undoubtedly introduces uncertainty and challenges to global markets, it has also created significant opportunities for aerospace and defense companies, such as Lockheed Martin. As defense budgets surge, companies in this sector are flourishing, and Lockheed Martin, as one of the major suppliers of aircraft and military systems to the U.S. and its allies, stands out as a primary beneficiary in this landscape.

Q2 Results: Rising Defense Spending Drives Robust Revenue, Earnings Growth

As I just mentioned, Lockheed Martin’s results are benefiting directly from increasing defense spending, driving robust revenue and earnings growth. In its Q2 results, the company posted a 9% year-over-year increase in sales, totaling over $18.1 billion. This revenue growth can be largely attributed to substantial new orders, including multi-year contracts for the PAC-3 missile system and notable international sales of the JASSM ER missiles. Regardless, Lockheed Martin’s rising revenues across all four business segments, as illustrated in the table below, highlight the company’s ability to leverage growing defense spending effectively.

The above table also illustrates that each of Lockheed Martin’s segments posted a rising operating profit. This is due to improved unit economics resulting from growing revenues. Hence, there was a 10% rise in business segment operating profit, which reached $2.04 billion, while the company’s adjusted earnings per share advanced by 5.6% to $7.11.

The substantial earnings momentum is bolstered by Lockheed’s Q2 free cash flow exceeding $1.5 billion, nearly doubling from $771 million a year ago. This remarkable increase is driven by enhanced operating cash flow, thanks to improvements in working capital.

Growth Momentum Set to be Sustained by Near-Record Backlog

Looking ahead, Lockheed’s revenues and earnings are set to benefit from its near-record-high backlog, which continues to be close to $160 billion—more than double the company’s annual revenue. The near-record backlog signifies a strong pipeline for future business and positions Lockheed Martin to capitalize on ongoing and future defense budget increases.

In any case, the current backlog is substantial enough to support record revenues and earnings over the medium term. Consensus estimates project that revenues will climb to $76.81 billion in Fiscal 2026, building on this year’s anticipated $71.25 billion. Similarly, adjusted EPS is expected to rise to $29.90 by Fiscal 2026, up from this year’s forecasted $26.54.

Post-Rally Valuation May Hamper Future Returns

Despite the market’s optimistic sales and EPS projections, the recent rally has pushed the stock’s valuation to rather elevated levels. This could hamper future returns. At a forward P/E of 20.9x, the stock is trading at its highest valuation in approximately six years. This multiple seems steep for a major industrial player potentially at the peak of an industry supercycle.

Sure, defense stocks are likely to remain attractive to investors if current geopolitical tensions persist. Yet, the potential for additional gains from Lockheed Martin’s current valuation appears limited, in my view.

Is LMT Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Lockheed Martin features a Moderate Buy consensus rating based on seven Buys, seven Holds, and one Sell rating assigned in the past three months. At $557.64, the average LMT stock price target suggests 0.1% downside potential, nonetheless. This reflects my concerns regarding the lack of potential gains, moving forward.

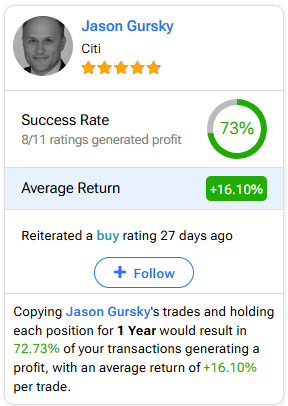

If you’re uncertain about which analyst to follow for buying and selling LMT stock, Jason Gursky of Citi (C) stands out as the most profitable for a one-year timeframe. With an impressive average return of 16.10% per rating and a 73% success rate, he’s a top choice. For more details, click the image below.

The Takeaway

Lockheed Martin’s strong share price performance, results, and favorable outlook, powered by increasing defense budgets and a robust backlog, reflect its critical role in the current geopolitical climate. However, the stock’s high valuation may limit its future return potential. While the company is well-positioned to benefit from ongoing global tensions, the multi-year high valuation could pose risks when it comes to further appreciation. Consequently, I have now become neutral on the stock.