The automotive industry has been an economic stalwart for over a century – and now the industry is in the midst of major changes. The changes are technological, in the nature of cars, and in the way that vehicle owners use their cars.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

The first change, embodied in the shift toward electric vehicles, is making the headlines. Billed as a cleaner future for the automotive sector, EVs have support from social pressures and government policies, and the car makers are responding with new designs and new models. But while electric vehicles may be hogging the attention, high-tech subscription services may have a greater long-term impact on the industry.

These subscription services are popping up at the connection between software, connectivity, and cars. Packages include features such as online mapping, remote vehicle control, and even hands-free driving. For the car makers, these services represent a new, higher-margin income stream; for the customers, they represent new ways to interact with the car.

Amidst these transformative waves, the tried-and-tested investment strategy in the automotive sector remains steadfast: investors should stick to the timeless wisdom of seeking out stocks that offer the best value for their investment.

That’s where analysts at Bernstein come in. They’ve pitted Tesla (NASDAQ:TSLA) against Ford (NYSE:F), the disruptor versus the stalwart, to find out which is the better bet in today’s market. Let’s see what they’ve uncovered.

Tesla

We’ll start with Tesla, Elon Musk’s flagship business – and currently the only US EV maker that’s turning a profit. Tesla has, in just over 20 years, risen from the start-up stage to boast a market cap over $560 billion – making it not just the world’s largest electric vehicle maker but the largest automotive company of any type. Tesla’s leading position in the EV industry is easy to sum up: the company was the first EV maker to scale up to full production, and the first to reach profitability.

Tesla first recorded those profits in 2020, and for the last seven consecutive quarters has reported revenues of at least $20 billion. This success has come on the heels of Tesla’s solid infrastructure build, including a network of high-tech factories producing high-quality vehicles that are meeting customer demand for performance and styling.

In addition to just building good cars, Tesla has also made connectivity a standard feature in every vehicle it sells. The basic service includes such features as music and media streaming, live traffic visualizations, and interactive maps. All Tesla cars have Standard Connectivity included for the first eight years of ownership; Premium level connections are available through paid subscriptions, which can be bought at any time through the car’s touchscreen.

This past April, Tesla released its numbers for first quarter vehicle production and delivery, as well as quarterly financial results. However, the numbers were met with some disappointment. Q1 production figures came in at 433,371 vehicles, down from the previous quarter’s approximate 495,000. Similarly, deliveries for Q1 totaled 386,810, a decline compared to the more than 484,000 vehicles delivered in Q4. Tesla listed several factors that contributed to the declines in production and deliveries, including arson at its Berlin Gigafactory, Red Sea shipping diversions due to the ongoing war in the Middle East, and idiosyncratic factors such as factory shutdowns and/or production ramps.

Those production numbers were the basis for the company’s Q1 earnings performance. Tesla’s total revenue came to $21.30 billion in 1Q24, down 8.5% year-over-year, while missing the forecast by $960 million. Bottom-line earnings, of 45 cents per share by non-GAAP figures, was 5 cents per share lower than had been anticipated, and was down 47% year-over-year.

Taking a closer look at the earnings results, Bernstein 5-star analyst Toni Sacconaghi noted, “While Q1 deliveries were disappointing, margins were not as weak as feared and CEO Musk pointed to new models over the next year. Investors also warmly cheered Tesla’s mapping partnership with Baidu. We do not believe Tesla can grow units in 2024 without taking a serious hit to free cash flow, and that any new models will likely be modifications to existing models.”

Getting into further detail, Sacconachi adds, “Autonomy in China remains very competitive, with XPeng and Huawei already giving away comparable offerings to Tesla’s FSD [Tesla’s Autopilot feature] for free. Our first-hand experience is that capabilities of leaders like XPeng and Huawei are similar to Tesla’s FSD today (Level 2+), while players like Li and NIO are not far behind. The functionality is often given away for free, and so we suspect Tesla may face low attach rates for FSD at its current level of pricing, and don’t see it as a material catalyst for sales in China.”

Quantifying his stance, Sacconaghi rates TSLA shares as Underperform (i.e. Sell), and his $120 price target implies the shares will depreciate ~32% in the next 12 months. (To watch Sacconaghi’s track record, click here)

Overall, Tesla gets a Hold rating from the analyst consensus, based on 33 recent analyst calls that include 9 to Buy, 15 to Hold, and 9 to Sell. As of now, TSLA is trading at $176.75, while its average target price of $174.60 suggests that its shares are expected to stay rangebound for the foreseeable future. (See TSLA stock forecast)

Ford Motor

We’ll now turn our attention to one of Detroit’s classic names, the Ford Motor Company. Ford’s reputation has been based on its domination of the pickup truck niche, with its light-, medium-, and heavy-duty F-series trucks, and for its famous muscle cars, embodied by the iconic Mustang. Ford’s F-150 pickup has long been recognized as a popular customer choice, and for decades has consistently been counted among the best-selling vehicles, of any type, in the US market.

