Upstart Holdings (UPST), the company behind the innovative AI-driven personal loan platform, has seen an extraordinary rally, with its stock price soaring 207% over the past six months. This remarkable surge reflects the company’s underlying advancements, such as improving lending models and expanding its product offerings. Nevertheless, the prolonged rally has significantly inflated Upstart’s valuation, raising concerns regarding the stock’s prospects. While Upstart’s progress toward profitability is commendable, its lofty valuation leaves little margin for error. Thus, I am bearish on the stock heading into 2025.

Positive Developments Driving the Rally

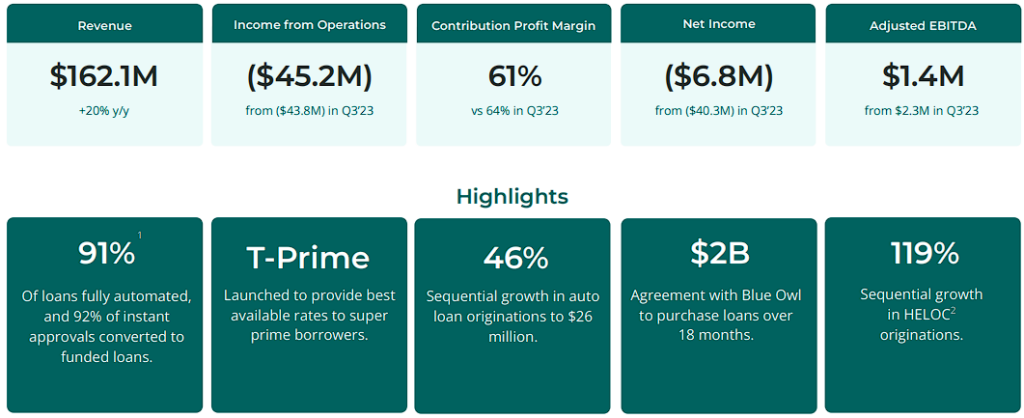

Upstart’s latest Q3 results clearly highlighted its continued developments, which, at first glance, contradict my bearish stance on the stock. The company recorded $162 million in revenue, marking a 20% increase compared to the previous year and an impressive 27% growth from the prior quarter. Lending volume rose by 43%, driven by implementing “Model 18,” an AI-based lending model that greatly enhanced borrower risk assessment and conversion rates. In fact, CEO David Girouard described this model as a significant leap forward, enabling Upstart to calibrate risk and approve loans with much greater precision. Evidently, in Q3 alone, the company originated 188,000 loans, amounting to $1.6 billion in volume—its best quarter in two years.

Beyond its core personal loan product, I am rather impressed by the fact that Upstart has shown its ability to innovate across new verticals. The auto refinancing division, for instance, has achieved a tremendous improvement, with the average time to fund a loan cut from 19 days to 9 days—a win for borrowers and Upstart’s own operational efficiency. At the same time, its HELOC product continues to expand rapidly, with originations doubling sequentially and an impressive 49% of applicants receiving instant approval.

Lastly, another factor worth mentioning that is bolstering Upstart’s momentum these days is its improved funding stability. Through strategic partnerships, such as the $2 billion loan purchasing agreement with Blue Owl’s Atalaya affiliate, the company has ensured access to a continuous stream of capital, even as its origination volumes grow. With 24 new lenders joining in 2024, Upstart has undoubtedly diversified its funding sources, which should prove to be a great contributor to any future success.

Set to Return to Profitability – But Is It Enough?

Now, one of the most promising stimuli of Upstart’s bullish rally is its progress toward profitability. Yet, I don’t believe these developments are enough to justify buying the stock at its current levels. In Q3, the company achieved a contribution margin of 61%, up from 58% in Q2, signaling improved efficiency and cost management. Adjusted EBITDA also turned positive at $1.4 million, which one could argue is a key milestone in the company’s overall recovery. Much of this progress was due to advances in automation and the success of new lending models, which have streamlined borrower onboarding and decreased delinquency rates.

However, Upstart is still expected to close Fiscal 2024 with a loss. Following Q3’s GAAP EPS loss of -$0.06 (adjusted EPS was also negative at $0.07), Q4 consensus EPS is estimated at -$0.04. Therefore, Upstart is expected to close the year with a loss of -$0.45 per share. The thing is, Wall Street anticipates a return to profitability in Fiscal 2025, with an estimated EPS of $0.54. And yet, at the stock’s current valuation, this estimate can barely justify hopping onto the bull train.

Valuation Stretched Thin

To my core argument, while profitability is within reach, the stock’s valuation remains a sticking point. At its current price, Upstart trades at a staggering 125x its fiscal 2025 projected EPS. This multiple leaves little room for error and assumes the company can sustain exponential growth in earnings—a lofty condition given the uncertainties in the lending market. In my view, this bloated valuation translates to significant downside risk for investors if Upstart falls short of the market’s ambitious targets. Any external risks, such as macroeconomic headwinds or credit market trends, could easily disrupt Upstart’s growth story, leading to heavy share price losses.

Is UPST Stock a Buy?

Wall Street analysts appear wary about Upstart’s future prospects as well. Specifically, UPST stock features a Moderate Sell, with analyst ratings now consisting of zero Buy, eight Hold, and five Sell ratings over the past three months. At $24.80, the average UPST stock price target implies a downside potential of 63.74% from its current levels.

For the best guidance on buying and selling UPST stock, look to Dan Dolev. He is both the most accurate and most profitable analyst covering the stock (on a one-year timeframe), boasting an average return of 12.36% per rating and an outstanding success rate of 50%.

Conclusion

Summing up, while Upstart has shown positive progress, its soaring valuation poses substantial risks. The company’s AI-driven advancements, expanding product portfolio, and progress toward profitability are noteworthy achievements that have fueled its recent rally. However, these positive developments may not fully justify the current valuation, which leaves little margin for error in a volatile market. For this reason, I believe investors should proceed with caution, as any divergence from expected growth could result in significant losses in the coming year.