From Detroit’s Motor City to the bright lights of Hollywood, cars have always held a special place in American hearts. The automobile isn’t just a mode of transportation; it’s a powerful symbol of personal freedom and self-expression.

For investors, though, the automotive industry paints a more complex picture. Despite long-term demand, the sector is often buffeted by short-term challenges and market fluctuations, making it tricky to pinpoint the best auto stocks to invest in.

Recent trends highlight these challenges. While automakers enjoyed robust pricing power in recent years, consumers are now grappling with tighter credit conditions. Meanwhile, electric vehicles, spurred by social and governmental pushes, are not gaining traction with buyers as swiftly as many had anticipated.

Despite all of this, Deutsche Bank analyst Edison Yu is optimistic about the mid- to long-term potential of the US car market, noting, “High level, we see the US auto industry in the later innings of a cycle that is already showing signs of normalization after a post-pandemic surge but certainly by no means crashing as the American consumer has proven to be highly resilient. Unlike past cycles, the OEMs have followed through on generally adopting more discipline but we wonder if that can continue (to the same extent at least) in the midst of affordability dynamics and inventories creeping up.”

Against this backdrop, Yu has spotlighted two giants in the industry – Tesla (NASDAQ:TSLA) and Ford (NYSE:F) – offering a clear recommendation on which stock is currently the better buy. Let’s take a closer look.

Tesla

First up is the most recognized name in electric vehicles, Tesla. The leading industrial enterprise among Elon Musk’s portfolio of companies, Tesla is an American pure-play EV company founded wholly within the 21st century – and it has led the way for EVs in North America. The company started regular production runs for its vehicles back in 2008, and has been clearing profits since 2020. Tesla has long been recognized as one of the stock market’s driving forces, with a mega-cap valuation of $690 billion.

The company’s market cap value is worth a second look. The company is not just the world’s largest electric car maker, but it is the largest automotive company of any stripe. The second-largest car maker is Japan’s Toyota, with a market cap of $237 billion, or about one-third that of Tesla. Reaching this scale, in a new product market, has been a remarkable achievement for Musk’s auto company.

The key to Tesla’s success has been its core product, the electric vehicles. The company is known for its premium models, the Model Y, Model X, and Model S cars, and also has the popular, and lower-priced, Model 3 in production. The recently released Cybertruck generated a lot of buzz but sales have been soft, although it continues Tesla’s marketing habit of instant brand recognition. Together, these vehicles brought Tesla a total of $19.878 billion in revenue during the last reported quarter, 2Q24.

That was the bulk of Tesla’s revenue. With the company’s energy and services segments, total quarterly revenue reached $25.5 billion, beating the forecast by $760 million and growing 2.3% year-over-year. The company’s bottom line profit came to 52 cents per share, by non-GAAP measures. This EPS was down sharply from the 91 cents reported in 2Q23, and missed the estimates by 10 cents per share.

The y/y decline in earnings reflects the overall softness in the EV market right now, but it’s important to remember that Tesla is profitable, whereas most US makers simply are not. This gives Musk a great deal of flexibility in his business ventures, and he is taking advantage of that to build an agreement between his AI venture, xAI, and Tesla. The potential agreement would see xAI tap into Tesla’s revenues, while Tesla would benefit from access to cutting-edge AI tech to use in its development of autonomous vehicles, as well as its development of voice-activated in-car systems and even in the humanoid robot ‘Optimus’ program.

What all of this does is make Tesla more than just a car company. With multiple tech shots in the making, Tesla brings to the table several routes toward continued profits.

That has caught the eye of Edison Yu, and in his write-up for Deutsche Bank, the automotive sector expert says, “At the core, we do not see Tesla as an automaker but rather a technology platform attempting to reshape multiple industries, deserving of a unique type of valuation framework. Tesla structurally already has a big lead in BEVs, especially as it relates to scale/cost, and commands outsized brand value globally. Near-term, automotive deliveries/margin have indeed been softer but we view this as temporary ahead of new models/refreshes coming in the pipeline.”

