Quantum computing has subtly become one of the hottest investment sectors in finance over the past few months. Companies such as IonQ (IONQ), Rigetti Computing (RGTI), and D-Wave Quantum (QBTS) have strong growth prospects, but their stock valuations have overextended to secure any reliable long-term alpha. As a result of my valuation and risk analysis, I am primarily neutral on all three when considering their long-term prospects.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

IONQ Remains Speculative Despite Strong Operations

IonQ is a pioneering quantum computing company providing trapped-ion quantum computing that offers longer coherence times, high connectivity between qubits, and low error rates in quantum gates. Such ground-breaking functionality helps position the company to deliver reliable, versatile, and efficient quantum solutions, paving the way for commercial success and broader quantum adoption. However, I’m neutral on the stock because the quantum computing industry remains nascent and carries greater investment risk than established technology investments.

Equity dilution and unforeseeable operational risks are the main concerns investors will face with IONQ stock and most other quantum computing investments. As IonQ does not currently have any earnings, its reliance on equity financing means investors will be prone to equity dilution in the coming years to fund operations.

Patience Is The Key to Returns in Quantum Computing

Future equity dilution is the primary reason why the stock’s current trailing 12-month price-to-sales ratio of over 150 is concerning. Based on conservative revenue growth estimates, the Fiscal 2026 forward price-to-sales ratio is around 40, meaning that approximately two years of growth have already been priced in. As such, now may not be an opportune time to initiate a fresh position in the company.

However, despite the overarching risks, it’s still worth recognizing that IonQ is well-positioned in the quantum computing industry. It has a first-mover advantage with early success in delivering functional quantum systems. Therefore, long-term success is not improbable. The company has already established partnerships with major tech players like Amazon (AMZN), Microsoft (MSFT), and Google (GOOGL).

My forecast is that IonQ’s market cap will expand to $22.5 billion by December 2030, with 350 million shares outstanding, leading to an intrinsic stock price of around $19.50 when discounted over five years using the company’s weighted average cost of capital as the discount rate. As the stock currently trades at almost $37 per share, the implied margin of safety for investment is negative.

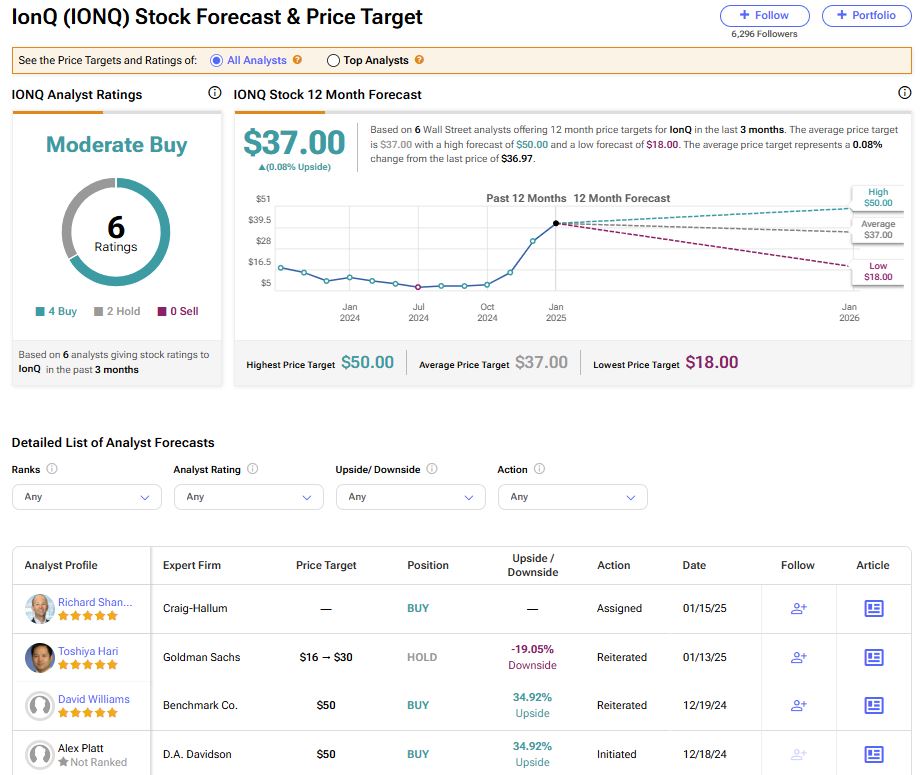

What Does Wall Street Say About IONQ?

On Wall Street, IONQ has a Moderate Buy rating, with the average IONQ price target being $37. This implies almost 0.8% upside potential over the next 12 months. This outlook is based on four Buy, two Hold, and zero Sell ratings. While this is positive, the low price target of $18 roughly aligns with my estimate of the stock’s current intrinsic value. Therefore, I am confidently neutral on IonQ.

RGTI Is Well-Positioned but Also Overvalued

Rigetti Computing is yet another avant-garde quantum computing company that may have overextended to the upside. As with IONQ, RGTI’s bloated valuation leads me to remain neutral on the stock. The company pioneered the development of Quantum Cloud Services, superconducting qubits, and modular architecture, allowing for scalable and accessible quantum systems. A modular approach allows Rigetti to scale efficiently by connecting smaller quantum processors into a larger system, thereby enabling the company to overcome current hardware limitations and build systems with more qubits while maintaining performance.

RGTI stock has also been subject to speculative market sentiment recently, but the valuation is somewhat more reasonable now. However, just like IONQ stock, the company’s next two years of growth have been priced into its valuation already. This was made evident by the company’s Fiscal 2026 forward price-to-sales ratio of nearly 50.

