Uber Technologies Inc. (UBER) announced that it has entered into a Google (GOOGL) master agreement under which the ride-hailing company will get access to Google Maps platform rides and deliveries services.

As part of the four-year agreement, Uber and Google have adopted a new pricing model based on the number of billable trips taken using the services, instead of the number of requests. The transaction also includes tiered volume-based discounts. Financial terms of the agreement weren’t disclosed.

The agreement replaces a previous agreement with Google in connection with its Maps services. According to company filings, Uber paid Google about $58 million for using Maps during 2016 to 2018. Google Maps is built into the the ride-hailing company’s app for the use by its drivers and customers.

“We do not believe that an alternative mapping solution exists that can provide the global functionality that we require to offer our platform in all of the markets in which we operate,” Uber said last year.

Under the terms of the accord, either party may terminate the agreement in the event of material breach by the other party and failure to cure such breach within a reasonable period of time after written notice. Either party may also terminate the agreement if the other party ceases its business operations or becomes subject to insolvency proceedings and such proceedings are not dismissed within 90 days.

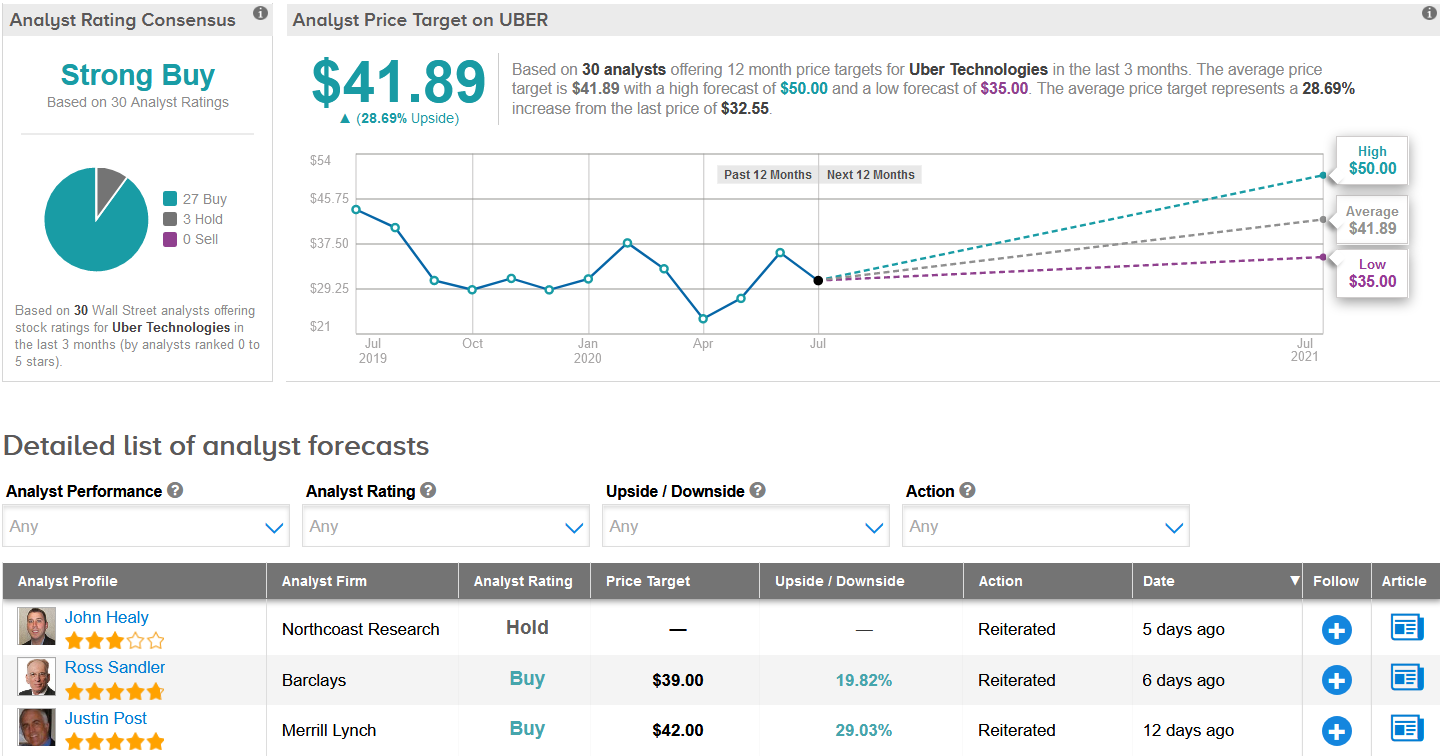

Shares in Uber rose less than 1% to $32.55 on Friday, taking this year’s advance to 9.5%. Looking ahead, the $41.89 average analyst price target implies shares have room to appreciate another 29% in the coming 12 months. (See Uber’s stock analysis on TipRanks).

Five-star analyst Jake Fuller at BTIG earlier this month maintained a Buy rating on the stock with a $47 price target but cautioned that consensus on the company’s financial performance is likely “aggressive”.

Fuller believes that the “ride-hail recovery” is not bending up as work-from-home policies persist and work-related ride volume remains challenged noting that Uber’s “social” rides would have to top 2019 levels “by a lot” in the second half of 2020 to make consensus.

However, the analyst adds that Uber’s stock price suggests that the risk to estimates appears to be priced in.

The rest of the Street shares Fuller’s bullish rating outlook. The Strong Buy analyst consensus boasts 27 Buys versus 3 Holds.

Related News:

Uber Buys Routematch To Expand Public Transit Operations

Beyond Meat Shares Rise On Sale Of Plant-Based Meat In Brazil

Uber Snaps Up Postmates In $2.65B Stock Deal- Report