Thor Industries (NYSE:THO) is the world’s largest RV manufacturer. I’m bullish on Thor Industries because of its large buyback program and rebound potential. Also, the company’s huge discount to its private market value signals roughly 63% upside potential.

Why Thor Industries’ Earnings Should Rebound

After trading up to ~$129/share in March, Thor’s stock price collapsed by approximately 15% on its earnings release and revised 2024 guidance. I believe Thor is substantially under-earning on its trailing 12-month net income ($272 million). Last year’s industry shipments dropped by an even greater percentage than in the global financial crisis of 2008, indicating that we’re near the bottom of the cycle.

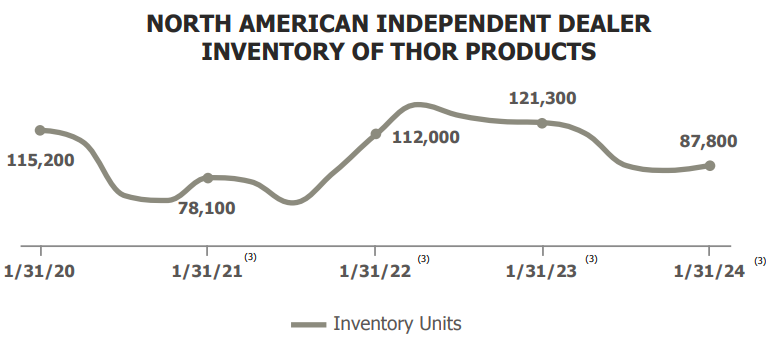

If customer inventories normalize or interest rates reverse, Thor’s net income could more than double (more on this below). Thor’s customers (the dealerships) have been digesting higher interest rates over the past two years and now have low inventories. Any reduction in interest rates, or even an acceptance of current interest rates, could cause dealerships to re-stock, sending Thor’s earnings higher.

Over the past 25 years, Thor’s average return on assets was 10.59%. These strong and sustained returns indicate that Thor has made solid capital allocation decisions. Despite this strong historical performance, I believe Thor paid a fairly premium price to acquire Erwin Hymer Group, the leading RV manufacturer in Europe, for an enterprise value of approximately $2.2 billion in 2019.

If we apply a 5% return on assets to Thor’s $2.2 billion acquisition of Erwin Hymer and 10.59% (Thor’s historical return on assets) to its remaining assets of $5.026 billion, we get normalized earnings of $642 million for the company. If this estimate proves correct, Thor’s earnings could rebound by more than 130% in the years ahead. At a market cap of $5.09 billion, this gives Thor Industries a normalized P/E ratio of 7.9x.

The Buyback Program Is Substantial

Thor Industries has been a serial acquirer, gobbling up smaller competitors to bolster its leading market share. However, in recent years, Thor has been acquiring its own stock instead. I believe these buybacks, which started in 2022, were made at very attractive prices and have increased the company’s intrinsic value.

Thor Industries has $461 million remaining on its share repurchase program. This is nearly 9% of Thor’s market cap. Because this expires in 2025, you have the potential for a 4.5% share repurchase per year. Combine this with the company’s 1.9% dividend yield, and you get a 6.4% annual shareholder return that is supported by Thor’s 12.2% normalized earnings yield. That’s what I like to see.

Thor’s Private Market Value

Famous investors Warren Buffett and Joel Greenblatt often focus on a company’s true, private market value — that is, what an acquirer would pay for the business. Then, Buffett and Greenblatt buy shares on the stock market at a large discount to that intrinsic value. So, what is a company like Thor Industries really worth? Let’s have a look.

Thor Industries’ founder Peter Orthwein, who was buying THO shares in late 2021 and early 2022 at prices between $98.54 and $103.41 (according to Barron’s), said, “I’ve been in the business since 1977, and we’ve acquired companies at six to seven times EBITDA [earnings before interest, taxes, depreciation, and amortization], sometimes even nine to 10 times.”

Now, Thor Industries is not just any RV company; it’s an integrated and diversified powerhouse with the largest global share. The company has been so resilient over the years that it even reported a profit in the depths of 2009. So, this is probably one of those companies that would command a 9x or 10x EV/EBITDA multiple. But to add a margin of safety, let’s just use an 8x multiple on Thor’s average EBITDA post-Tiffin and Erwin Hymer acquisitions.

Thor Industries has averaged $1.27 billion of EBITDA over the past three fiscal years. 8x this amount is $10.16 billion, which is my estimate of Thor’s private market value. This represents nearly 63% upside for THO, whose enterprise value is currently $6.245 billion.

For further clarity on what a business of Thor’s quality is worth, let’s look at Erwin Hymer Group. When Thor agreed to acquire Erwin Hymer in 2018, it estimated that the company’s EBITDA would be €235 million in 2018 and €300 million in 2019, for an average of €268 million.

Prior to some modifications, including the exclusion of the North American business, Thor initially agreed to pay an enterprise value of €2.1 billion ($2.4 billion) to acquire Erwin Hymer, so that was an EV/EBITDA of 7.8x. This is very close to the multiple we used to estimate Thor’s private market value.

Is THO Stock a Buy, According to Analysts?

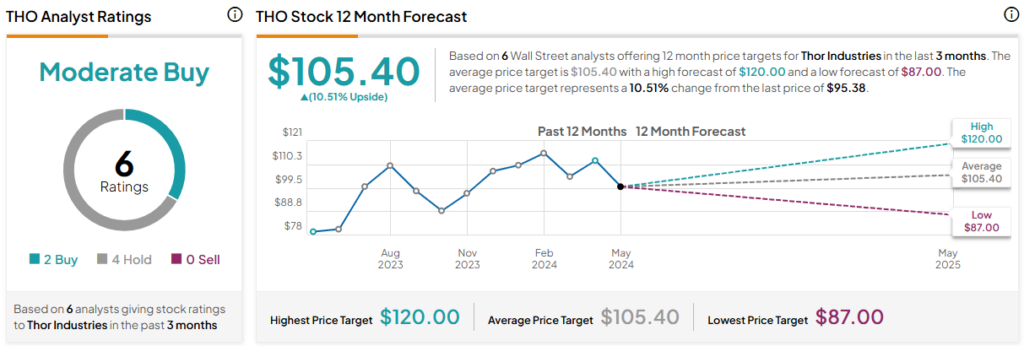

Currently, two out of six analysts covering THO give it a Buy rating, resulting in a Moderate Buy consensus rating. The average Thor Industries stock price target is $105.40, implying upside potential of 10.5%. Analyst price targets range from a low of $87.00 per share to a high of $120.00 per share.

The Bottom Line on THO Stock

Thor’s private market value represents 63% upside from its current price. I believe the company’s earnings are nearing a cyclical trough, with industry shipments down by their greatest percentage since 2008. Thor Industries has a track record of earning far more on its assets. Thus, my estimate of Thor’s normalized earnings is $642 million, and my estimate of its private market enterprise value is $10.16 billion.