Broadcom (AVGO) shares slumped 5% yesterday despite the semiconductor titan delivering superb Q4 earnings results last week. More broadly, the stock is down 26% from its all-time high of $250. Broadcom is best known as the maker of custom AI chips and is also gaining popularity for its infrastructure software offerings. Its major customers include hyperscalers like Alphabet (GOOG) and Meta Platforms (MSFT). Management is secretive about its customers but has confirmed three unnamed major hyperscalers that it serves, plus four new potential hyperscalers that it’s working with and might serve soon, according to the latest earnings call.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

Despite the stock’s volatility over the past three months, I reiterate my bullish stance on AVGO as I see it achieving new heights in the long term. Broadcom wields a durable competitive advantage in custom chips and has a sizable revenue opportunity in AI. The fundamentals are solid, but market bears are reacting to short-term noise related to tariffs and the new low-cost Chinese models. Although Chinese disruptors challenge the view that AI needs pricey chips, AVGO remains well insulated.

What Can Hurt Broadcom?

I believe that tariff worries have been put on hold for some time now as President Trump paused them and discussed revisiting the situation in April. As far as DeepSeek is concerned, I maintain my opinion and believe that this is a problem for companies like OpenAI and not companies like Broadcom or Nvidia (NVDA). If a Chinese company got its hands on Broadcom’s recipe for custom silicon and AI networking chips, I would have been worried.

In my view, Broadcom’s custom AI accelerators will stay relevant even if a low-cost model from China can rival its US counterparts because the US is busy developing its own technology. Another thing to note is that DeepSeek is being actively banned by governments worldwide due to its open-source nature, which raises privacy concerns. Broadcom is not under threat as its customers are still advancing their models and spending hefty sums on AI-related capex. US tech giants have earmarked over $300 billion in AI-related capex in 2025 alone, with some companies like Meta projecting “hundreds of billions” in AI spending over the next few years.

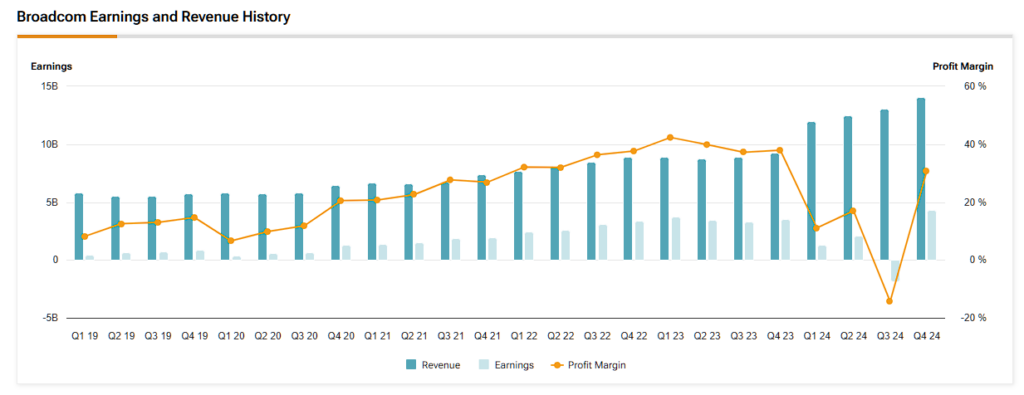

So, these short-term hiccups caused volatility in AVGO stock in recent weeks. While I am not ruling out the risks of tariffs to Broadcom, I am not turning bearish on a high-quality company just yet. I think the company’s fundamentals are still intact; the latest quarter is a testament to that. Broadcom reported 25% revenue growth for Q4 and beat analysts’ estimates by over $325 million. The company’s AI revenue was a top contributor and surged 77% year-over-year to $4.1 billion, ahead of its guidance of $3.8 billion.

Additionally, the company’s infrastructure software business (VMware) grew 47% year-over-year to $6.7 billion. I believe this unit is promising and gives Broadcom a diversification edge against the cyclicality of the semiconductor industry. VMware helps enterprises access compute power virtually without installing the hardware or software on their own computers. Broadcom acquired the company back in November 2023 for $69 billion, and needless to say, it’s been a massive success for the company.

During the quarter, Broadcom converted 60% of its VMware customers to subscriptions from perpetual licenses. That’s impressive progress, considering that many of its VMware customers were not initially happy with the replacement of perpetual licenses. Broadcom has also successfully sold its full-stack data center virtualization offering to 70% of its 10,000 VMware customers.

Broadcom’s AI Revenue Can Potentially Double By 2027

Broadcom’s growth rates are undoubtedly impressive, and I think the $4 billion print in AI revenue is something investors should pay close attention to. For Q1 2025, the company is guiding to $4.4 billion in AI revenue, which I firmly believe it will surpass as it has beat its guidance multiple times in previous quarters. Investors need to realize that its AI business is growing at double-digit rates and is still not at its full potential.

