New York-based shoes and fashion accessories firm Steven Madden (SHOO) reported strong second-quarter 2021 financial results driven by growth in all business segments.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

The company designs, makes and sells apparel, footwear and accessories for men, women and children under the brands Mad Love, BB Dakota, GREATS, Blondo, Betsey Johnson, Dolce Vita and Steven Madden.

Adjusted earnings per share totaled $0.48, beating the Street’s estimate of $0.30. Steven Madden had reported a loss of $0.19 per share in the same period last year. Quarterly revenue surged 178.6% year-over-year to $397.9 million, exceeding analysts’ expectations of $371.69 million.

Revenue from the wholesale business increased 162.2% year-over-year to $262.1 million, and Retail revenue climbed 220.6% to $132.7 million. (See Steven Madden stock chart on TipRanks)

The Chairman and CEO of Steven Madden, Edward Rosenfeld, said, “Looking ahead, while the environment remains volatile, we are confident that the strength of our brands and momentum in our business positions us to drive revenue and earnings growth in the back-half of 2021 and beyond.”

For 2021, the company expects revenue growth of 43% to 47% year-over-year, and adjusted EPS to be in the range of $2 to $2.10.

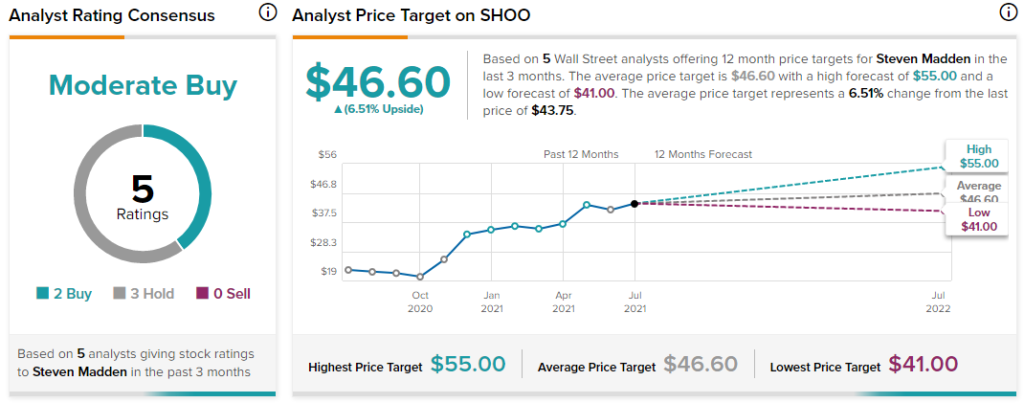

Last month, BTIG analyst Camilo Lyon reiterated a Buy rating on the stock with a price target of $55 (25.7% upside potential). The analyst had expected Steven Madden to report EPS of $0.27 in the second quarter.

Overall, the stock has a Moderate Buy consensus based on 2 Buys and 3 Holds. The average Steven Madden price target of $46.60 implies 6.5% upside potential to current levels. The company’s shares have gained 92.8% over the past year.

Related News:

Chefs’ Warehouse Reports Quarterly Profit; Shares Pop

General Dynamics’ Q2 Profit Exceeds Estimates; Revenue Disappoints

Loblaw’s Profit Rises 122% in Q2