SoundHound AI (NASDAQ:SOUN) shares have had a remarkable run in 2024, to say the least. The voice AI innovator, which allows companies to create customized conversational experiences, has seen its stock skyrocket by ~340% year-to-date.

While the company has undoubtedly benefited from the broader momentum in AI, several key developments have directly fueled this impressive growth. These include successes in diversifying its customer base, securing a $1 billion bookings backlog, and maintaining a strong partnership with industry giant Nvidia.

In its recently reported Q3 FY 2024 results, SoundHound posted revenues of $25.09 million, reflecting an 89.2% year-over-year increase. Furthermore, the company raised its full-year revenue guidance, now forecasting 2024 revenues between $82 million and $85 million, while projecting 2025 revenues to climb significantly to a range of $155 million to $175 million. On the earnings front, the adjusted EPS of -$0.04 beat expectations by $0.03.

Despite this strong performance, top investor Juxtaposed Ideas remains cautious, questioning whether SOUN’s share price can sustain its momentum heading into 2025.

“SOUN’s expensive valuations and delayed path to profitability offer a minimal margin of safety, worsened by the volatility arising from the (potential) AI bubble,” asserts the 5-star investor, who sits in the top 4% of TipRanks’ stock pros.

Juxtaposed attributes SoundHound’s weakening balance sheet and delayed path to EBITDA profitability to acquisition and growth-related expenses. While these factors may pressure next year’s performance, the investor believes they could support growth over the longer term.

“Long-term shareholders need not fret, since these efforts have been top line accretive,” states Juxtaposed, adding that these outlays also demonstrate “SOUN’s high-growth start up stage.”

Nevertheless, the near-term outlook remains challenging. Juxtaposed warns that SoundHound is rapidly burning through cash, with cash and equivalents down 32.3% quarter-over-quarter, while outstanding shares have risen by 8.6% over the same period. The investor predicts another round of shareholder dilution is likely imminent.

Additionally, the stock’s valuation has become increasingly stretched. Over the past two months, SoundHound’s Forward EV/Sales and Forward Price/Sales ratios have more than doubled. Juxtaposed notes that other generative AI SaaS stocks have similarly seen valuations balloon, signaling potential market volatility ahead.

Given these risks, Juxtaposed recommends “waiting for a moderate retracement,” assigning the stock a Hold (i.e. Neutral) rating. (To watch Juxtaposed Ideas’ track record, click here)

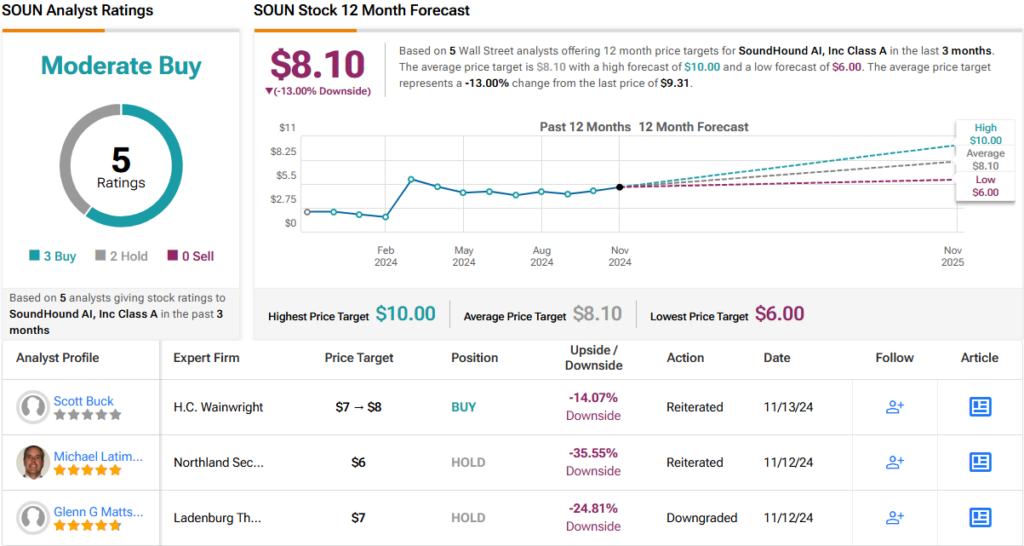

Turning to Wall Street, SoundHound carries a Moderate Buy consensus rating based on 3 Buy and 2 Hold recommendations. However, analysts agree that the stock’s outsized share gains may have outpaced its fundamentals. The average price target of $8.10 suggests a potential downside of 13% in the months ahead. (See SOUN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.