“Long-term,” the analyst added, “Tesla is an emerging leader in autonomous driving (robotaxi) and humanoid robots (Optimus), in our view, which represent some of the most clear and lucrative applications of end-to-end AI. Furthermore, the energy storage business is already undergoing a major growth/margin inflection, set to generate +$13bn in sales in 2025E.”

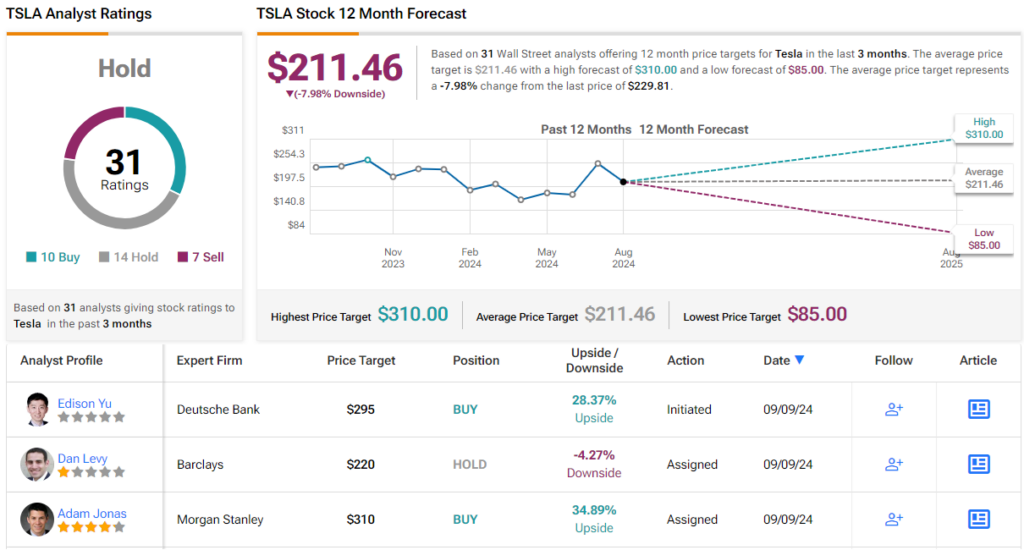

Quantifying his stance on Tesla, Yu rates the shares as a Buy. His price target, set at $295, implies that the stock will appreciate by 28% in the next 12 months. (To watch Yu’s track record, click here)

The rest of the Street, however, is not convinced that Musk’s empire is worth the risk. The 31 recent analyst recommendations break down to 10 Buys, 14 Holds, and 7 Sells, resulting in a Hold (i.e. Neutral) consensus rating. The share price outlook is cloudy, as the $211.46 average target price suggests it will slip 8% by this time next year. (See TSLA stock forecast)

Ford Motor Company

The second stock on our list is one of Detroit’s most venerable names, Ford Motor Company. Ford was one of the Motor City’s early leaders in the automotive industry and is best known for two innovations that transformed the early 20th century. First was the assembly line system, which changed the nature of factory work forever – and second was the famous Model T automobile, the first mass-produced car designed from the start to be affordable on the mass market.

Ford has evolved since the 1920s but has always kept an eye on what the car-driving public likes and wants. The company’s famous Mustang muscle car, which has been in continuous production since 1964, has always had a following, and Ford’s equally famous F-series pickup trucks – with lines designed for light, medium, and heavy-duty use – were first introduced in 1948. They are now in their 14th generation and have for decades been among the best-selling vehicles of any type in North America.

In recent years, Ford has made a strong push to develop and market EV models, including electric variants of its customer-favorite Mustang and F-150 vehicles. However, the company still runs a net loss on EVs, and while electric models are showing the strongest year-over-year gains in sales, they still make up a small fraction of the company’s total sales. In the last monthly sales numbers, for this past August, Ford listed sales of 182,985 vehicles of all types. Of that total, 8,944 were pure electric vehicles, and 16,394 were hybrid electric models. The remaining 157,647 vehicles sold were gasoline-powered, and of that total, more than 70,000 were F-series trucks. We should note, however, that hybrid vehicle sales led the year-over-year gains, with sales growing by 49.8% in August.

