TripAdvisor (TRIP) stock soared nearly 14% yesterday amid reports of rumored acquisition interest in the $18-19 range. TRIP is my most significant stock position and was my top recommendation entering 2025, so I’m pleased with the latest developments. That said, I expect any takeover offer in the rumored range to be quickly rebuffed by TripAdvisor’s management.

I maintain a Strong Buy rating on TRIP from a long-term perspective. Still, trading activity before the next earnings release could be volatile as various factors from inside and outside the boardroom (including takeover rumors) play out on trading screens across Wall Street.

TripAdvisor was the first stock I listed as a recommended portfolio addition during the tax-loss selling season in December 2024.

Solid TRIP Fundamentals Need Time to Simmer

TripAdvisor is a U.S.-based company best known for its branded website focused on hotel and restaurant reviews, similar to Yelp (YELP). The company began listing travel booking prices alongside its review pages to add differentiating value in a busy online marketplace. TripAdvisor is not an online travel agency (OTA), but it has partnered with OTAs and earns revenues from directing business through its website.

Viator, TripAdvisor’s secondary business, has become the largest segment. Revenues for Viator in Q3 2024 reached $270 million, up ~10%, versus branded TripAdvisor’s quarterly sales of $255 million. Viator operates as a “travel experiences” platform, with local travel agencies around the globe listing their tour offerings to tourists. One of the differences between the branded TripAdvisor and Viator platforms is that through Viator, the revenue partners are smaller companies, which puts Viator in a position of strength. In contrast, the branded TripAdvisor platform is vulnerable to being squeezed by large OTAs.

The company also owns an up-and-coming restaurant booking segment called TheFork. This business has shown the most significant growth multiple of all, but with revenues currently accounting for less than 10% of TripAdvisor’s consolidated sales, it doesn’t represent a significant proportion (for now).

TripAdvisor’s Financials Indicate Long-Term Value

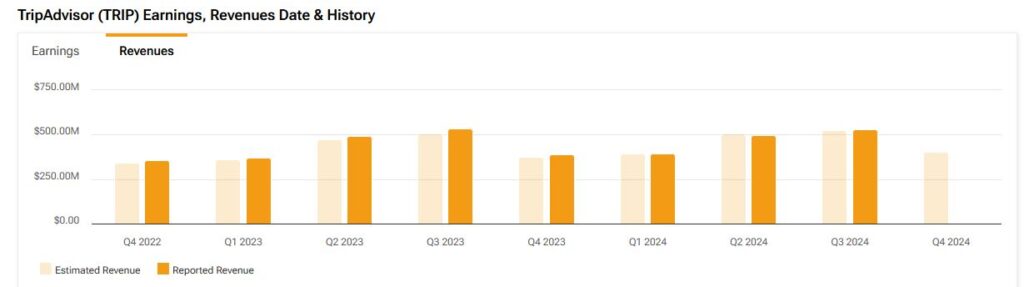

As a travel-related company, TripAdvisor’s businesses are seasonal. The summer season falls within Q3, the most recent quarter reported by the company. Those results were soft, and combined revenues dropped by $1 million to $532 million. Investors were justifiably disappointed, especially since the Olympics occurred during TripAdvisor’s busiest time of year. Company management had guided to a soft Q3 on weak macro trends, but that didn’t stop investors from driving shares more than 10% lower the day after those earnings were released.

TripAdvisor is a profitable company, though. The firm carries gross margins above 90% and operating income in the 8% range. Normalized diluted EPS has totaled $0.62 over the past four quarters (which puts the stock at a trailing P/E of 29x after this week’s re-rating). The company’s cash position is very positive, and thankfully, TRIP has repurchased $25 million worth of stock in 2024.

Regarding its balance sheet, TripAdvisor carries debt but has been operating with a net cash position showing around $50 million annual growth. That net cash balance is set to flip to a net debt position shortly, however, as the company agreed to acquire Liberty Tripadvisor Holdings, an associated company that held 29 million TRIP shares for itself. For all intents and purposes, the acquisition is primarily a large share buyback, with the added benefit of simplifying TripAdvisor’s corporate structure.

