The last few years have been a roller coaster, affecting sectors across the economic board. The arrival of COVID in 2019 has been especially true in the healthcare sector. But conditions are approaching normal now, with the pandemic fading into the background and inflation showing signs of easing. For investors, this normalization makes managed care companies – long the gatekeepers of the healthcare sector – worth a closer look.

Covering this sector from the investment firm Robert Baird, analyst Michael Ha is giving these stocks just that extra scrutiny. Multiple headwinds have battered managed care companies in recent years, including reductions in Medicare rates, higher medical costs, and a spat of cyberattacks – but Ha believes that the industry as a whole has the measure of the situation. Tailwinds, particularly higher healthcare demand from the aging Boomers, will help to lift healthcare stocks as a whole.

“We are bullish long term on Managed Care,” Ha says, and goes on to elaborate: “For the Managed Care companies that are successfully able to build a fully integrated model, we see a bright future over the next decade of attractive long-term sustainable earnings growth, margin expansion beyond historical health insurance levels, and potential for P/E multiple expansion north of the S&P 500.”

Identifying the standout performers is key. Ha has taken the measure of two well-known managed care stocks, UnitedHealth (NYSE:UNH) and Humana (NYSE:HUM), and lays out which one presents the stronger investment opportunity. Let’s take a closer look.

UnitedHealth

We’ll start with UnitedHealth, one of the world’s leading insurance companies – and the largest health insurer in the US market. UnitedHealth boasts a market cap of $451 billion and brought in more than $371 billion in revenues last year. In February of this year, the company was rocked by a ransomware cyberattack against its payment processing unit Change Healthcare. The attack prevented payouts to providers, put confidential patient information at risk, and triggered several Federal regulatory investigations. UNH reportedly paid out a $22 million ransom and in July will begin notifying customers whose data may have been put at risk.

That UnitedHealth has the resources to weather an attack like this is undisputed. The company’s 12-month revenue for the year ending on March 31 came to $379.5 billion, up almost 13% year-over-year – and that period included the height of the cyberattack. The company has been working to restore the affected services and has incurred over $6 billion in direct costs to support healthcare providers that were adversely impacted by the cyberattack.

While UnitedHealth is best known as an insurance provider, the company is also the parent firm of Optum, a customer-facing direct-care health services provider. Based in Minnesota, Optum employs approximately 310,000 people worldwide and provides a varied range of services in the healthcare industry, ranging from technology to pharmacy care and benefits to direct healthcare services. Optum was formed by UnitedHealth in 2011, and within 6 years was accounting for nearly half of the parent company’s profits. Optum brought in $226.6 billion in total revenue in 2023.

UnitedHealth last reported earnings results for 1Q24, and the results beat expectations. At the top line, the company reported total revenues of $99.8 billion, up 8.6% year-over-year and some $490 million ahead of the forecast. Bottom line earnings, by non-GAAP measures, came to $6.91 per share. That included 25 cents per share in ‘business disruption impacts’ due to the Change cyberattack and still beat the estimates by 29 cents per share. For the full year, UnitedHealth estimates the impact of that attack to come to $1.15 to $1.35 per share.

Weathering the cyberattack was good – but beating the estimates based on a sound, and expanding, business was better – and led Baird analyst Ha to describe UNH as his ‘top structural long’ in the managed care segment.

“Managed Care is a game of scale and UnitedHealth is king with top two or three market share in nearly every health insurance line of business. Its scale in health insurance helps to build a competitive moat around its core business, but we believe the true differentiation lies in its Optum business and we are specifically very bullish on OptumCare/OptumHealth,” Ha opined.

Looking ahead, the analyst lays out a firm case for strength in UNH: “We believe the embedded earnings opportunity from converting existing UnitedHeatlhcare MA lives over to full risk capitation in OptumCare/OptumHealth is significant and will help drive increased visibility/sustainability of its long-term earnings stream with opportunity for enterprise margin expansion that should drive multiple expansion beyond historical levels over the next decade.”

