Palantir (NASDAQ:PLTR) has been an early winner in the AI game, with the shares delivering huge returns of a mighty 370% over the past year.

It’s a sharp upward trajectory that has been built on plenty of hype but not exclusively so. In fact, Morgan Stanley analyst Sanjit Singh has been somewhat taken aback by the big data specialist’s success, having “underappreciated several factors” behind the company’s rise. “In the past ~18 months,” says the analyst, “Palantir has executed ahead of our expectations on several fronts.”

For one, Palantir’s US Commercial segment experienced accelerated year-over-year growth of roughly 50% in FY24, up from 36% in FY23, driven by the success of its AIP product offering and an effective bootcamp go-to-market strategy. Meanwhile, the Government business rebounded with growth of around 27%, compared to 11% in FY23, following several significant US Government contract wins. Additionally, the company demonstrated strong cost management, with operating expense growth slowing to 5% YoY in FY24, down from 7% in FY23 and 41% in FY22. This contributed to approximately 900 basis points of margin expansion in FY24.

“To put it bluntly,” Singh went on to add, “if executive management teams and decision makers want to get their AI initiative into live production environment rapidly, Palantir has emerged as one the select few partners to call.”

But in light of all those huge gains, the big question is, does all of that make the stock a Buy right now?

The simple answer, according to Singh, is no. “The inflection in growth and our positively revised assessment of Palantir’s positioning in the Gen AI cycle is well reflected in shares,” the analyst opined.

For instance, the outsized returns have mostly been driven by “multiple expansion” with PLTR’s 56x EV/NTM Sales multiple ballooning by +292% in 2024, while FCF and revenue estimates have been adjusted upwards by a relatively modest 41% and 10%, respectively. And with the company indicating an upcoming investment cycle, the prospects for further expansion appear “more muted.” Meanwhile, the Commercial business, which is expected to be the primary driver of the AI narrative, has contributed less to the CY25 revenue estimate revisions compared to the Government business. Not to mention, Palantir is trading “well ahead of High-Growth Software peers.”

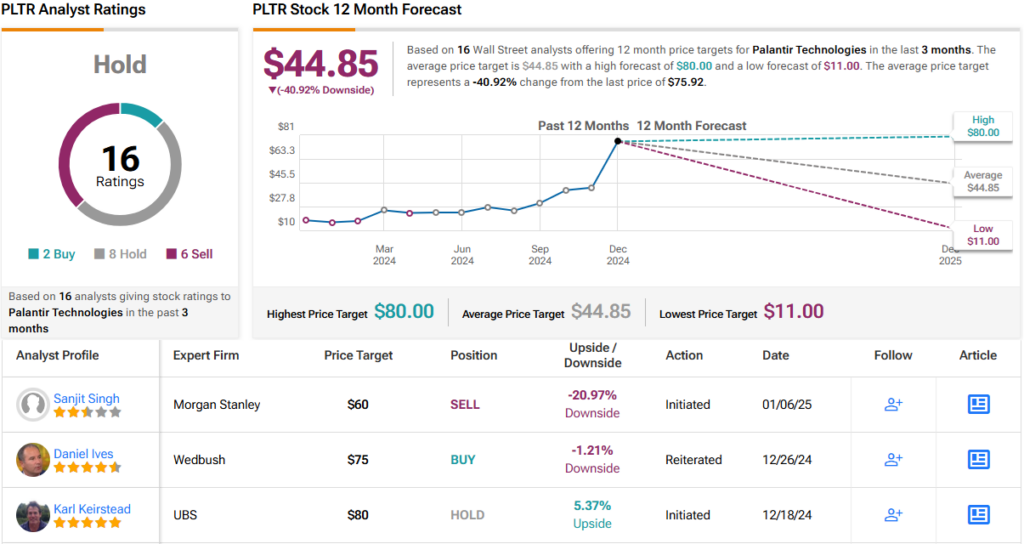

As such, despite acknowledging PLTR’s excellent positioning in the AI game, Singh rates the stock as Underweight (i.e., Sell), while his $60 price target implies a downside of 21% awaits in the year ahead.

Turning to the rest of Wall Street, 5 other analysts join Singh in the bear camp and with an additional 8 Holds and just 2 Buys, the stock claims a Hold (i.e. Neutral) consensus rating. That said, that might as well be a Sell, given the average target stands at $44.85, suggesting ~41% downside from current levels. (See PLTR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.