Shares in Starbucks (SBUX) popped 6% in Tuesday’s after-hours trading after the company reported a solid earnings beat. Specifically, Q3 Non-GAAP EPS of -$0.46 beat Street estimates by $0.15 while GAAP EPS of -$0.58 also beat by $0.05.

Meanwhile revenue of $4.22B topped analyst estimates by $80M. This was despite falling 38% year-over-year- primarily due to lost sales related to the COVID-19 outbreak.

Similarly comparative sales growth of -41% was also better than the consensus expectations going into the print of -42.2%. This was driven by a 51% decrease in comparable transactions, partially offset by a 23% increase in average ticket

“We are pleased to share that the vast majority of Starbucks stores around the world have reopened and our global business is steadily recovering” commented Kevin Johnson, Starbucks CEO.

He continued: “We firmly believe that we are well positioned to regain the positive business momentum we had before the pandemic began and look forward to reigniting our ‘Growth at Scale’ agenda.”

Indeed, SBUX opened 130 net new stores in Q3, yielding 5% year-over-year unit growth, ending the period with 32,180 stores globally, of which 51% and 49% were company-operated and licensed, respectively.

However, Starbucks Rewards loyalty program active members fell 5% year-over-year in the US to 16.3 million due to Covid-19 related temporary store closures.

Looking ahead, Starbucks is now expecting global comparable store sales declines of 12% to 17% for each of Q4 and full year (vs previous guidance of declines of 10% to 20% for Q4 and full year).

That’s alongside a consolidated revenue decline of 10% to 15% for Q4 with Non-GAAP EPS in the range of $0.18 to $0.33 for Q4 and $0.83 to $0.98 for full year.

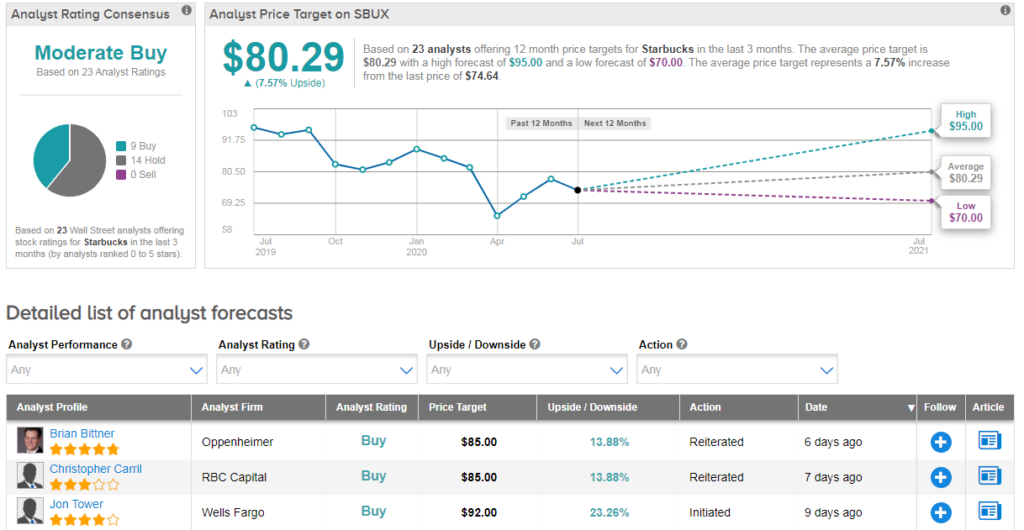

Overall analysts have a cautiously optimistic Moderate Buy consensus on the stock. Their average price target stands at $80- and with shares down 15% year-to-date, this indicates upside potential of 8%. (See SBUX stock analysis on TipRanks).

“While SBUX’s long-term positioning remains attractive, we continue to see a clear downside path to Street estimates through 2021 and are forced to remain patient in pitching the stock” writes Oppenheimer analyst Brian Bittner.

“A primary issue is consensus assumes store-level volumes in ’21 rise above the ’19 peak, despite lingering headwinds such as: disrupted morning routines, elevated unemployment and reliance on high customer frequency” he added. The analyst has a hold rating on the stock and $85 price target.

Related News:

Amazon Shares Rise As Analysts See More Upside

Visa Pulls Back On Revenue Miss; RBC Reiterates Buy Call

Verizon (VZ) Stock Looks Attractive After Earnings, Says 5-Star Analyst