Ford’s forays into EVs have included electric versions of both of these market-leading models, but even the Mustang and F-150 names have not been able to push the company’s EV segment into profitability. Sales are sound; per the April 2024 sales update, Ford’s EV sales were up 129% year-over-year, but Ford’s Model E unit, the electric vehicle segment, reported a loss of $1.3 billion in the first quarter of this year.

Turning to the overall Q1 earnings report, released at the end of April, we find Ford reporting $42.8 billion at the top line, beating the forecast by $1.3 billion. The company had non-GAAP earnings of 49 cents per share, 5 cents ahead of the estimates. While EVs were a loser, the company’s Ford Pro commercial segment saw 36% year-over-year growth, based in large part on demand for Super Duty trucks and Transit delivery vans. In addition, the company’s R&D-focused Ford Blue segment saw strong hybrid sales; these mixed combustion-electric vehicles are on track for 40% sales growth this year. Ford’s Maverick is the best-selling hybrid truck in the US market.

Of interest for tech-focused investors, Ford has Connected Services available for customers, on the subscription model. Services include connected navigation and theft recovery, as well as hands-free driving and electric charging network access. The services are designed to enhance the driving experience in any Ford vehicle, and to make regular software updates easy.

Initiating coverage of Ford for Bernstein, analyst Daniel Roeska paints a picture of a legacy company adapting itself to changing times.

“The iconic automaker continues to enjoy strong profits from one of the most concentrated and protected auto markets in the world (U.S. large SUV and large pickup trucks). The company is generating sufficient cash to fund its transition to electric vehicles and return cash to shareholders. Over the past few years, the company has quickly pivoted away from lower margin products (cars), restructured its company and business units, and focused its efforts on higher margin B2B sales (i.e. commercial vehicles, Ford Pro). While there is much more to do on electrification, we see management converging on a clear path forward that will expand the use of hybrid cars and significantly limit losses in the EV business,” Roeska opined.

Looking ahead, Roeska goes on to explain why Ford should continue to bring returns for investors: “We forecast 2024 results at the upper end of guidance, +15% ahead on consensus EBIT, and see significantly better results than in upcoming years (+18% ‘25e EBIT vs. consensus) driven by lower losses, and ultimately profits on electric vehicles. If you haven’t owned Ford lately – now is the time.”

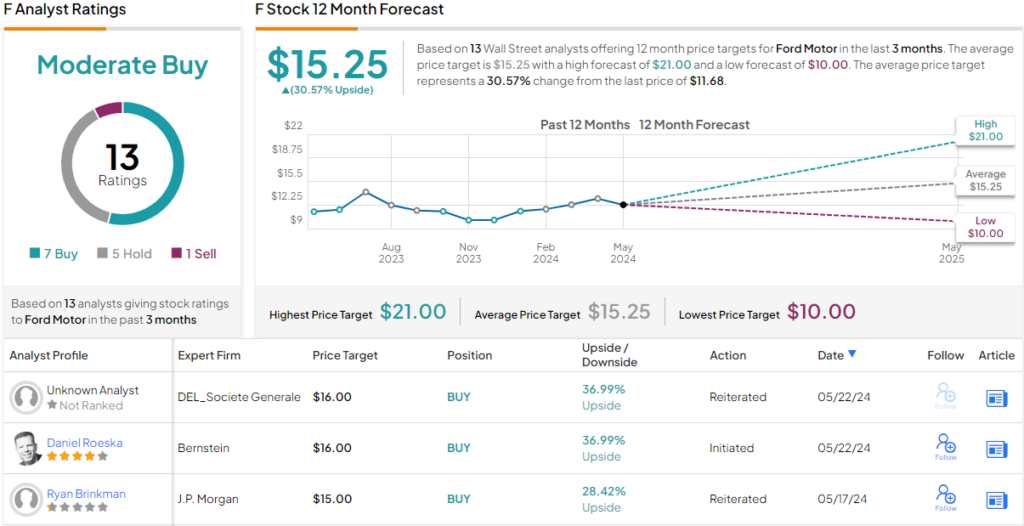

These comments support the analyst’s Outperform (i.e. Buy) rating on F, while his $16 price target points toward a 37% upside on the one-year horizon. (To watch Roeska’s track record, click here)

The rest of the Street’s projections for Ford indicate a split between the believers and the fence sitters. The stock’s Moderate Buy consensus rating is based on 7 Buys, 5 Holds (i.e. neutral), and 1 Sell. However, the bulls appear in the driving seat; going by the $15.25 average price target, shares will be changing hands for 30.5% premium, a year from now. (See Ford stock forecast)

Laid out together, it’s clear that for Bernstein, Ford is the superior automotive stock to buy right now. The company offers investors a broader base to support its operations, and is capable of compensating for shifts in the EV landscape.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.