As for Ford’s Q2 financial results, the company reported $47.8 billion in revenue, with $44.81 billion coming from its automotive division – up 5.6% year-over-year but falling short of expectations by $70 million. The company’s earnings, 47 cents per share by non-GAAP measures, were down 25 cents from 2Q23 and were 21 cents per share below the forecast.

Pressures on the company included steep losses in the EV segment, the Ford Model E division. EVs saw quarterly revenues decline 37% year-over-year and realized a net loss of $1.14 billion. This was offset by consistent momentum with the redesigned F-150 pickup, along with record sales of the company’s Transit commercial van models.

While Ford is facing headwinds in the near term, the company’s proven longevity and its lineup of popular vehicles are assets that cannot be denied – and form the positive side of a decidedly mixed review from analyst Edison Yu.

“Ford represents a potentially compelling turnaround story longer term, in our view, albeit with near-term execution/timing risk. While Ford has done well to restructure money-losing operations overseas, Ford Blue in the US continues to have an inflated cost structure, dragging down overall profitability, while Ford Pro (commercial) puts up impressive results. Our sense is this reflects acute difficulty optimizing a massive entrenched organization. In particular, Ford’s warranty performance has been a headwind for years but should mechanically reverse as vehicle quality improves, enabling billions in cost savings to eventually flow through,” Yu opined.

For the near-term, however, Yu remains cautious, saying, “With so many moving parts, there is naturally tremendous execution risk in the next few years and we could see the stock facing material volatility along the way.”

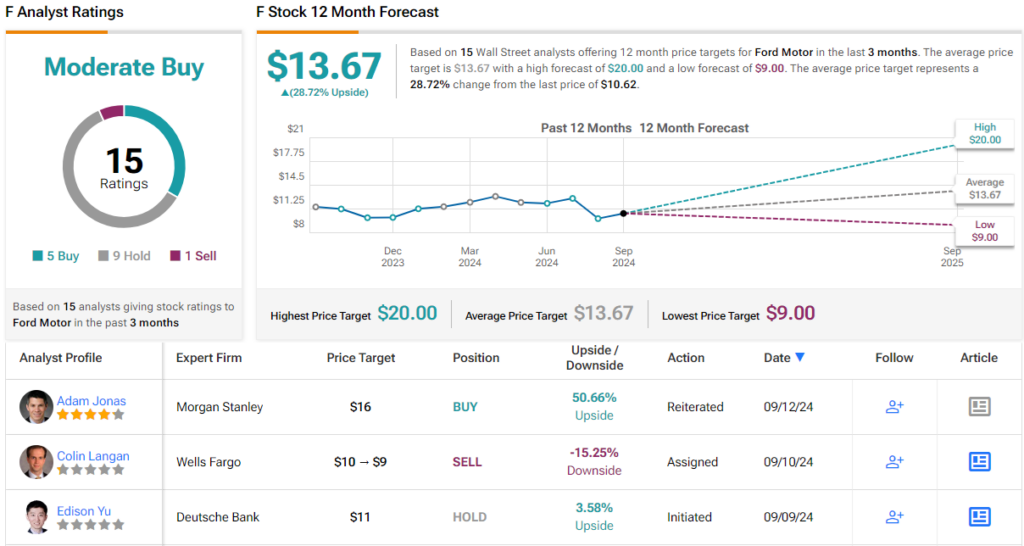

With this stance in mind, it’s no surprise that Yu rates Ford as a Hold (i.e. Neutral). His price target of $11 points toward a modest one-year upside of 3.5%.

The Street generally is a bit more upbeat on Ford. The stock has a Moderate Buy consensus rating, based on 15 analyst reviews with a breakdown of 5 Buys, 9 Holds, and 1 Sell. With an average target price of $13.67, Ford shares can claim a 12-month upside potential of just under 29%. (See Ford stock forecast)

In conclusion, Deutsche Bank clearly sees Tesla as the superior auto stock for investors at this time.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com