Weak TripAdvisor Share Price Attracts Acquisition Vultures

After spending a few years in the high-teens to low-$20 range, TRIP stock rose sharply in early 2024 as it was reported that several possible acquirers were circling TripAdvisor. Shares hit a 2024 high mark of $28 per share but gave up 50% by August. TRIP management came out of the merger discussions without a deal, walking away thinking they couldn’t get fair value for the company’s assets. Shareholder disappointment, partially from M&A speculators and soft business guidance, resulted in the stock pulling back sharply.

I never lost hope in TripAdvisor’s potential, primarily via its Viator segment, while also theorizing that TRIP’s management didn’t sell the company because of a disagreement over Viator’s fair value. The company has faced an optics problem, as its primary business (the TripAdvisor website) was bleeding revenues, with overall growth having declined to an almost non-existent level. However, the investment focus should change since Viator has overtaken branded TripAdvisor as the largest segment (by sales) and recently became EBITDA profitable. Unless the branded TripAdvisor business makes a miraculous comeback, TripAdvisor is now a story primarily about Viator. I like that story and see a lot of potential for the future here.

TRIP shares rose more than $2 to close just under the $18 level following news that Liberty TripAdvisor had been approached about a possible acquisition for its entirety. However, the interested party was not named. In early 2024, the acquisition interest reportedly came from private equity circles, specifically Apollo Global Management (APO). Since TRIP management walked away from a potential acquisition north of $25 less than a year ago, I find it unlikely that one of the same parties has inquired about a cash purchase in the $18-19 range this week. In my view, this looks like interest from a new party.

Unfortunately, I don’t think there’s any chance TripAdvisor will be sold for under $20, and probably not for under $25, either. I don’t know whether company management will publicly comment on the rumored offer or if the rumor will fade organically. Regardless, I’m holding a core position in TRIP with a target price of $25 or above.

Is TripAdvisor a Good Stock to Buy?

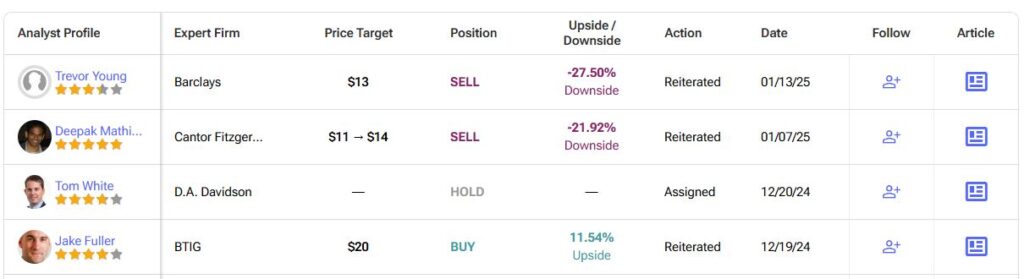

According to Wall Street analysts, TRIP carries a consensus Hold rating from 11 analysts who cover the company. Currently, TRIP stock carries two Buy, five Hold ratings, and four Sell ratings. The average TRIP price target is $17.22 per share, which implies that TRIP is overvalued and is expected to decline by 4% to reach its price target.

Long-Term Patience Required to Tap Into TRIP

As a TripAdvisor shareholder, seeing some life in the stock after a ~9-month lull is excellent. That said, I doubt the rumored takeover in the $18-19 range will go anywhere, as it grossly undervalues the company.

Furthermore, it’s worth noting that TripAdvisor management agreed to acquire Liberty TripAdvisor’s TRIP shares for $16.21 per share when the stock was trading at 52-week lows below $13. That’s a heavy premium for buying a large block of your own stock, but clearly, management felt doing so would still be value accretive. The possibility that they’d suddenly agree to sell the entire company for 11-17% higher seems highly unlikely.

In the near term, there remains a possibility that Apollo or other parties will resurface and embroil TripAdvisor in a bidding war that eventually results in a sale in the mid-$20 range.

I maintain my Strong Buy rating on TRIP stock for the long term. Management seems optimistic heading into Q4, and analysts are expecting the company to return to growth when they report their results on February 12, 2025. I expect Viator to become the focal point as the broader TripAdvisor narrative brightens up in 2025.