Over the past year, SoundHound AI (SOUN) stock has recorded one of the wildest rides among all AI stocks. What makes SoundHound’s investment case intriguing is that the company seems to have set itself apart by focusing on voice recognition and natural language interactions rather than purely large-scale language models. In 2024, the stock surged parabolically as enthusiasm for anything AI-related reached new heights. And yet, 2025 has brought a sharp correction, with the market raising questions about its long-term outlook. The stock now trades below $10, well below the heady days of $20 per share. Given the radical contrast between analyst opinions, I prefer to stay neutral on SoundHound, for the time being at least.

With SoundHound’s Q4 earnings report just days away, investors are debating a key decision: Is it time to buy, sell, or hold? Can investor excitement translate into real progress toward sustainable growth, or is its ambitious vision set to result in continued losses?

What Does SoundHound AI Do?

SoundHound’s bread and butter is its proprietary voice recognition and conversational AI technology. The company has inked deals with automotive giants like Hyundai (HYMTF), Stellantis (STLA), and Lucid Motors (LCID) to bring voice-driven functionality to their infotainment systems. From hands-free calls to navigation, SoundHound aims to make in-car experiences safer and more intuitive.

But its ambitions go far beyond the auto industry. SoundHound has been moving swiftly in the restaurant and customer service sectors, proving its technology’s versatility. Partnerships with major brands like Chipotle (CMG) and White Castle are putting its voice assistants to work, handling phone orders, customer inquiries, and even drive-thru interactions with impressive accuracy. These integrations hint at a future where a significant share of quick-service restaurant interactions might occur via AI-powered voice, cutting wait times and improving efficiency.

Still, the central question is whether all these partnerships can push SoundHound toward a robust, self-sustaining revenue model. Voice AI is an emerging essential. Nevertheless, we should not forget that apart from the natural tailwind in play, competition in this space is utterly brutal, and SoundHound has to somehow come out with both superior tech and a tangible, realistic path to a positive bottom line.

Quick Q3 Recap: Growth Gains vs. Profitability Pains

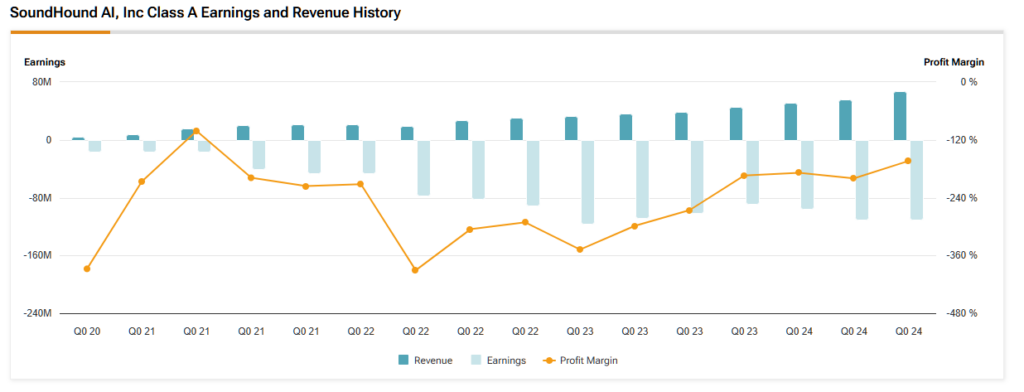

Let’s quickly rewind to Q3 for context. SoundHound achieved record revenue of $25.1 million, marking a staggering 89% year-over-year growth. But don’t rush to a verdict just yet. At first glance, such a vast growth rate would typically reflect a surge in demand for conversational AI, especially when we consider how quickly businesses are trying to modernize their customer experiences. This is partially true.

However, if we drill down, we can see that SoundHound posted a net loss of $21.8 million or a net loss of $15 million on an adjusted basis. On a per-share basis, that translates to a $0.06 loss, slightly ahead of analyst estimates but a reminder that the company is burning through cash by the day. Of course, it’s not unusual for AI-focused companies to operate at a loss during a rapid expansion phase. However, investors naturally want to see a roadmap to profitability, even if the road is bumpy. I am not sure that this road map is there, and with only $136 million left in the bank at the end of the quarter, it makes sense to see frustration levels rising.

Encouragingly, SoundHound is expected to post revenues of $33.7 million in Q4, implying another superb year-over-year growth of 96.5%. Yet, the company is still expected to post a net loss of around $0.10 per share. This dichotomy (rapid growth vs. sustained losses) will again be front and center on February 27.

