We’re off the starting blocks in 2025 now, with the holidays behind us and another twelve months ahead, making this a perfect time to set up a well-balanced portfolio. The best investing approaches will include a variety of strategies: low- and high-risk, growth and value, momentum-driven plays, and passive strategies such as dividend investing.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

That last deserves a closer look. It’s usually seen as a defensive strategy, not a usual approach at a time of strongly rising markets – but dividends provide a steady income stream, which is a vital attribute for any investing strategy.

With that in mind, let’s explore some dividend stocks that encountered headwinds in 2024 but now appear attractive according to Janney Montgomery analyst Jason Stewart.

These dividend payers not only promise reliable income but also boast impressive yields starting at 14%. Let’s take a closer look, leveraging Stewart’s insights to uncover what makes them compelling investment choices.

Cherry Hill Mortgage (CHMI)

First up is Cherry Hill Mortgage, a real estate investment trust (REIT) that focuses its activities on building a diversified, hybrid residential mortgage portfolio. Since its founding in 2013, the company has invested in mortgage servicing rights (MSRs) and residential mortgage-backed securities (RMBSs), with the aim of providing its own shareholders with sound risk-adjusted returns plus additional opportunities for capital appreciation.

Cherry Hill has built its portfolio through multiple strategies. These include the acquisition of servicing-related assets by bulk purchase from mortgage servicers; the leveraged opportunistic acquisition and management of agency RMBSs; the purchase of both fixed- and floating-rate non-agency RMBSs; and effective hedging and risk management. The company announced this past November that it had completed its conversion to an internally managed REIT.

As a REIT, Cherry Hill is subject to tax regulations governing the return of profits directly to shareholders – and that is directly responsible for the company’s status as a dividend champ. REITs frequently use dividend payments as a vehicle for regulatory profit return compliance. Cherry Hill’s dividend history stretches back to the final quarter of 2013, and while the company has adjusted the payment as necessary over this period, it has never missed a quarterly payment.

In the most recent dividend declaration, made on December 12, Cherry Hill set a 4Q24 payment of 15 cents per common share. This dividend is scheduled for payment this coming January 31; at the current rate, the annualized payment of 60 cents per common share gives a forward yield of 23%.

The dividend is supported by Cherry Hill’s combination of earnings and assets. The company’s last reported quarter, the third quarter of 2024, showed non-GAAP earnings of 8 cents per share, as well as unrestricted cash reserves of $50.2 million. The company had a book value of $4.02 per share.

For Janney’s Jason Stewart, Cherry Hill shows a strong profile for dividend investors. The analyst sees the company in a position to keep delivering reliable results.

“CHMI employs an agency plus MSR investment strategy, which we expect will deliver superior risk-adjusted returns on a through cycle basis. In addition, the company recently completed a strategic review and internalized management of the company leading to alignment of interests with shareholders. We expect BVPS to be driven by the agency MBS portion of the portfolio near term with the MSR investment providing substantial cash carry. The company’s internal management structure is one of several factors that should drive earnings coverage of the dividend, and the overly discounted valuation makes for an attractive entry point,” Stewart opined.

To this end, Stewart rates Cherry Hill with a Buy rating, and his price target of $4 implies a runway toward ~53% upside for 2025. Based on the current dividend yield and the expected price appreciation, the stock has ~76% potential total return profile. (To watch Stewart’s track record, click here)

REIT stocks don’t always get a lot of analyst attention – they tend to fly under the radar. However, there are two reviews on file here and both are to Buy, making the consensus rating a Moderate Buy. CHMI shares are priced at just $2.62, with an average price target of $4. (See CHMI stock forecast)

Angel Oak Mortgage (AOMR)

Next on our list is another REIT, Angel Oak Mortgage. This is an externally managed company, and its real estate activities are focused on acquiring first-lien, non-QM loans, along with other mortgage-related assets, from the US real estate and mortgage scene. Angel Oak’s investments in these assets are directed at producing attractive returns for its own investors.

Angel Oak has built a portfolio based on a vertically integrated plan for both asset management and mortgage lending. The company has its hands in all aspects of this business, from sourcing and underwriting loans, to loan acquisition, to asset allocation and portfolio management, and it monitors its own performance to ensure that it creates a cycle of long-term gains for its investors and shareholders.

