Sales at Tiffany & Co. dropped less-than-expected as the US luxury jeweler experienced an uptick in revenue from China and benefited from strong e-commerce revenue.

In the three months ended Oct. 31, Tiffany’s (TIF) net sales dropped 1% to $1.01 billion, surpassing the Street’s consensus of $980.71 million. Sales in mainland China grew by over 70%, with comparable sales nearly doubling during the reported period versus the earlier year. Global e-commerce sales soared 92% in the third quarter year-on-year and represented 12% of total net sales in the year-to-date period, as compared to 6% for each of the last three fiscal years.

Tiffany, which recently agreed to be snapped up by French luxury goods giant LVMH, earned an adjusted $1.11 per share in the third quarter, exceeding analysts’ projections by 45 cents.

“We had a strong third quarter both in sales on a relative basis and terrific results in profitability on an absolute basis, which speaks volumes about the enduring strength of the Tiffany brand and gives us confidence as we enter the important holiday season,” Tiffany CEO Alessandro Bogliolo stated. “We look forward to surprising and delighting our consumers during the holiday season and the successful completion of the merger transaction with LVMH in early 2021.”

For the current fourth quarter, which covers the holiday season, Tiffany projects a mid-single-digit percentage decline in total net sales, compared to the 3% drop expected by analysts.

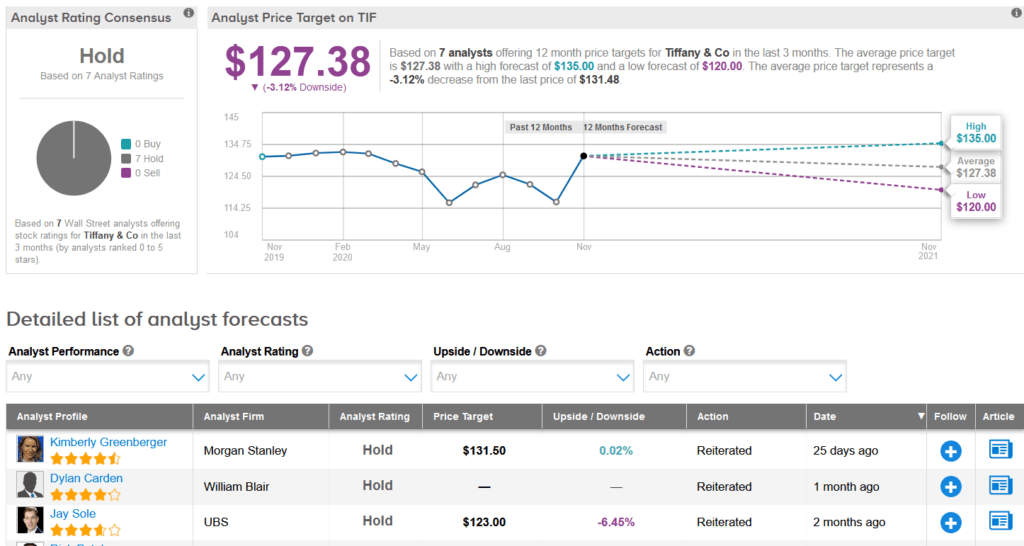

Shares in Tiffany have gained more than 7% over the past month, trimming this year’s decline to a mere 1.6%. Looking ahead, the average analyst price target stands at $127.38 and indicates 3% downside potential over the coming year.

Guggenheim analyst Robert Drbul recently reiterated a Hold rating on the stock, saying that the coronavirus pandemic has had an outsized impact on TIF’s tourism component and real estate exposure in urban areas.

Commenting on the LVMH deal, Drbul said he continues to view LVMH as a logical fit with strategic synergies.

The rest of the Street firmly shares Drbul’s stock outlook with a Hold analyst consensus backed by 7 unanimous Hold ratings. (See TIF stock analysis on TipRanks)

Related News:

Nike Ramps Up Its Dividend By 12%; Street Bullish

Foot Locker Tops 3Q Estimates; Shares Dip 5% On Covid-19 Woes

Shoe Carnival Gains As E-Commerce Sales Fuel 3Q Profit Beat; Analyst Raises PT