Tesla (NASDAQ:TSLA) investors received an early Christmas gift, unwrapped with the surge of enthusiasm following Trump’s election win. The stock has soared by 91% since then, driven by the perception that the Elon Musk-led company could benefit from the new administration’s favorable policies.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Mizuho analyst Vijay Rakesh sees a strong likelihood of this scenario playing out, citing “idiosyncratic tailwinds” that are expected to support the EV giant over the next four years.

Among these, Rakesh points to opportunities arising from a loosening regulatory framework for autonomous driving, which should provide additional upside for the valuations of its FSD and Robotaxi endeavors. The 5-star analyst notes that Tesla’s autonomy software is advancing toward broad commercialization, reckoning that FSD will achieve Level 4+ approval by 2025, with EU approval expected by 2027, potentially generating licensing revenue.

While Rakesh is bullish on the opportunities here, it’s interesting to note that his forecasts are far below Tesla’s expectations. For instance, on robotaxis, while Tesla has projected 2-4 million units per year, Rakesh is assuming only 207,000 Cybercabs in 2030, which is approximately 93% lower than Tesla’s forecast and below industry estimates, such as the Insurance Institute for Highway Safety’s projection of 4.5 million self-driving vehicles by 2030.

Likewise, for humanoid robots, Tesla is assuming 10 billion units by 2040, but the analyst is projecting Tesla to produce approximately 7.2 million robots, a huge 99% reduction. By 2030, Rakesh expects around 3 million robots, compared to industry estimates of around 7 million.

Nonetheless, Musk’s close relationship with the Trump administration could provide Tesla with a distinct advantage, ensuring “favorable legislative exposure.” This, combined with other positive factors, strengthens Tesla’s outlook. For instance, the setup for EV deliveries in the first half of 2025 looks promising due to favorable year-over-year comparisons. Additionally, the possible expiration of the U.S. EV lease credit between 2025 and 2026 might position Tesla more favorably than legacy and other EV manufacturers, who often rely heavily on leased vehicles.

As mentioned, deregulation could further accelerate the progress of FSD and Cybercab initiatives, while import tariffs on vehicles from regions like the EU, APAC, Latin America, and Canada might enhance Tesla’s competitive edge. Moreover, with auto production ramping up in 2026–2027, Tesla is poised to outpace both ICE and EV competitors, thanks to models like the Cybercab and Model Q.

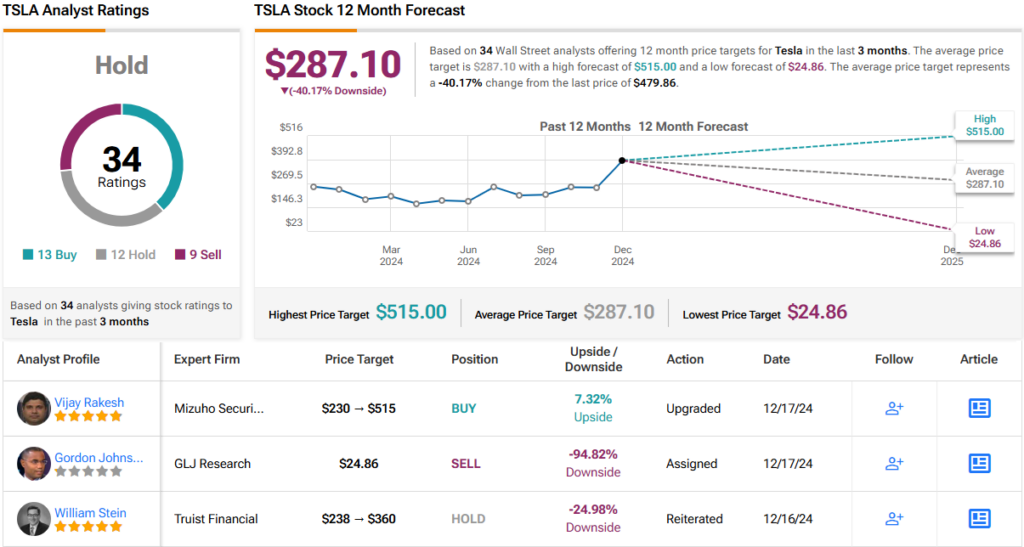

So, down to the nitty-gritty – what does all this mean for investors? Rakesh not only upgraded his rating on TSLA from Neutral to Outperform (i.e., Buy) but also raised his price target from $230 to $515, implying an 11% gain for the stock in the coming months. (To watch Rakesh’s track record, click here)

The other 33 recent analyst reviews on TSLA are evenly split between 12 Buys and 12 Holds, with an additional 9 Sells. This results in a consensus rating of Hold (i.e., Neutral). However, it could just as easily be interpreted as a Sell, considering the $287.10 average price target implies a 40% decline over the next 12 months. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.