LMP Automotive Holdings, Inc. (LMPX) is an Ecommerce and facilities-based automotive retailer. In the long run, the company plans to profitably consolidate and partner with automotive dealership groups in the U.S.

LMPX has been on a dealership acquisition spree recently. Despite delivering a robust set of Q2 numbers, its shares have dropped 31.3% so far this year.

Let’s take a look at the company’s latest financials and understand what has changed in its key risk factors that investors should know.

Driven by sales from acquisitions, LMPX’s Q2 revenue increased $132.3 million year-over-year to $140 million.

The COO of LMPX, Richard Aldahan, said, “Demand continues to outpace supply for new vehicles. We expect this to continue into 2022 due to the pent-up demand from a large percentage of consumers who deferred their vehicle purchases in 2020, preferences for transportation due to the current suburban housing migration occurring, and component supply shortages within the manufacturing process.”

In Q2, LMPX’s gross margin expanded by 0.9% to 18.9%. Owing to acquisition-related expenses and operating expenses from acquisitions completed in the first half of 2021, the total operating expenses of the company jumped to $24.5 million, as compared to $0.96 million a year ago. Net income per share of the company came in at $0.86, as compared to net income per share of $0.03 a year ago. (See LMP Automotive stock chart on TipRanks)

Additionally, LMPX’s pipeline of dealership acquisitions remains active with the company aiming to reach 80 to 100 locations by the end of next year.

In the second half of fiscal 2021, the Chairman and CEO LMPX, Sam Tawfik, expects revenue of approximately $610 million and adjusted EBITDA of $44 million on an annualized basis.

Now, let’s look at what’s changed in the company’s key risk factors.

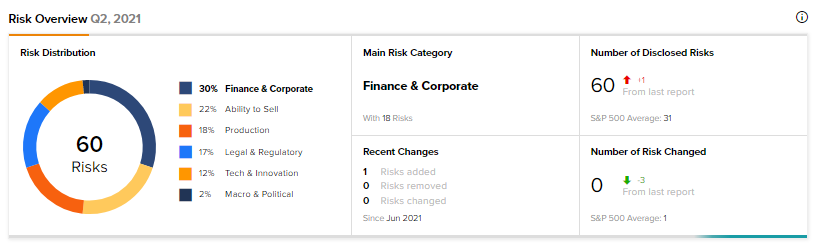

According to the new Tipranks’ Risk Factors tool, LMPX’s main risk category is Finance & Corporate, which accounts for 30% of the total 60 risks identified. Since June, the company has added one key risk factor under the Production risk category.

LMPX highlights that the success of its stores depends on vehicle manufacturers. LMPX relies on vehicle manufacturers for its new vehicle inventory; it depends on them for desirable product mix at the right time and at the right place to meet customer demand.

Vehicle manufacturers may be impacted by factors like economic downturns, recessions, or a decline in new vehicle sales or supply shortages. Such risks and disruptions could affect vehicle manufacturers and in turn impact LMPX’s ability to obtain or finance its desired new vehicle inventories.

Recently, there have been global shortages of automotive microchips, and a prolonged shortage of new vehicle inventory could mean lower new vehicle sales and lower gross profit for LMPX.

This shortage has resulted in higher demand for used vehicles. This means higher revenue and gross profit per used vehicle for LMPX, along with higher costs of acquiring used vehicles.

Additionally, any bankruptcy of a major vehicle manufacturer may cause LMPX to incur impairment charges related to inventory, fixed assets as well as intangible assets related to certain franchisees. Such an event could negatively impact LMPX’s results of operations and its financial condition.

The Production risk factor’s sector average is at 12%, compared to LMPX’s 18%.

Related News:

Dynatrace Buys SpectX; Shares Rise 2%

L3Harris Wins U.S. Air Force Robots Contract Worth $85M

Regeneron Signs Third COVID-19 Drug Supply Agreement with U.S. Government