As a variety of domestic and international factors continue to play out, the S&P 500 Index has dropped about 9.4% over the past month. Nonetheless, the market continues to present pockets of opportunity for savvy investors.

Despite a challenging environment, the TipRanks Analysts’ Top Stocks tool helps identify these key opportunities in the market. Let us take a look at two names in which Wall Street analysts see maximum potential.

Focus Financial Partners (FOCS)

Focus Financial is a partnership of independent, fiduciary wealth management firms that offers wealth management as well as other services. Focus’ partner firms maintain their independence while also benefitting from synergies and scale that come from joining hands with Focus.

In its latest fourth-quarter showing, Focus delivered robust performance owing to record M&A activity and strong partner firm results. Revenue rose 38% year-over-year to $523.9 million, beating expectations by $39.8 million. Earnings per share at $1.10, too, came in comfortably ahead of expectations by $0.07.

Importantly, in Q4, Focus closed 22 transactions, which included nine partner firm acquisitions and 13 mergers. By 2025, Focus is aiming to achieve a revenue of $4 billion, adjusted EBITDA of $1.1 billion, and an adjusted EBITDA margin of 28%.

Further, the company has been steadily expanding its footprint. Last week, it established its presence in Switzerland with the addition of Geneva-based wealth and investment management firm Octogone Holding. The move boosts Focus’ international presence and helps it enter multiple ultra-high net worth markets across the world.

Focus is expected to announce first-quarter results on May 5. Analysts expect the company to deliver EPS of $1.09 on revenues of $515.65 million.

RBC Capital analyst Daniel Perlin has reiterated a Buy rating on the stock alongside a price target of $75. Raymond James’ Patrick O’Shaughnessy too, has a Buy rating on the stock with a $60 price target.

While O’Shaughnessy sees a long growth trajectory for Focus, he expects the company to incur higher interest expenses, owing to the expected interest rate hikes.

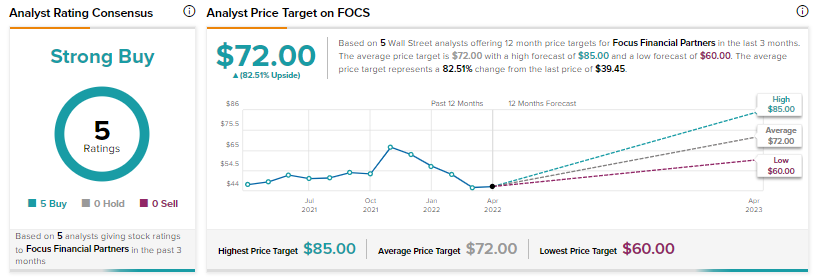

Overall, the Street has a Strong Buy consensus rating for Focus, based on five unanimous Buys. The average Focus price target of $72 implies a massive potential upside of 82.5% for the stock. That’s after a 35.5% slide in the share price so far in 2022.

The stock has a price/sales ratio of 1.89, implying investors can acquire shares in the company by paying $1.89 for each dollar of sales generated by Focus.

AppLovin Corp (APP)

The second name on our list, AppLovin, has also seen its share price decline by about 59.6% so far this year.

Its marketing software helps developers in marketing and monetizing their apps and growing their businesses.

In its most recent fourth-quarter showing, revenue surged 56% over the prior-year period to $793 million. Impressively, the number of Software Platform Enterprise Clients jumped 192% to 461 during this period.

Consequently, with an adjusted EBITDA growth of 60%, the company delivered a net income of $31 million as compared to a net loss of $19 million in the comparable year-ago period.

Importantly, last month, AppLovin extended its software platform capabilities to the connected TV space, with the $430 million acquisition of Wurl. The latter helps content companies to distribute streaming content to over 300 million TVs across the globe every month.

AppLovin is expected to announce first-quarter numbers on May 11. The street expects the company to post a net loss per share of $0.05 on revenues of $823.4 million.

Stifel Nicolaus analyst Scott Devitt has reiterated a Buy rating on the stock while decreasing the price target to $80 from $105. The lowered price target still implies a potential 109.7% upside!

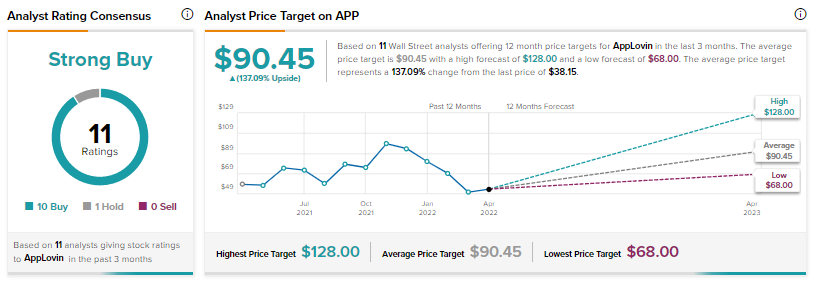

Overall, the Street has a Strong Buy Consensus rating on AppLovin based on 10 Buys and one Hold. The average AppLovin price target of $90.45 implies a potential 137.1% upside for AppLovin.

The stock has a price/sales ratio of 5.58. Moreover, both hedge funds and retail investors seem optimistic about the stock. Hedge funds have increased holdings in AppLovin by 9.6 million shares in the last quarter.

Further, Tipranks data indicates the number of portfolios holding AppLovin has increased by about 27.7% in the past 30 days.

Closing Note

After double-digit share price decline in both these names, a combination of robust sales growth, strategic acquisitions, and near 100% potential upside anticipated by analysts makes these two stocks compelling candidates for addition to investment portfolios.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure

Related News:

ServiceNow Shares Up 8% on Q1 Beat

Will Starbucks Stock Rebound on Q2 Earnings?

How Did Rivian Impact Amazon’s Poor Q1 Result?