A key point that sets Angel Oak apart from its peers in the mortgage REIT landscape is its affiliation with the Angel Oak mortgage origination company. This affiliation allows the REIT to use an ‘originator model’ in its loan sourcing, rather than depending on purchasing or otherwise acquiring loans and mortgage assets from third parties in an aggregator model. Angel Oak reaps a number of advantages from this model, chief among them being greater accuracy in the company’s risk and return analyses.

Turning to the dividend, we find that Angel Oak last declared the payment on November 6, in the amount of 32 cents per common share. At the annualized rate of $1.28 per share, this dividend gives a robust yield of 14%. The company last paid out its dividend on November 27.

In 3Q24, the last period for which Angel Oak has reported results, the company saw a net interest income of $9 million, up 22% year-over-year. Also of interest, Angel Oak’s GAAP net income, at $31.2 million, came to $1.29 per share. The company did run a net loss when measuring distributable earnings, of 14 cents per share; this did not, however, stop the company from keeping up its dividend payment.

For analyst Stewart, in his coverage for Janney, the key here is that Angel Oak has a solid niche position.

“AOMR is attractively positioned as a leader in the non-QM space, which is expected to experience exponential growth over the next several years. The company has a well-structured balance sheet, solid credit performance, and the capacity and flexibility through its partnership with its affiliated lender to invest and expand with the growing non-QM market. Active rotation of the shareholder base has created a buying opportunity at the same time ROEs remain in the mid-double-digit range. We expect mid-single-digit growth in GAAP BVPS and multiple expansion toward economic BVPS,” Stewart stated.

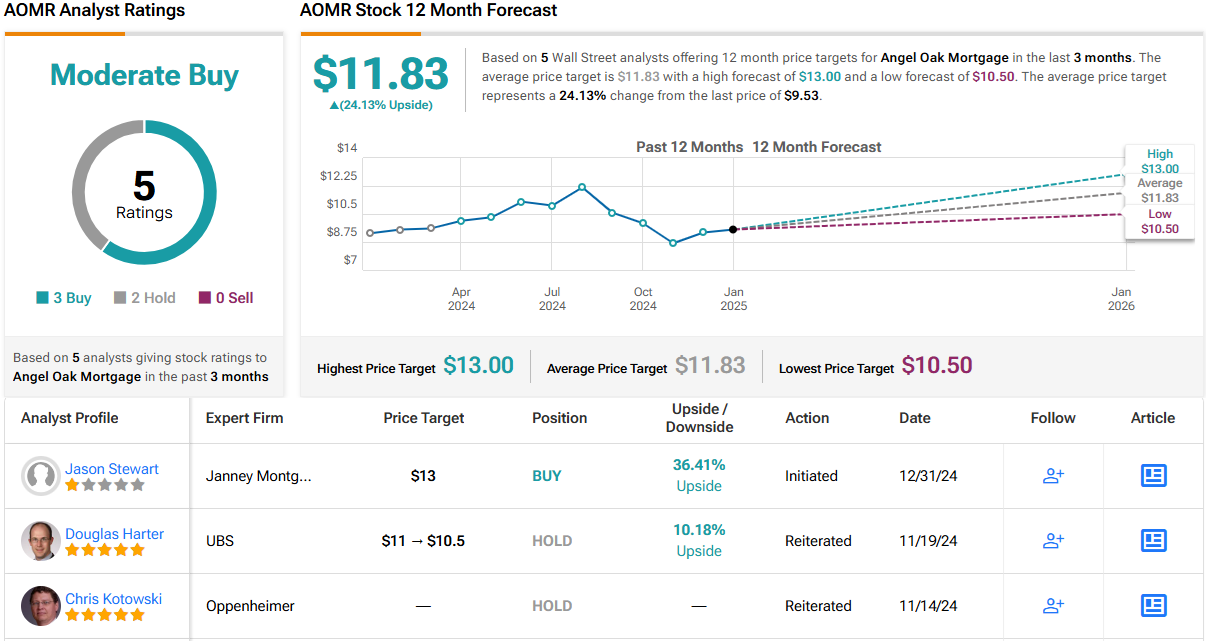

Saying that the best is yet to come for this stock, Stewart puts a Buy rating on the share. He complements that with a $13 price target, enough to suggest a 36% appreciation for the coming year. Taken together with the dividend yield, this stock’s total 12-month return may reach as high as 40%.

Overall, Angel Oak’s stock has earned a Moderate Buy consensus rating, based on 5 recent reviews that break down to 3 Buys and 2 Holds. The shares are priced at $9.53 and their $11.83 average price target implies a potential one-year upside of 24%. (See AOMR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.