Spotify stock (NYSE:SPOT) surged after the company posted strong Q4 results. However, extreme share price gains over the past year have resulted in Spotify’s valuation now raising eyebrows. On the one hand, the audio streaming company continues to display robust traction regarding user and revenue growth. Nevertheless, concerns emerge when examining the stock’s valuation in conjunction with Spotify’s narrow-margin business model. Thus, I am neutral on the stock.

Q4 Results: Excellent User Growth, Pricing Power Shine

While I like using Spotify, I am not a fan of the stock for reasons I’ll get into later. Still, I can’t deny I was pretty impressed looking at the company’s user growth and pricing power shown in its most recent Q4 results. Spotify’s user base growth is picking up speed again, and when you throw in its strong pricing leverage, it’s driving a reacceleration in revenue growth. Let’s examine.

In the fourth quarter, Spotify experienced a notable surge in monthly active users (MAUs), reaching an impressive 602 million — a 23% increase from the previous year. Notably, Premium MAUs saw a robust increase of 15%, reaching a total of 236 million, while ad-supported MAUs witnessed an even more substantial increase of 28%, reaching an impressive 379 million.

Comparing these growth figures to the same quarter in 2022, where the numbers stood at 20%, 14%, and 25%, respectively, it’s evident that Spotify’s user base is picking up.

Simultaneously, total revenues grew by 16% year-over-year to €3.67 billion (or 20% Y/Y in constant currency). This growth was led by:

- Premium revenue growth of 17% to €3.17 billion (or 21% Y/Y in constant currency).

- In turn, this was driven by subscriber growth of 15% Y/Y, as stated earlier, and Premium average revenue per user (ARPU) growth of 1% Y/Y to €4.60 (or up 5% Y/Y in constant currency), and

- Ad-Supported revenue growth of 12% year-over-year (or 17% Y/Y in constant currency), driven by growth across all regions.

Firstly, let me highlight the significance of the 16% surge in revenues, as it signals an uptick compared to the previous three quarters. Specifically, revenue growth clocked in at 14.3%, 10.9%, and 10.6% from Q1 to Q3, respectively. Hence, Q4 halted a trend of declining growth rates while potentially reinstating growth momentum that will revitalize the stock’s investment case.

Another important note to make is that Spotify demonstrated its pricing power. Despite the unfavorable impact of foreign exchange transactions on ARPU growth, the metric’s 5% increase in constant currency speaks volumes. It underscores Spotify’s ability to boost prices without hindering user growth, which, as mentioned, experienced an acceleration.

Don’t Trust the Margin Expansion Story Just Yet

Besides strong numbers, the most crucial catalyst that likely contributed to Spotify’s post-earnings surge is the margin expansion story the company is actively pursuing. Nevertheless, this is where my reservations begin to surface. I remain unconvinced by this narrative.

Why? Well, let’s start with its gross margin, which came in at 26.7% in Q4, marking a 140 basis points expansion compared to last year. Despite what appears to be a notable margin expansion, Spotify’s profit margins are still pretty slim, and they are destined to stay that way. This is because most of Spotify’s revenues go back to labels and artists.

The catch is that as Spotify’s user base expands, so do the royalties they have to dish out. Scaling up the user base won’t magically pump up their profit margins. While they managed a boost through higher pricing this time around, there’s a limit to how much they can jack up prices and stay competitive, especially with rivals like Apple Music in the mix.

Another highlight in Spotify’s results, which may initially seem like proof of its margin expansion story, is that its free cash flow came in at €396 million. This is the highest free cash flow Spotify has ever posted, marking a significant increase from last year’s negative figure of €73 million.

That said, the €396 million figure is likely highly misleading. It was artificially boosted by a €419 million increase in trade and other liabilities. In simpler terms, Spotify essentially deferred payments to its counterparts, creating a positive cash flow situation that might not be as rosy as it appears.

Finally, it appears that Wall Street was excited with Spotify’s Q1 guidance, which projects an operating income flow of €180 million. However, even if all of this converts into free cash flow, the annualized €720 million still falls short when compared to Spotify’s hefty market valuation of €47 billion.

This implies a P/FCF ratio of 65, which is, for me, impossible to justify, regardless of the assumed free cash flow growth rate over the next few years (be it 15%, 25%, or 35%).

While I can appreciate why investors are willing to pay a premium for Spotify’s stock due to its sticky business model, resilient cash flows, and potential for growth, it’s hard to envision the company growing into such an ambitious valuation multiple. Given the significant gross profit constraints inherent in its business model, I don’t believe the margin expansion story is the magic solution.

Is SPOT Stock a Buy, According to Analysts?

Turning to Wall Street, Spotify Technology has retained a Moderate Buy consensus rating based on 16 Buys, seven Holds, and one Sell. in the past three months. At $261.75, the average Spotify stock forecast suggests 8.7% upside potential.

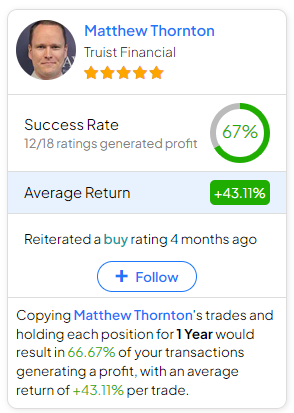

If you’re wondering which analyst you should follow if you want to buy and sell SPOT stock, the most profitable analyst covering the stock (on a one-year timeframe) is Matthew Thornton from Truist Financial, with an average return of 43.11% per rating and a 67% success rate.

The Takeaway

In conclusion, while Spotify’s Q4 results showcase commendable user growth and pricing power, I believe the surge in the stock’s valuation prompts caution. The notable increase in revenues and seeming margin expansion story may excite investors. However, if you take a closer look, it becomes evident that profit margins still remain thin, while the Q4 free cash flow figure is likely misleading. Therefore, I suggest that you exercise caution when evaluating Spotify’s prospects at its current price levels.