Coffee chain Starbucks (SBUX) is witnessing continued activist drama as two hedge funds, Elliott Investment Management and Starboard Value, are making moves to boost the company’s performance. Elliott, which has already taken a sizeable stake worth $2 billion in Starbucks, is pushing for a board seat. Meanwhile, last week, the Wall Street Journal reported that Starboard has taken a stake in the coffee chain. However, the exact details remain unknown at the moment. SBUX shares rose 2.6% yesterday on news of Starboard’s stake.

Activist investors are known to bring about major leadership changes to enhance a company’s sales and share price performance.

Starbucks stock is under pressure as macro headwinds, competition from local outlets, and resistance in Chinese markets are weakening the company’s sales. Notably, SBUX shares have lost 18.7% of their value so far this year. The company is implementing a turnaround strategy that involves a three-part action plan. To restore lost ground, Starbucks seeks to expand its stores, invest in its digital ecosystem, and enhance its supply chain.

Elliott Wants Board Seat

Elliott has been clear that it wants representation on Starbucks’ board. Reports suggest that the directors of the two entities met last week to discuss a settlement. As part of a potential settlement, Elliott’s Managing Partner Jesse Cohn is reportedly expected to take a board seat at Starbucks. The settlement will also allow SBUX CEO Laxman Narasimhan to retain his role and a board seat. Further, board expansion and governance improvement remain key points of the potential deal.

Another key player in the story is Howard Schultz, Starbucks’ Chairman Emeritus, who still owns a majority stake in the company. Schultz is reportedly said to be opposing a deal with Elliott.

Starbucks’ Woes Deepen

Starbucks reported disappointing results for Q3 FY24, with revenues significantly missing estimates. Meanwhile, earnings per share (EPS) came in line with expectations. Global comparable store sales fell 3% year-over-year owing to a lower number of orders processed, which offset higher average prices per order. Importantly, comparable sales from China, one of Starbucks’ major markets, fell 14% compared to Q3 FY23.

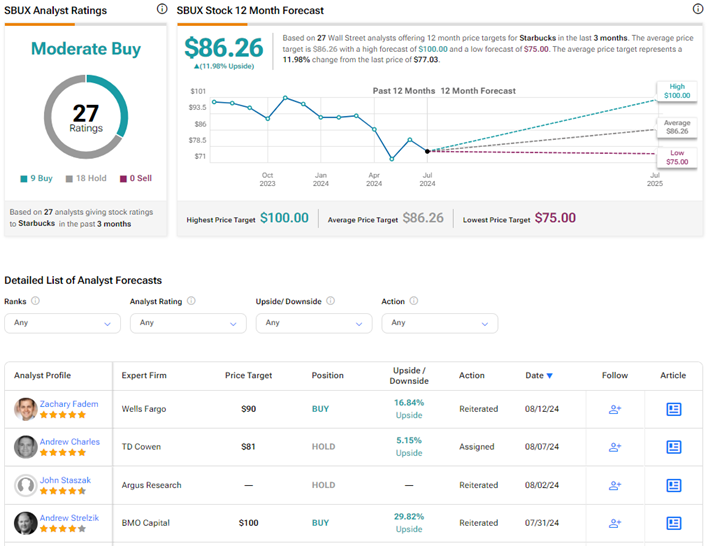

On the China growth strategy, analyst Andrew Charles of TD Cowen believes that the refranchising of Starbucks’ China business would be modestly dilutive to the company’s EPS. A tax-free spin-off of SBUX’s China business or refranchising to a Master franchisee would reduce management’s burden and help focus more on the U.S. markets. Charles has a Hold rating and $81 price target on SBUX stock, which implies 5.2% upside potential from current levels.

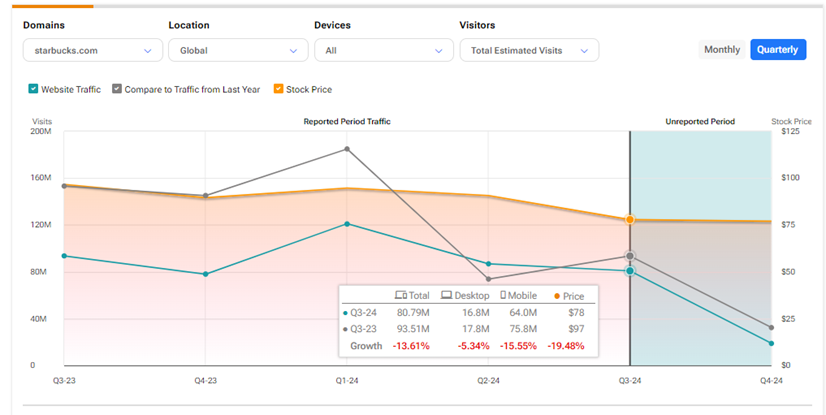

Website Traffic Hinted Sluggish Growth

According to TipRanks’ Website Traffic tool, the total estimated visits to all of Starbucks’ apps and websites worldwide fell by 13.61% in the third quarter compared to last year. The weak website footprint hinted at slowing growth for Q3, ahead of the results.

Is Starbucks Stock a Good Buy?

Wall Street remains divided on Starbucks’ growth trajectory. On TipRanks, SBUX has a Moderate Buy consensus rating based on nine Buys versus 18 Hold ratings. The average Starbucks price target of $86.26 implies nearly 12% upside potential from current levels.

Questions or Comments about the article? Write to editor@tipranks.com