Medical technology company Isoray, Inc. (ISR) is focused on providing advanced treatment applications and devices for delivering targeted internal radiation treatments for cancers throughout the body.

Recently, the company delivered a better-than-expected fourth-quarter fiscal 2021 top line. Let’s look at Isoray’s recent financials and understand what has changed in its key risk factors that investors should know.

Isoray’s revenue in the fourth quarter increased 19% year-over-year to $2.71 million, outperforming analysts’ estimates by $10 thousand. Core prostate brachytherapy revenue increased 5% over the prior year, but its contribution to the total revenue dropped to 74% from 84% a year ago.

Meanwhile, Isoray’s non-prostate brachytherapy revenue increased 92% year-over-year.

Significantly, gross profit increased 26% year-over-year to $1.35 million on the back of higher sales but was partially offset by increased non-isotope material costs and higher headcount.

While R&D expenses jumped 45% due to higher headcount and market research expenses, sales & marketing expenses decreased 4% because of lower incentive compensation. Net loss per share of the company narrowed to $0.01 from $0.02 a year ago. (See Isoray stock chart on TipRanks)

The CEO of Isoray, Lori Woods, said, “Isoray’s business is more diversified than it has ever been as represented by a quarter of the fourth quarter revenue being derived from our rapidly growing non-prostate cancer treatments.

“We continue to believe that the core prostate business is very well-positioned, and we expect to return to the higher pre-pandemic growth rates over time.”

On September 14, Northland Securities analyst Tim Chiang initiated coverage on the stock with a Buy rating and a price target of $1.25. Chiang believes that Isoray stock could bounce as the company announces new partnerships. He sees the recent downward trend in its price as a buying opportunity.

Oppenheimer’s Suraj Kalia also has a Buy rating on Isoray with a price target of $1.65. The two ratings add up to a Moderate Buy consensus rating for the stock. The average Isoray price target of $1.48 implies 133.8% upside potential for the stock. Shares are down 42.4% over the past six months.

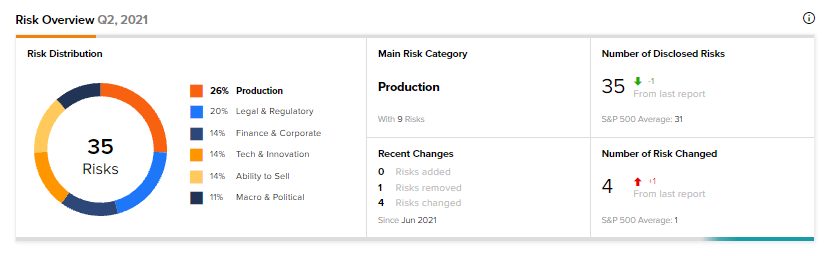

Now, let’s look at what’s changed in the company’s key risk factors.

According to the new Tipranks’ Risk Factors tool, Isoray’s main risk category is Production, which accounts for 26% of the total 35 risks identified. In September, the company removed one key risk factor under the Finance & Corporate risk category.

Isoray notes that it may need additional capital in the future to maintain its NYSE American listing. NYSE considers delisting a company’s shares if it fails to maintain minimum stockholder’s equity.

Isoray highlights that it may not be able to maintain this listing unless it raises additional capital or its market capitalization increases.

The Production risk factor’s sector average is at 11%, compared to Isoray’s 26%.

Related News:

NIO’s September Deliveries Skyrocket 125%; Street Says Buy

XPeng’s September Deliveries Breach Milestone; Analysts Remain Bullish

Canoo, AVL Join Hands to Develop ADAS Software