Shares of beauty retailer Ulta Beauty (ULTA) tanked in after-hours trading after posting Q2 earnings that missed expectations. This can also be attributed to the company’s lowered outlook for 2024, which made things worse.

Earnings per share came in at $5.30 versus analysts’ consensus estimate of $5.56 per share. In addition, sales increased by 0.9% year-over-year, with revenue hitting $2.552 billion. However, this also missed analysts’ expectations of $2.613 billion.

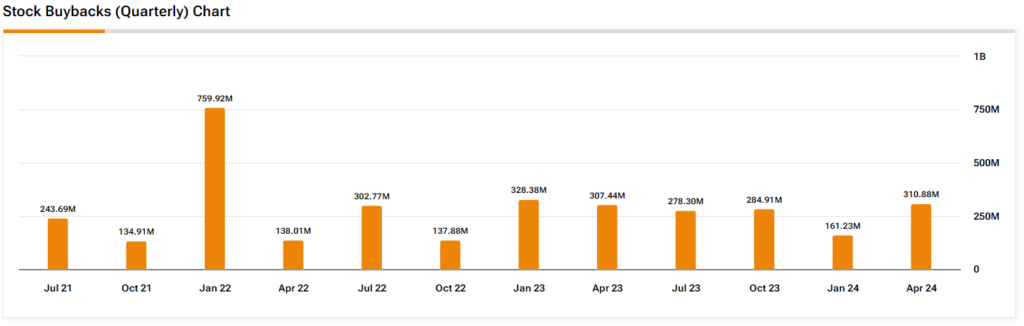

Furthermore, Ulta returned over $212.3 million to shareholders via buybacks during the second quarter. The firm has regularly repurchased its shares in each of the most recent quarters (as demonstrated in the image below) and has $1.6 billion remaining under its buyback plan.

Looking ahead, Ulta expects FY 2024 earnings and revenues to be in the ranges of $22.60 to $23.50 per share and $11 billion to $11.2 billion, respectively. For reference, analysts were expecting $25.26 per share in earnings and revenue of $11.495 billion. Furthermore, it expects to repurchase a total of $1 billion worth of stock for the entire fiscal year.

Is ULTA a Good Stock?

Turning to Wall Street, analysts have a Moderate Buy consensus rating on ULTA stock based on 10 Buys, seven Holds, and one Sell assigned in the past three months, as indicated by the graphic below. After a 12% drop in its share price over the past 12 months, the average ULTA price target of $467.82 per share implies 25.08% upside potential. However, it’s worth noting that estimates will likely change following today’s earnings report.