Tesla’s stock (TSLA) has rallied about 72% off of its April 2024 low as investors championed its Cybertruck, earnings, and upcoming Robotaxi event, which has since been delayed. I believe Tesla’s Robotaxi has been a flop and that autonomous taxis and EVs are far less practical than investors are pricing in. In 2023, hybrid sales outpaced EV sales, and Honda (HMC), of all companies, had better earnings growth than Tesla. Consequently, TSLA’s rally may be short-lived, and I am bearish on the stock.

Robotaxis Have Flopped and May Continue to Do So

Tesla’s Robotaxi hype has continued despite years of promises that haven’t come to fruition. For example, in 2019, Elon Musk said, “I feel very confident predicting autonomous Robotaxis for Tesla next year.” Fast forward to 2024, and Tesla’s full self-driving (FSD) cars still require constant driver supervision and occasional driver intervention. Some have even suggested that the newest version of FSD is getting worse, not better.

Meanwhile, Alphabet (GOOGL) and General Motors (GM) have autonomous taxis driving passengers around San Francisco without direct supervision. But their use has shown that Robotaxis aren’t all that practical.

Without driver supervision, passengers have been engaging in extracurricular activities, sometimes of the illegal variety, in the back seat. No one is present to prevent smoking within the vehicle or other vandalism to the vehicle. Also, these vehicles have been causing traffic jams and other problems and have been disabled by protesters putting pylons on the hoods.

Hybrid Vehicles and Competitors Are Gaining Share

Recently, hybrid vehicle sales have grown faster than EV sales in both the U.S. and China. In the U.S., “Hybrid sales rose 65% vs. a 46% gain for EV sales,” according to Investor’s Business Daily. Also, “Plug-in hybrid electric car sales in the first quarter [of 2024] increased by around 75% year-on-year in China, compared to just 15% for battery electric car sales,” according to the International Energy Agency. Why is this happening? Maybe because hybrids are more practical for most consumers.

On top of this, Tesla has been decreasing prices and struggling to maintain its market share lead, with BYD’s (BYDDF) revenue growth greatly surpassing Tesla’s over the past 12 months. Price wars are typical for the auto industry, where there are so many players. Tesla’s first-mover advantage in EVs is now gone, and its profit margins may be the next shoe to drop. This is probably just the beginning, with China producing extremely affordable EVs and nearly every automaker globally having an EV plan.

Tesla’s Net Income Is Overstated

To make matters worse, Tesla has managed to drastically overstate its net income by reporting a one-off $5.9 billion tax benefit in the 4th quarter of 2023. In the company’s latest annual report, Tesla reported the following: “In 2023, our net income attributable to common stockholders was $15.00 billion, representing a favorable change of $2.44 billion, compared to the prior year. This included a one-time non-cash tax benefit of $5.93 billion for the release of valuation allowance on certain deferred tax assets.”

So, what would Tesla’s PE ratio be without this one-off, non-cash tax benefit? Well, if we subtract this $5.93 billion tax benefit from Tesla’s trailing 12-month net income of $13.61 billion, we get $7.68 billion. Divide the company’s $764 billion market cap by this, and you get a PE ratio of 99.5x, similar to the company’s forward PE. This valuation is far too high, given everything that’s happening in the world with EVs and autonomous taxis.

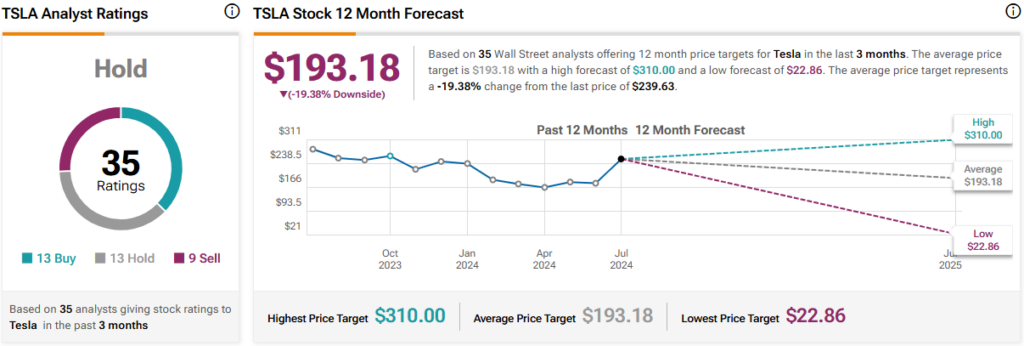

Is TSLA Stock a Buy, According to Analysts?

Currently, 13 out of 35 analysts covering TSLA give it a Buy rating, 13 rate it a Hold, and nine rate it a Sell, resulting in a Hold consensus rating. The average TSLA stock price target is $193.18, implying downside potential of 19.4%. Analyst price targets range from a low of $22.86 per share to a high of $310 per share.

The Bottom Line on TSLA Stock

Tesla’s net income is overstated due to a non-cash tax benefit. When we adjust for this, we can see the company’s earnings have come crashing down to earth as it tries to maintain its market share amid an influx of cheap Chinese EVs and surging competition from hybrids. Waymo and Cruise have achieved full autonomous taxi capability ahead of Tesla, but the prospects for autonomous taxis don’t look bright, with a flurry of problems emerging. At 99.5x adjusted earnings, TSLA’s rally may be short-lived.

Questions or Comments about the article? Write to editor@tipranks.com