Estimating Fair Value

My analysis indicates that 50 and under is a solid barometer for estimating fair value for quantum computing stocks because they’re currently doubling their revenue growth rates year-over-year. Similarly, Nvidia (NVDA) achieved strong revenue growth in recent years, but its price-to-sales ratio never exceeded 50.

Based on the company’s current market position and net loss trends, it is expected to record its first profit around 2030. As such, equity dilution remains a concern for Rigetti shareholders. At around 400 million outstanding shares in December 2030 with revenues of $150 million, the revenue per share stands at $0.375. At a price-to-sales ratio of 45, the stock price is expected to hit $17 per share.

When discounting my December 2030 price target for Rigetti back to the present day using the company’s weighted average cost of capital as the discount rate, the implied margin of safety for investment is negative, at -13%.

What Does Wall Street Say About RGTI?

On Wall Street, the average RGTI price target is $6.10, based on six Buy, zero Hold, and zero Sell ratings. Therefore, the implied 12-month downside is a whopping 41%. In my opinion, this price target is too bearish but is more in line with my general price outlook on the industry due to valuation factors rather than Wall Street’s perspective on IONQ.

Smaller Market Share Indicates Better Growth Prospects for QBTS

Last but certainly not least, my analysis suggests D-Wave Quantum has the most optimistic long-term growth prospects because of its relatively smaller position in the sector compared to its peers. Given the underlying risks, I am still neutral on the stock, although QBTS remains better positioned than RGTI and IONQ, respectively. In contrast to these two companies, QBTS has a Fiscal 2026 forward price-to-sales ratio of just 26. Moreover, QBTS is expected to double its annual revenue growth rate in the next fiscal year.

D-Wave Quantum’s unique market position is related to quantum annealing, which finds the lowest-energy state of complex optimization problems. Additionally, the company’s proprietary cloud platform –Leap — integrates its quantum processors with classical computing infrastructure.

My valuation model for the company sees QBTS with around 375 million outstanding shares and annual revenues of $175 million by 2030, which entails a revenue per share of approximately $0.45 and a price-to-sales ratio of 45. Ultimately, this could translate into a higher stock price towards a fair value of $20.25 per share. The current stock price is $4.10, so the implied compound annual growth rate over five years would be 40%.

While this looks promising, I remain neutral on the stock because its rightful place is probably in a venture-style portfolio that includes other quantum computing stocks to offset risks related to operational challenges applicable to any one company. The total annual return of a portfolio yielding 30% for two quantum stocks and 5% for three quantum stocks yields a total five-year annualized return of just 15%.

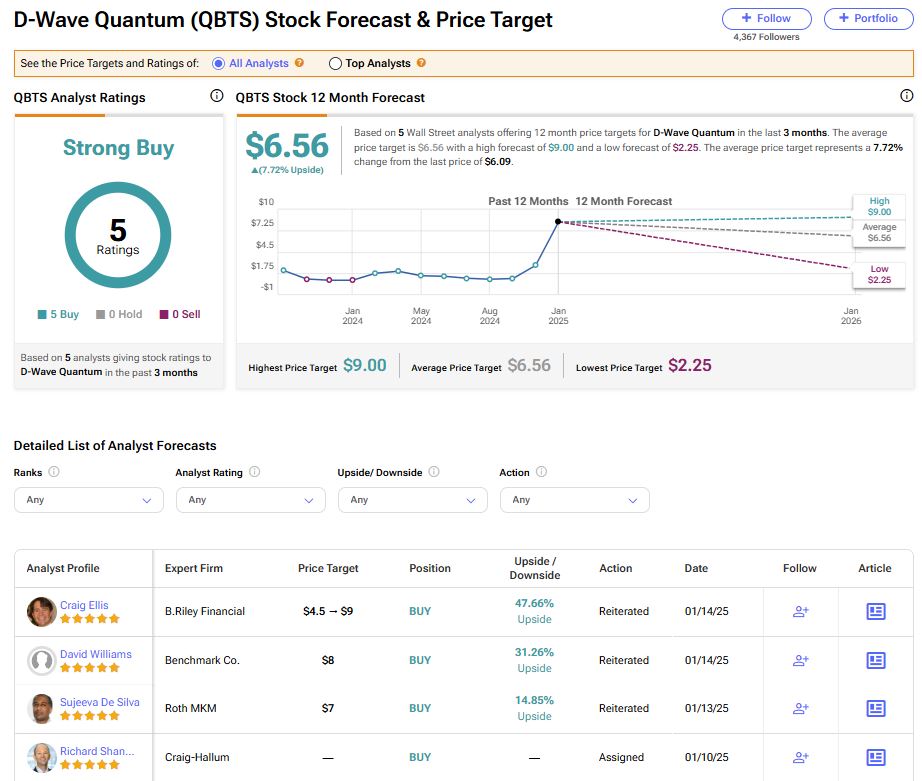

What Does Wall Street Say About QBTS?

On Wall Street, D-Wave Quantum has a Strong Buy rating, with the average QBTS price target indicating a 7.7% upside potential. This is based on five Buy, zero Hold, and zero Sell ratings. While this is very optimistic and reflects the valuation model I outlined above, I am still cautious due to uncertainty about how the market will develop and which companies will be able to sustain growth and command an enduring business model.

The Wisdom Behind Diversified Venture-Style Portfolios

When picking stocks in nascent industries with no clear winners (yet), it is wise to position capital tentatively while diversifying as much as possible to mitigate risk. In such a model, returns will likely gravitate towards a standard 15% annual return over five years or more. All three companies I have presented here are well-positioned in a novel, high-growth industry with superb long-term growth prospects, but none of the valuations are particularly appealing at current prices.