Texas Instruments (TXN) sees third-quarter sales beating analysts’ expectations as the work-from-home environment continues to drive demand for the chipmaker’s products for personal computers, tablets and servers.

Texas Instruments projects current-quarter revenue will be in a range of $3.26 billion to $3.54 billion, which is above analysts’ expectations of $3.12 billion. Earnings are expected to be in the range of $1.14 to $1.34 a share compared with the 98 cents forecast by an average of analysts.

“We will maintain high optionality so we can continue to support customers’ demand, particularly during a time when their ability to forecast may continue to be limited,” said Texas Instruments CFO Rafael R. Lizardi. “We have informed our customers that lead times on our products remain short, and more than 40,000 products are available for immediate shipment on TI.com.”

In the quarter ended June 30, the chipmaker saw net income increasing to $1.38 billion, or $1.48 per share, from $1.31 billion, or $1.36 per share, a year earlier. Meanwhile, total revenue in the reported period, fell about 12% to $3.24 billion mainly due to a 40% drop in sales to the automotive sector. However, it beat analysts’ estimates of $2.94 billion.

Personal electronics was up over 20% sequentially and up about 10% compared to the same quarter to a year ago. “This can best be explained by work-from-home trends and TI being in a position to support unforecasted demand in second quarter,” the company said.

Texas shares gained as much as about 3% in extended market trading after declining less than 1% to $135.48 at the close on Tuesday.

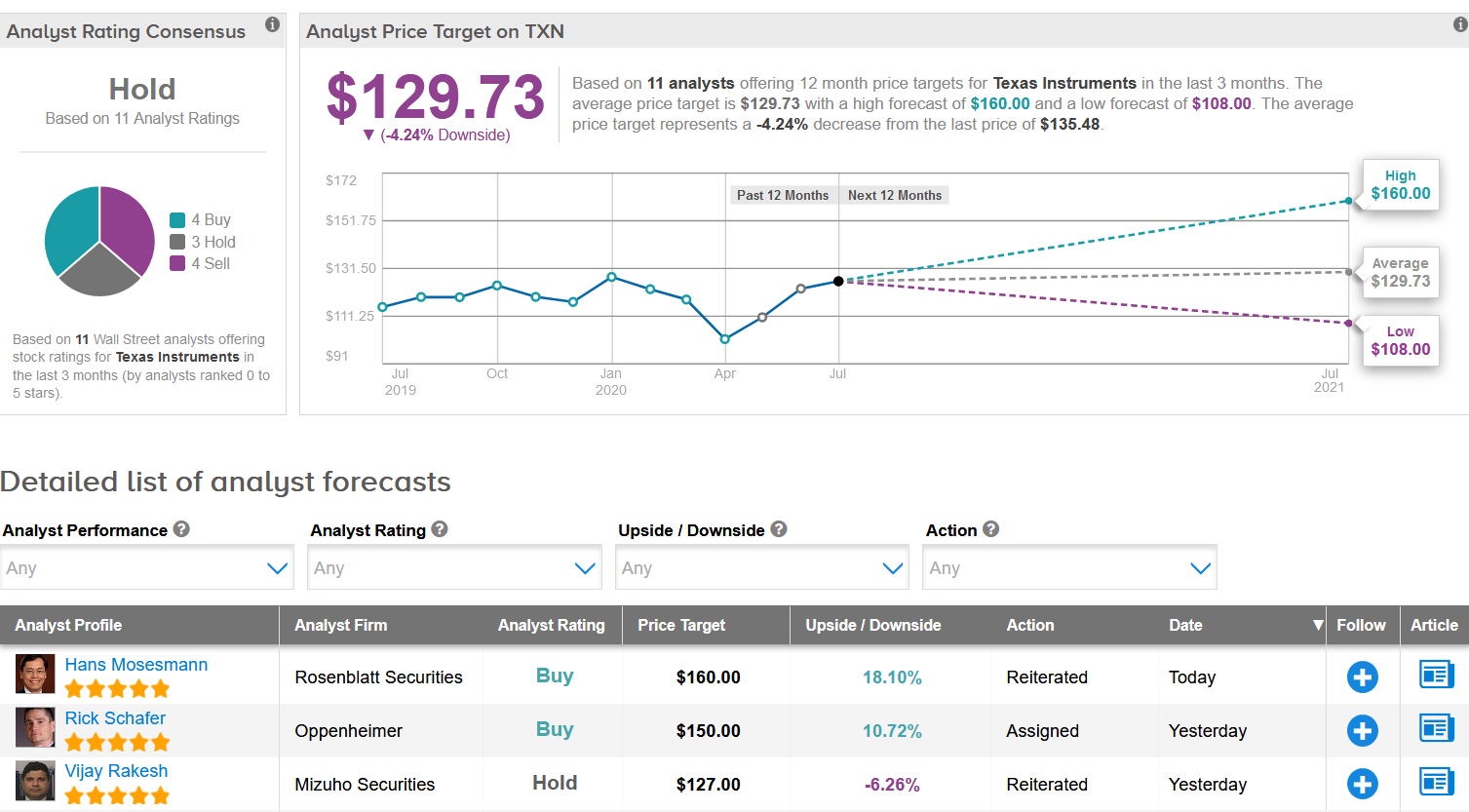

Following the financial results, Rosenblatt Securities analyst Hans Mosesmann raised the stock’s price target to $160 (18% upside potential) from $135 and maintained a Buy rating, saying that the company is the premier analog pure-play at a time when the semiconductor sector is in the early stages of a cyclical recovery

“Management’s posture of continued industry demand cautiousness while actively maintaining healthy inventories (distribution inventories continue to decline) to respond to un-forecasted demand (optionality), could disappoint some investors but this is just TI, being TI; prudently conservative,” Mosesmann wrote in a note to investors. “We like the setup into the back half of 2020 and for 2021 on TI being a much stronger company than in the past, excellent execution, and the TI.com go-to-market presence that we see continuing to lead to analog share gains over time, and also in embedded processing segments.”

The rest of the Street is for now staying on the sidelines when it comes to recommending the stock. The Hold analyst consensus is based on 3 Holds and 4 Sells versus 4 Buys. With shares up 5.7% since the start of the year, the $129.73 average analyst price target implies 4.2% downside potential in the shares over the coming year. (See TXN stock analysis on TipRanks)

Related News:

Logitech Ramps Up Annual Profit Outlook As Q1 Income Leaps 75%

Synaptics Snaps Up DisplayLink For $305M In All-Cash Deal; Top Analyst Lifts PT

IBM Pops 5% in Extended Trading After Quarterly Profit Beats Expectations