SoFi Technologies (SOFI) has experienced a dip due to an unfavorable 2025 outlook despite strong Q4 2024 earnings. However, the firm has diversified to ease risks associated with being solely a lender and is now generating further growth opportunities. SoFi is building a capital-light, low-risk revenue stream through its loan platform business, while its banking success and financial service products have significantly boosted the company’s efficiency.

Diversifying Revenue

SoFi, an all-digital U.S. bank, reported high sales and earnings increases, ending 2024 with 10.1 million members (a 34% increase) and 14.7 million products (a 32% increase). The company has diversified its offerings beyond its core lending segment to fuel growth and mitigate risks. Non-lending services for individual accounts grew 84% year over year in Q4 2024.

The loan platform business (LPB), which originates and services loans on behalf of third parties, is a growing revenue stream for the company. In Q4, $1.1 billion in third-party loan volume through LPB generated $63.2 million in fee income plus $3.6 million in servicing fees.

SoFi aims to become the go-to infrastructure provider for other companies’ fintech needs, primarily through its Galileo technology platform. Galileo-powered accounts grew by 15% to 168 million in 2024. Galileo secured several significant deals, including a partnership with the U.S. Treasury Department and a leading hotel rewards program.

A shift towards growth in the banking side of the business has led to increased SoFi Money customers (up by 51% in 2024), creating a more efficient business structure. While the number of personal loans grew at half the rate, the growth in financial services creates a natural marketing funnel for SoFi’s loan products. The current ratio of financial services products to loans is 6.3-to-one, indicating potential for improved efficiency in customer acquisition.

Analysts Response Mixed

SoFi showcased a robust financial performance in Q4 and full-year 2024. The GAAP net revenue for Q4 was $734.1 million, reflecting a 19% hike from the previous year. Meanwhile, the full-year net revenue stood at $2.7 billion, a 26% increase from the preceding year. Fee-based revenue also saw significant growth, with Q4 reporting a 63% increase year-over-year and the full-year figure recording a 74% surge.

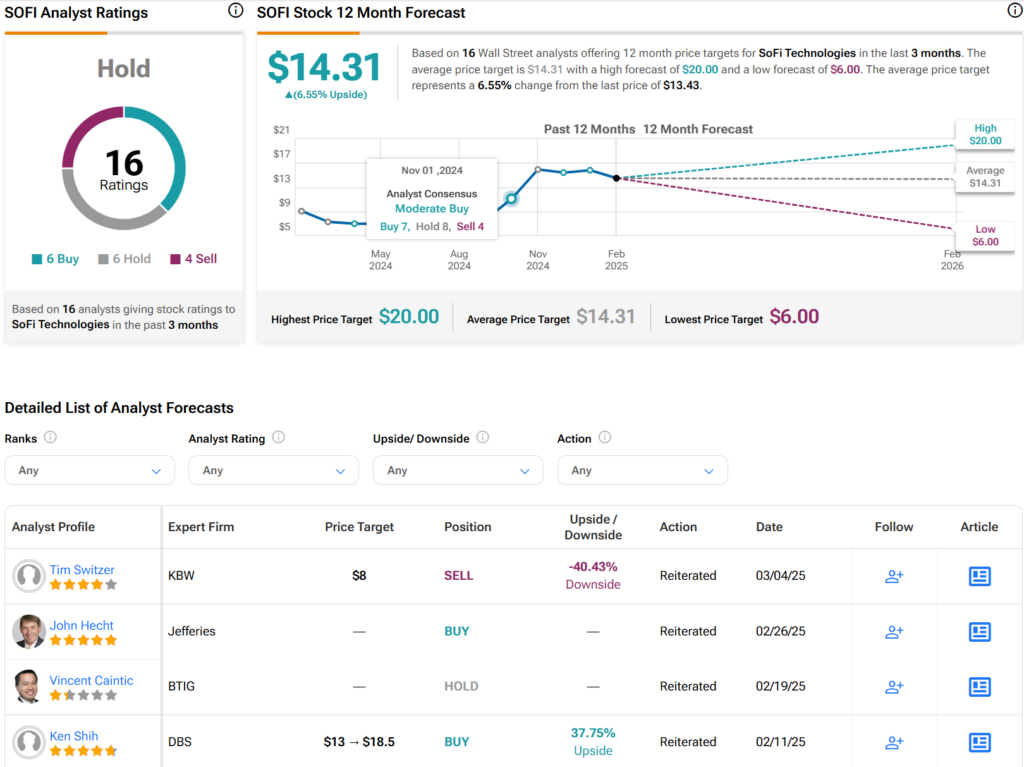

Analysts following the company have had a mixed response to the most recent earnings. SoFi Technologies is rated a Hold overall, based on the recent recommendation of 16 analysts. The average price target on SOFI stock is $14.31, which represents a potential upside of 6.55% from current levels.