These comments support Ha’s rating of Outperform (i.e. Buy) on UNH shares, and his $597 price target implies a one-year upside potential of ~23%. (To watch Ha’s track record, click here)

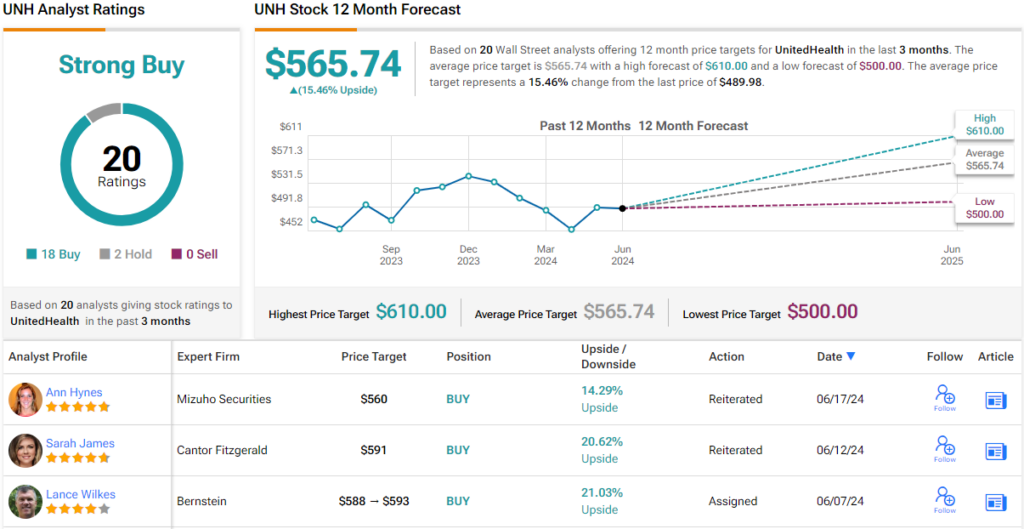

Overall, this mega-cap insurer has a Strong Buy consensus rating, based on 20 recent analyst reviews that split to 18 Buys against just 2 Holds. The shares are priced at $489.98, and the $565.74 average price target suggests that the stock will gain ~15% in the next 12 months. (See UNH stock forecast)

Humana

The next managed care we’ll look at is Humana, a perennial member of the top ten largest health insurers in the US. By revenue, the company is ranked #5; in the full-year 2023, the company brought in more than $106 billion at the top line, for a 14.5% year-over-year increase. The company offers Medicare Advantage plans, including medical and routine dental, vision, and hearing benefits. Additionally, Humana is a major provider of medical, dental, and vision plans for individuals and families in the private insurance market. The company is also a provider of various Medicaid plans, based on eligibility.

As of the end of last year, this Kentucky-based health insurer was providing coverage for nearly 17 million members in the US. This number included approximately 9 million covered under various Medicare plans. The company offers a wide range of plan types to fit the varying needs of its customers. These include HMOs and PPOs, health maintenance organization plans, and preferred provider organizations, as well as special needs plans, or SNPs, and private fee-for-service plans, or PFFSs. While Humana has a wide reach across the US, not every plan is available in every state or zip code.

Humana’s stock has taken two hard hits recently, both in April of this year. At the beginning of that month, the Centers for Medicare and Medicaid Services (CMS), the Federal agency that regulates payments to Medicare and Medicaid providers, authorized a 3.7% rate increase to take effect in the calendar year 2025. While a rate increase was expected, the 3.7% announced was in line with expectations, and it still equates to a substantial increase in the payments the company will have to make. In addition, later in April, Humana reported its 1Q24 financial results – and revised down its GAAP EPS guidance for the fiscal year 2024, from $14.87 to $13.93. While the stock has recovered somewhat from those hits, shares in HUM are down approximately 22% so far this year.

At the same time, Humana’s 1Q24 report beat the forecasts on both revenues and earnings. Revenue in the quarter came to $29.6 billion, up more than 10% from the prior-year quarter and some $1.12 billion better than had been anticipated. The company’s non-GAAP EPS was also sound, and at $7.23 per share, it beat expectations by $1.23.

Still, Baird analyst Ha sees Humana in an unsettled position, and that is the key factor in his stance. He writes of this stock, “We believe uncertainty surrounding arguably the most complex MA bidding seasons to come (2025) will likely keep traditional Medicare Advantage plan multiples depressed in the near future. This coupled with CMS’ recent finalized rule (starting 2027) limiting D-SNP enrollment only to parent plans with an integrated MA and MDCD offering in geographic service areas, places an additional cloud of uncertainty over Humana in the coming years given its lower exposure to Medicaid vs. peers.”

For Ha, the clouded outlook here justifies a Neutral (i.e. Hold) rating, while his price target of $374 suggests a modest 4.5% upside for the shares on the one-year horizon.

Overall, HUM shares have 18 recent analyst reviews that include 8 Buys and 10 Holds, all coalescing to a Moderate Buy consensus rating. Yet, the stock’s $344.29 average price target implies a one-year decline of ~4% from the current share price of $358.04. (See HUM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.