Due in part to the adverse reaction spawned by the recently announced U.S. strategic crypto reserve, Terawulf Inc. (WULF) has seen its stock plummet -17% despite reporting a significant 102% year-over-year increase in revenue in 2024, rising to $140.1 million. The company also announced a successful self-mining of 2,728 Bitcoins, showcasing its robust capabilities in the Bitcoin mining sector. However, operational challenges and increased costs underscore key areas for caution. Terawulf highlighted its strategic growth with a 10-year data center lease agreement with Core42, projecting over $1 billion in revenue. This important development marks a milestone in the company’s ambitions in HPC hosting. As part of its diversification efforts, Terawulf has also ventured into the rapidly growing digital infrastructure market, backed by long-term customer agreements.

Making Significant Strides

TeraWulf specializes in creating and managing environmentally sustainable, next-generation data center infrastructure specifically intended for Bitcoin mining and hosting high-performance computing (HPC) workloads. The company’s primary source of income comes from Bitcoin mining, with most of its energy coming from zero-carbon sources such as hydroelectric and nuclear power.

The company has recently made significant strides in the digital infrastructure market. TeraWulf secured 72.5 MW of hosting capacity at Lake Mariner via long-term data center lease agreements with Core42. The company has also improved its digital infrastructure facilities at Lake Mariner to support this diversification, integrating advanced liquid cooling systems and Tier 3 redundancy to handle high-density compute workloads.

TeraWulf has seen a significant revenue increase of 102% for fiscal year 2024, reaching $140.1 million, up from $69.2 million in 2023. The boost in revenue is primarily due to a 129% increase in the average price of Bitcoin over the year, accompanied by an expanded mining capacity at Lake Mariner to 195 MW from 110 MW the previous year. Despite industry-wide challenges owing to Bitcoin halving and network hashrate increases in April 2024, the company managed to maintain robust mining margins by leveraging its low-cost and predominantly zero-carbon infrastructure.

At the end of 2024, TeraWulf held $274.5 million in cash, cash equivalents, and Bitcoin on its balance sheet. It had an outstanding debt of around $500 million related to convertible senior notes due in 2030.

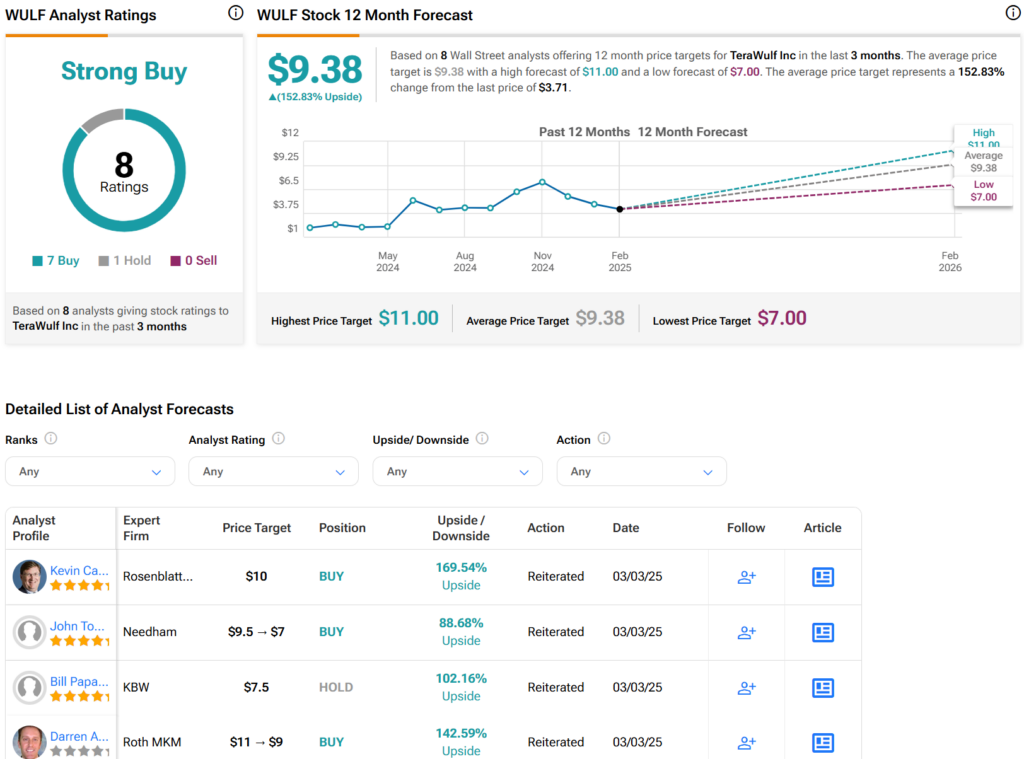

Analysts Remain Bullish

Analysts following the company have been mostly bullish on the stock. For example, Roth MKM’s Darren Aftahi has reiterated a Buy rating for the stock while revising the price target to $9 (from $11), noting the company’s recent updates and results have been “status quo.” This is attributed to the continuing holding of the Core42 deal at around 70MW, with further discussions for additional power. There has been a noted increase in costs, but if TeraWulf sustains the annual average power cost below $0.05/kWh, the mining results are expected to remain relatively stable.

TeraWulf Inc. is rated a Strong Buy overall, based on the recent recommendations of eight analysts. The average price target for WULF stock is $9.38, which represents a potential upside of 152.83% from current levels.