SolarEdge Technologies (SEDG) shares fell over 3% on Friday after a 16% surge on Wednesday that pushed the stock to its highest level in over five months. The initial rally was driven by better-than-expected Q4 revenues and a return to positive free cash flow, which was further helped by management’s confidence in being able to maintain a positive free cash flow figure in 2025. However, BMO Capital still ended up downgrading the solar company to Underperform.

This downgrade was due to the BMO’s concerns that SolarEdge’s core inverter and battery business remains far from meeting expectations. In addition, analyst Ameet Thakkar believes that the recent stock rally was largely driven by short-covering rather than a fundamental improvement in the company’s operations.

As a result, Thakkar now expects the narrative around SolarEdge to shift from near-term liquidity risks to the company’s operating earnings power, which he believes has been impacted by current market demand and the company’s cost structure. Therefore, despite the recent improvements, the analyst thinks that SolarEdge may not actually be able to achieve breakeven adjusted operating income until 2027 or 2028 on a GAAP basis, which led BMO to set a price target of $15 for the stock.

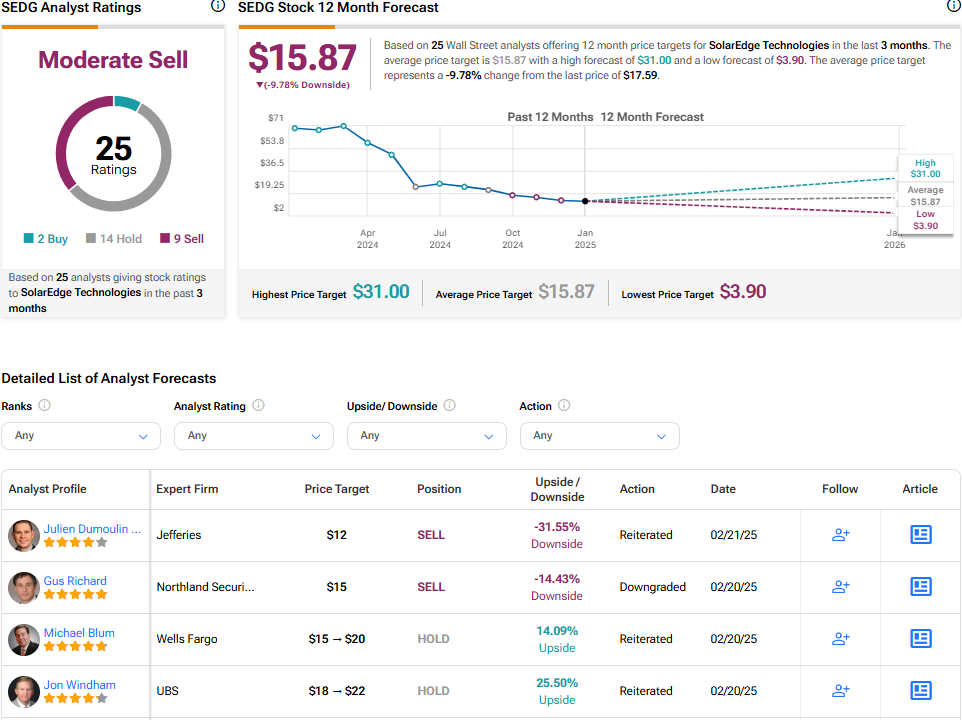

Is SEDG Stock a Buy or Sell?

Turning to Wall Street, analysts have a Moderate Sell consensus rating on SEDG stock based on two Buys, 14 Holds, and nine Sells assigned in the past three months, as indicated by the graphic below. After a 75% decline in its share price over the past year, the average SEDG price target of $15.87 per share implies 9.8% downside risk.

Questions or Comments about the article? Write to editor@tipranks.com