Shares of Verra Mobility Corporation (VRRM) jumped 7.8% at the end of trade on Tuesday, after the company posted robust revenue growth in Q2. The company provides smart mobility technology solutions and services via two segments, Government Solutions, and Commercial Services.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Let’s take a look at the financial performance, as well as what’s changed in the company’s key risk factors that investors should be aware of. (See Verra Mobility stock charts on TipRanks)

A surge in leisure travel coupled with growth in speed and red-light programs helped Verra’s Q2 revenue to increase 61.2% year-over-year to $128.7 million, beating estimates by $17 million.

Verra CEO David Roberts said, “This stellar performance was led by our Commercial Services segment, which grew triple digits year-over-year and 41% sequentially as robust demand for rental cars remained strong in our key tolling markets. Our Government Solutions segment continues to benefit from the NYC school zone speed camera program.”

Importantly, Verra swung to profit in Q2. It generated earnings per share of $0.02 versus a net loss per share of $0.15 a year ago, but lagged consensus by $0.02.

Buoyed by improving business metrics and positive travel trends, Verra provided guidance to reflect a strong second half of 2021. The company estimates 2021 revenue to be in the range of $510 million to $530 million and adjusted EBITDA to be in the range of $240 million t0 $245 million.

On August 10, BTIG analyst Mark Palmer reiterated a Buy rating on the stock and maintained a price target of $19. Palmer believes that Verra shares’ “valuation fails to reflect the company’s prospects once the crisis has fully abated, with its surprisingly strong Q2 print offering support for that perspective while underlining the stock’s attractiveness as a reopening play.”

Based on three Buys, and one Hold, consensus on the Street is a Strong Buy. The average Verra Mobility price target of $18.63 implies a 16.4% potential upside for the stock. Shares are up 18.4% so far this year.

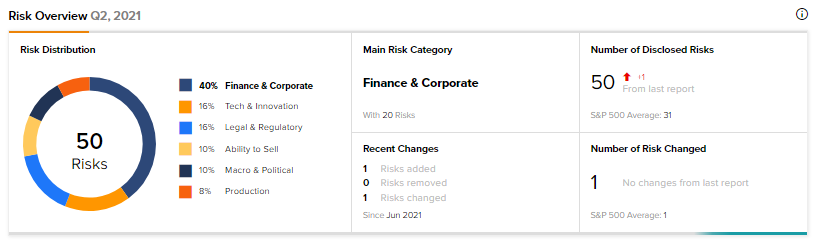

Now, let’s have a look at what’s changed in the company’s key risk factors profile.

According to the new TipRanks Risk Factors tool, Verra Mobility’s main risk category is Finance & Corporate, accounting for 40% of the total 50 risks identified. Since June, the company has added one key risk factor.

In August, Verra announced a $100-million share buyback program, with a duration of 12 months. Verra acknowledged that it cannot guarantee that its stock repurchase program will be carried out fully (or at all), or that this program will enhance long-term value for investors.

A repurchase of shares could also could deplete the company’s cash reserves, while the termination of this stock buyback program may lead to a decrease in Verra’s stock price.

Related News:

BioNTech Q2 Revenues and Earnings Top Estimates; Shares Pop 15%

What Do Qualtrics’ Newly Added Risk Factors Reveal?

What Investors Can Learn from Tyler’s Newly Added Risk Factors