American Airlines Group Inc.’s (AAL) credit rating was cut to ‘B-‘ from ‘B’ at S&P Global on June 3 amid expectations that the U.S. airline will generate a “substantial” cash flow deficit this year due to the impact of the coronavirus pandemic.

The credit rating agency said that American Airlines’ steps to partly offset the steep decline in airline bookings through capacity reductions, cost savings, and liquidity initiatives, will be insufficient to offset the effects from the impact of the aviation crisis on the company’s credit metrics.

“We expect American’s operating performance and liquidity to continue to be negatively affected in 2020 due to the decline in airline passenger traffic because of COVID-19, with some recovery expected in 2021,” S&P credit analyst Betsy R Snyder wrote in the report. “We are maintaining our assessment of liquidity as less than adequate primarily due to our expectation of a substantially negative level of cash generation over the next 12 months.”

S&P sees American Airlines returning to positive cash flow in 2021 assuming that air traffic will start to recover in the second half of this year. The credit rating agency expects the U.S. airline to generate adjusted negative EBITDA of at least $2 billion in 2020 compared with positive EBITDA of $7.3 billion in 2019 and to return to positive EBITDA in 2021 of at least $4 billion.

American Airlines stock has lost almost two-third of its value so far this year as stringent travel restrictions tied to the coronavirus pandemic have brought travel demand to an almost halt. U.S. airlines have been burning through billions of dollars in the first quarter incurring huge losses and implementing broad cost-cutting plans, as well as taking steps to shore up its cash buffers.

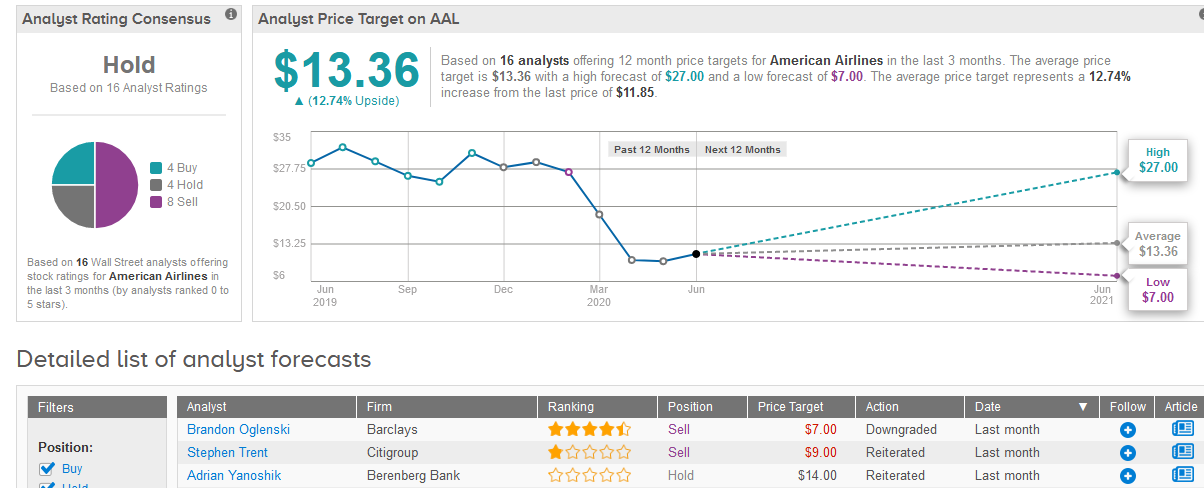

The airline’s stock advanced 5.6% to $11.85 as of Wednesday’s close.

Five-star analyst Brandon Oglenski at Barclays last month lowered the stock’s rating to Sell from Hold, with a $7 price target, (reflecting 41% downside potential) saying the future is uncertain on travel demand but definite on “plenty of additional debt.”

Overall Wall Street analysts are sitting on the fence when it comes to the stock’s outlook. The Hold consensus is divided into 4 Hold, 8 Sell and 4 Buy ratings. The $13.36 average price target is less bearish than Barclays’ outlook and implies 13% upside potential in the shares in the coming year. (See American Airlines stock analysis on TipRanks).

Related News:

Billionaire Investor Dan Loeb’s Fund Lists Boeing As Top Winner In May

Amazon Leases 12 Boeing Cargo Aircraft To Meet Online Orders Surge

TUI Strikes Compensation Deal With Boeing Over 737 MAX Jets