A Sysco (SYY) subsidiary, namely Sysco Hampton Roads Inc, has been awarded a $805M contract from the US Defense Logistics Agency.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

It is a five-year, fixed-price contract with economic-price-adjustment, indefinite-quantity contract for full-line food distribution.

According to the statement, the contract performance will take place in Virginia, with a Sept. 20, 2025, ordering period end date. Using military services are Air Force and Navy, says the US Department of Defense.

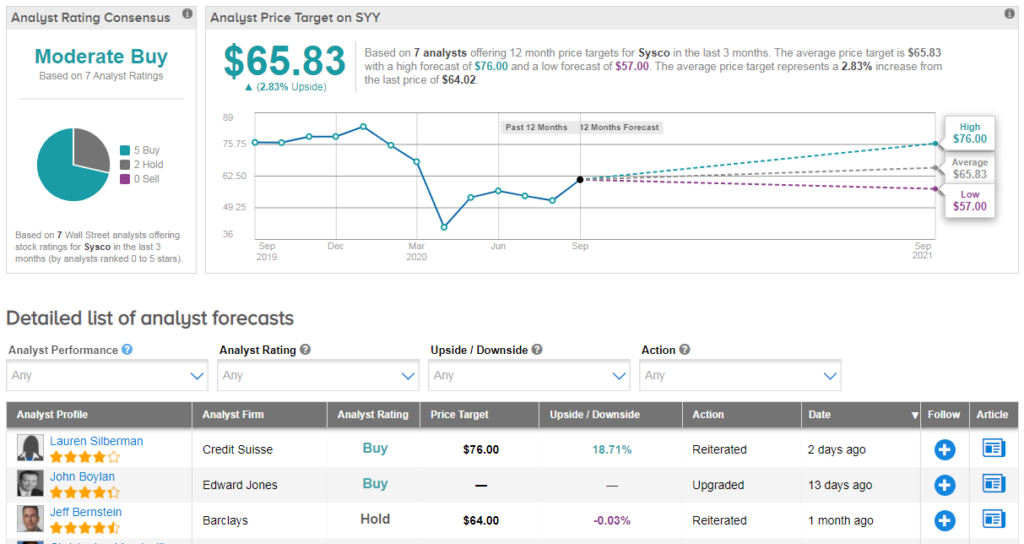

Shares in Sysco have plunged 25% year-to-date, and the stock scores a cautiously optimistic Moderate Buy Street consensus. In the last three months, 5 analysts have published buy ratings vs 2 hold ratings.

That’s with an average analyst price target of $66, indicating marginal upside potential from current levels.

However in a positive signal, Credit Suisse analyst Lauren Silberman has just reiterated her SYY buy rating while ramping up the price target from $65 to $76 (19% upside potential).

“As the largest competitor in US foodservice distribution, we believe recent challenges present a unique opportunity for the market share leader as customers seek suppliers they can trust will have the appropriate scale, capital and agility to meet needs in a dynamic environment” she explained.

Silberman believes that the temporary (and permanent) closure of smaller food distributors that lack capital should be a tailwind to attract new customers to SYY- and increase awareness of the breadth and quality of product offerings.

Management appears to be increasingly focused on accelerating SYY’s pace of growth, she says, while new CEO Kevin Hourican’s experience in supply chain should help execute cost savings activities.

“SYY offers the best margin profile relative to peers and we expect the company to continue to leverage its scale to approach ~5% EBIT margins over time” states Silberman. As a result, the analyst models FY22 sales down ~1%, FY22 EPS down ~5% and FY22 EBITDA up ~2.5% relative to FY19 levels. (See SYY stock analysis on TipRanks)

Related News:

Tesla Sinks 7% As Battery Day Falls Flat; Analyst Sees Buying Opportunity

Walmart Partners With Goldman To Offer Marketplace Sellers Credit

Nvidia Issues Mea Culpa Over Bungled GeForce RTX 3080 Launch