Management reaffirmed that it expects its three hyper-scale clients to generate a serviceable addressable market (SAM) of about $60-$90 billion in FY2027. In 2024, Broadcom’s total AI revenue was ~$12 billion, a fifth of the $60 billion minimum expected from three major customers. I pointed out above that the company is working with four new hyperscalers, which have not been accounted for in the 2027 SAM projection. These four hyperscalers are not official customers just yet, but there’s little reason to doubt the commercial eventuality on the cards.

Moreover, the custom chip kingpin still has a lot of revenue to realize. Even if it gets 50% of the projected SAM in 2027, and the rest goes to other smaller custom chip makers like Marvell Technology (MRVL), its AI revenue will double from 2024 levels. That is the big picture many bears and panic sellers are missing. Broadcom isn’t fundamentally troubled; it’s an excellent business firing on all cylinders.

Top Wall Street Analysts Reaffirm Confidence in AVGO Stock

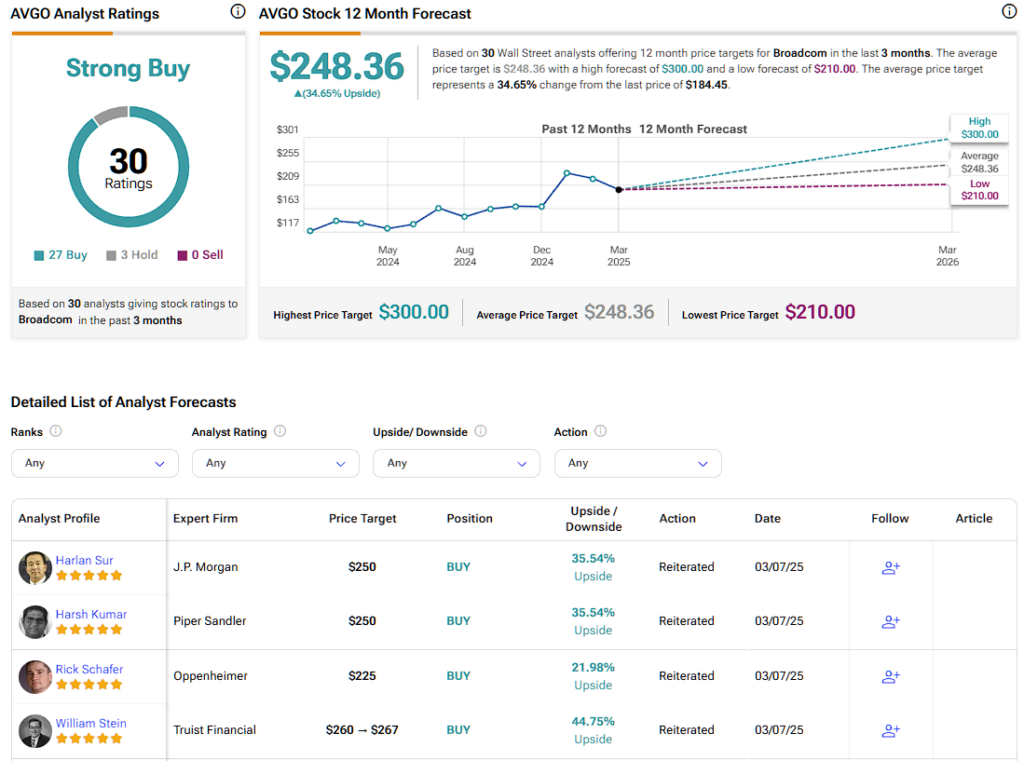

Following Broadcom’s earnings, multiple Wall Street analysts reiterated their bullish ratings on AVGO stock. On March 7, J.P. Morgan analyst Harlan Sur, a five-star analyst according to Tipranks’ ratings, reiterated his Buy rating and $250 price target on AVGO stock. Sur cited a strong quarter, robust demand for the company’s AI networking products, and its leadership in the AI infrastructure market as the primary drivers of his bullish stance. Additionally, the analyst pointed out Broadcom’s successful execution in upselling its infrastructure software offerings, which will contribute to its stable revenue growth.

The semiconductor industry is cyclical, and Broadcom’s non-AI semiconductor revenue has been lagging. However, growth in infrastructure software and AI semiconductors has more than offset the cyclicality.

After earnings, Broadcom is trading at 29.5x its FY2025 earnings estimate, which is fair value for the stock, in my opinion. Considering its expanding AI opportunity, Broadcom can deliver healthy profit growth over the next few years and justify current valuations.

Is Broadcom a Buy, Sell, or Hold?

On Wall Street, AVGO stock carries a Strong Buy consensus rating based on 27 Buy, three Hold, and zero Sell ratings over the past three months. AVGO’s average price target of $248.36 per share implies approximately 35% upside potential over the next twelve months.

Long-Term View Trumps Short-Term AVGO Volatility

Broadcom’s fundamentals remain strong despite recent volatility due to tariffs and DeepSeek. The market for its custom AI chips is expanding, and it sits on a sizable revenue opportunity that can potentially double over the next two years. Additionally, the integration of VMware was a success and gives it a diversification edge. The company is firing on all cylinders and is available at a fair price.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue