Once upon a time, Intel (NASDAQ:INTC) was the go-to chip stock, but those glory days are a distant memory. The company’s fall from grace is so severe that, even in a year when the semiconductor industry is thriving (with the SOX index up 20% year-to-date), Intel’s shares have crashed by an abysmal 60%.

However, for those wondering if now might be the time to pick up some shares of this legacy heavyweight at a serious discount, Danil Sereda, a 5-star investor ranked in the top 3% of TipRanks’ stock experts, would like a word.

“Despite Intel’s efforts in restructuring and new product launches, I see no immediate end to the headwinds,” says Sereda, who has now downgraded his rating on INTC from Buy to Hold (i.e., Neutral). (To watch Sereda’s track record, click here)

Intel’s problems are myriad, as was evident in its recent disastrous Q2 readout. There were disappointments galore, with misses on almost every important metric, from revenue to profitability while a worse-than-expected outlook only offered more fodder for the bears. Sereda was not impressed, either, noting management’s “pessimistic Q3 guidance and ongoing challenges from competitors like AMD, Nvidia, and TSMC suggest a tough road ahead for Intel.”

Of course, it’s not as if Intel is unaware of these issues; its restructuring efforts are targeting profitability and capital efficiency improvements exceeding $10 billion in 2025, primarily off the back of reductions in OPEX, COGS, and CAPEX. The plan includes also slashing the workforce by more than 15%.

Yet, on the plus side, Intel is close to completing its “five nodes in four years” initiative, with the Intel 20A product set to begin production ramp-up in the second half of 2024. “On the other hand,” says Sereda on the matter, “it’s far from certain that this initiative will help INTC to stand out among its peers.”

Additionally, the company’s ambitious foundry plan includes becoming the world’s second biggest external foundry by 2030, but Sereda thinks Intel’s overall business model has “some vulnerabilities that could limit its growth and profit margins,” while it faces a big struggle trying to compete with TSMC.

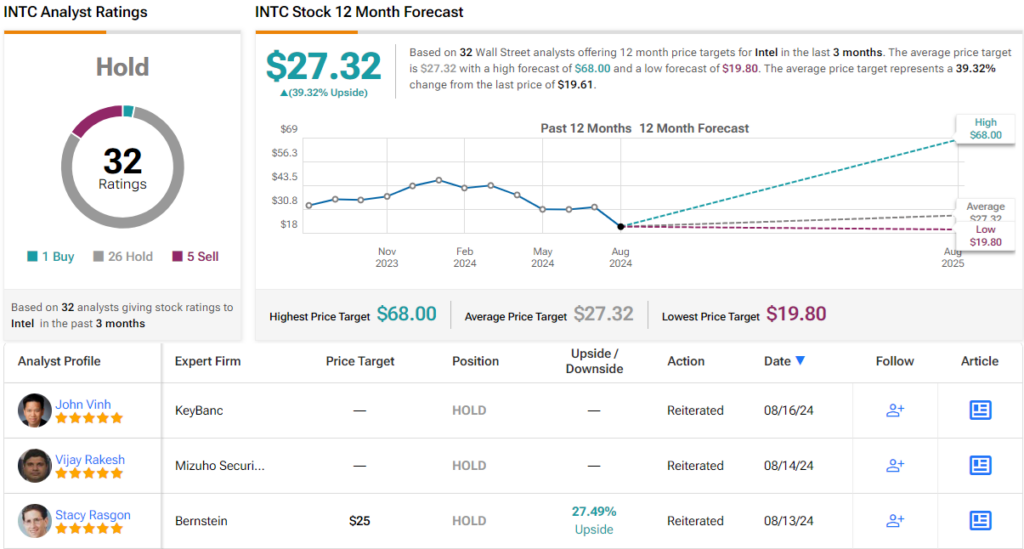

So, Sereda’s recommendation is to hold off for now, a sentiment that aligns with the broader consensus on Wall Street. Currently, 26 analysts remain on the fence with Hold ratings, far outweighing 5 Sells and a solitary Buy, culminating in an overall Hold consensus. However, there’s a twist: the average price target of $27.32 suggests that many believe the stock has been overly punished, implying potential one-year returns of ~39%. (See Intel stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.