Major Moves Since Last Report

Since that last report, SoundHound’s management has taken several key steps to strengthen its presence in automotive AI. One key move was deepening its partnership with Lucid Motors, bringing voice assistants to Lucid’s luxury EV lineup. This collaboration aligns SoundHound with an automaker known for cutting-edge, high-end technology, a crucial strategic fit for its brand.

Then came the reveal at CES 2025: SoundHound’s in-vehicle food ordering system, which allows drivers to place orders using voice commands from behind the wheel. If SoundHound can corner the market on seamless in-car transactions, voice commerce could become a lucrative channel down the road.

On a less positive note, Nvidia (NVDA) divested its stake in SoundHound earlier this month, prompting a steep 30% drop in the stock. While Nvidia hasn’t offered much explanation, losing a major backer rattled investors who wonder if SoundHound can remain competitive without heavyweight institutional support.

SOUN’s Risky Valuation

Regarding valuation, SoundHound’s 2024 and 2025 (forward) price-to-sales (P/S) ratios hover around 42x and 21x. Therefore, you can see how SoundHound is trading at a seemingly hefty multiple on this year’s expected sales. However, that multiple is expected to halve next year, implying another 2x in revenues year-over-year in 2025. But it also amplifies risk: if SoundHound’s revenue growth slows or fails to meet lofty expectations, the stock could tumble further.

Profitability (or lack thereof) continues to be a sticking point. Although SoundHound held $136 million in cash and equivalents at the end of Q3, a persistent high burn rate means it may need to raise additional capital. Any new funding round post-Q4, given further losses should be posted in this quarter, is to dilute existing shareholders, a scenario no investor enjoys.

Meanwhile, the competitive landscape remains fierce, with players like OpenAI, Amazon (AMZN), and Alphabet (GOOGL) perfecting large-scale AI models that might ultimately pivot aggressively into voice technology. For SoundHound to outlast these giants, it must deliver superior voice solutions and meaningful return on investment to partners and clients alike. Thus, investors should consider how management addresses this situation in the Q4 post-earnings call.

Is SOUN Stock a Good Investment?

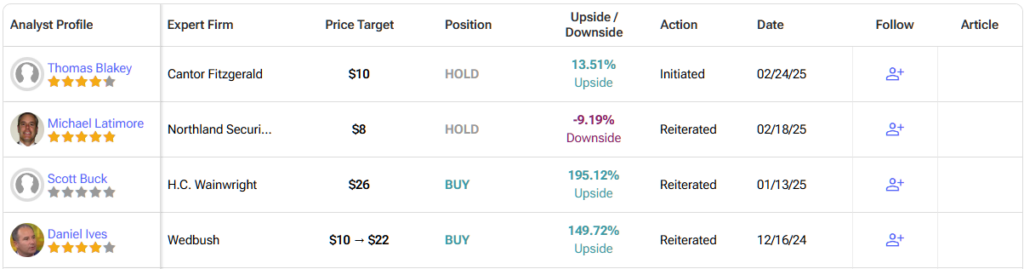

On Wall Street, there is disagreement about the future of SOUN’s stock price. While one analyst screams Hold, others recommend a Buy. On average, Wall Street maintains a Moderate Buy consensus rating on SOUN stock, based on two Buy and one Hold ratings issued over the past three months. SOUN’s average price target of $18.67 per share suggests a staggering potential upside of 112% over the coming 12 months.

Meanwhile, Cantor Fitzgerald analyst Thomas Blakey initiated coverage of SOUN earlier this week, giving it a Neutral rating and a price target of $10.

Risk Appetite Decides How to Handle SOUN Stock

Ultimately, deciding what to do with SoundHound stock before the earnings depends on your appetite for risk. If you’re convinced voice recognition and conversational AI will remain pivotal—and you trust SoundHound to manage its rapid growth responsibly—this could be a long-term gem in your portfolio. A strong Q4 report showing improved financial discipline might spark a rebound.

However, if you’re cautious about unprofitable tech plays in a market increasingly prioritizing cash flow, it might be wise to stay on the sidelines until the company demonstrates a tangible path to breaking even. One earnings report won’t settle every question. Still, Q4 will offer key clues about SoundHound’s ability to sustain its growth, cut costs, and convince investors that its voice-first strategy isn’t just compelling but also profitable in the making. Given this setup, I hold a neutral stance on the stock.