While several EV startups have set their sights on claiming a chunk of the global EV market, the segment has been less than kind to upstart OEMs. Plenty have suffered against a backdrop of higher interest rates, elevated pricing and waning demand.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

However, as the ongoing shift to an EV world continues, one company looks well-set-up to carve a piece out of the market. That at least is the opinion of BTIG analyst Gregory Lewis, when assessing the prospects of Vietnam-based auto manufacturer VinFast Auto (NASDAQ:VFS).

“Key to VFS’ success should continue to be the backing from parent Vingroup, the largest conglomerate in Vietnam,” the analyst explained. “The founder and largest shareholder has committed ~$2.5B in grants/loans (should all be distributed by April 2024) and we view the founder’s backing as crucial as VFS looks to scale globally.”

The backing, says Lewis, differentiates VFS from the pack. The firm was established in 2017 as a subsidiary of Vingroup, which is led by the country’s wealthiest individual, Pham Nhat Vuong. Vingroup has a significant presence in various sectors, including technology, industrial, real estate, and services.

The company, which designs and manufactures EVs, e-scooters, and e-buses, went public last August through a SPAC merger, providing it with approximately $1.5 billion in cash post de-SPAC, which will be used to expand the brand internationally. Earlier in the year, the company introduced its initial batch of cars to the US market using a direct-to-consumer (DTC) approach. However, in December, it announced its first dealership partner in North Carolina, indicating a hybrid sales strategy as it seeks to boost sales in North America.

The pivotal element in VFS’s expansion into North America is its facility in North Carolina, where construction began in July 2023. The facility is projected to become operative in 2025, starting with an initial capacity of approximately 150,000 electric vehicles per year. In comparison, VFS’s main facility in Vietnam boasts a capacity in the range between 250,000 to 300,000 EVs per year. The company anticipates an aggressive scaling of production driven by growing demand in both Vietnam and North America. Furthermore, VFS aims to extend its sales reach to around 50 global markets.

“Bottom line,” Lewis summed up, “while the EV market faced headwinds in 2023, forcing many OEMs to delay production, VFS’ founder backing and existing Asian footprint outside China should be key differentiators as global EV demand increases longer-term.”

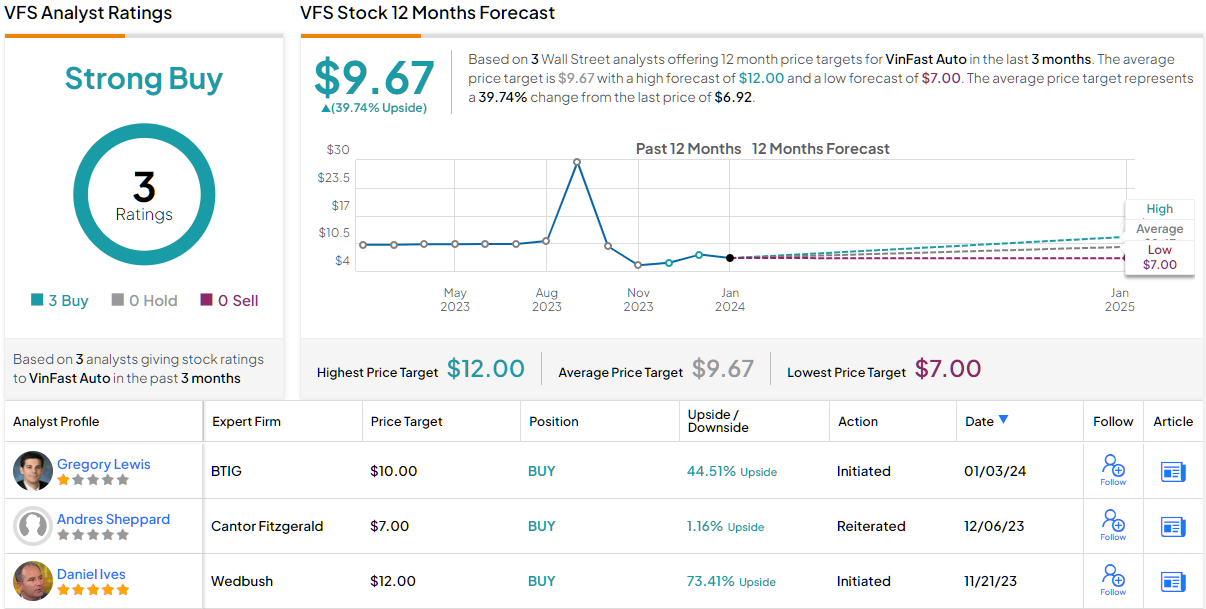

Accordingly, Lewis rates VFS stock a Buy, while his $10 price target suggests shares will climb 44% higher over the coming months. (To watch Lewis’s track record, click here)

2 other analysts have waded in with VFS reviews, and like Lewis, they are both positive, providing the stock with a Strong Buy consensus rating. At $9.67, the average target makes room for 12-month returns of ~40%. (See VinFast stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

.