Tractor Supply (TSCO) reported stronger-than-expected Q2 results, topping both earnings and revenue estimates. Despite the robust results, shares of the largest U.S. rural lifestyle retailer plunged 4.3% to close at $180.94 on July 19.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The company reported adjusted earnings of $3.19 per share, beating analysts’ expectations of $2.90 per share. Net Sales of $3.6 billion exceeded the consensus estimate of $3.42 billion.

Meanwhile, earnings per share jumped 10%, while net sales increased 13.4% on a year-over-year basis. The company reported earnings of $2.90 per share in the prior-year period. (See TSCO stock charts on TipRanks)

Comparable store sales grew 10.5% in the quarter, driven by a higher number of transactions, average ticket growth, and increased demand for everyday merchandise. Notably, same-store sales increased 41% on a 2-year stack basis.

Tractor Supply’s CEO Hal Lawton commented, “The team is executing at a high level and advancing our Life Out Here Strategy while navigating the cost pressures we are experiencing. With a resilient business model, ongoing market share growth and strategic investments to transform the Company, we are excited about the significant opportunities ahead of us and remain committed to disciplined financial returns and sustained profitable growth.”

Based on robust Q2 results and market share gains, the company raised its guidance for Fiscal 2021. It now forecasts adjusted earnings in the range of $7.70 – $8.00 per share, while the previously guided EPS range was $7.05 – $7.40. Revenues are forecast to be in the range of $12.1 – $12.3 billion versus the previous guidance range of $11.4 billion – $11.7 billion.

Moreover, comparable store sales are forecast to grow 11% to 13% versus the prior guidance range of 5% to 8%.

Following the upbeat Q2 results, Robert W. Baird analyst Peter Benedict reiterated a Buy rating and a price target of $210 (16.1% upside potential) on the stock.

Benedict sees current share price weakness as a buying opportunity and remains confident that the company’s competitive moat should widen going forward and lead to significant share price gains. He said that “some conservatism is at play,” especially for the fourth quarter.

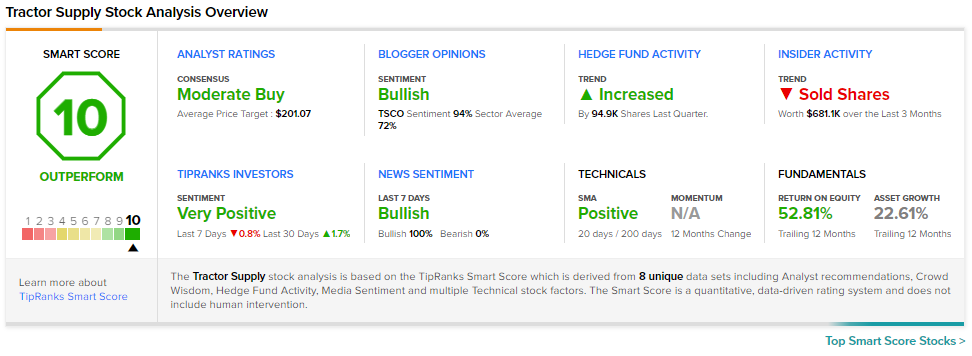

Consensus among analysts is a Moderate Buy based on 9 Buys and 9 Holds. The average Tractor Supply price target of $201.07 implies 11.1% upside potential to current levels. Shares of TSCO have jumped 25% over the past year.

Tractor Supply scores a “Perfect 10” on TipRanks’ Smart Score rating system, indicating that the stock has strong potential to outperform market expectations.

Related News:

State Street Posts Upbeat Q2 Results, Shares Leap 2.9%

Autoliv Misses Q2 Estimates, Shares Plunge 4.8%

KKR to Create Colombia’s First Digital Infrastructure Company with Telefónica