Shares of Sofi Technologies (SOFI) have been on an absolute tear, skyrocketing 152% over the past six months alone. With such massive gains, it’s easy to wonder: Is this a bubble waiting to pop? Honestly, I don’t think so. In fact, I’d argue the opposite. SoFi Technologies is in the middle of a major growth surge. The fintech powerhouse has seen its revenue growth accelerate, its margins expand, and its earnings potential ramp up big time. So, while the stock has already delivered jaw-dropping returns, there’s a solid case for why the party isn’t over just yet.

SOFI’s Revenue Growth Picking Up Pace

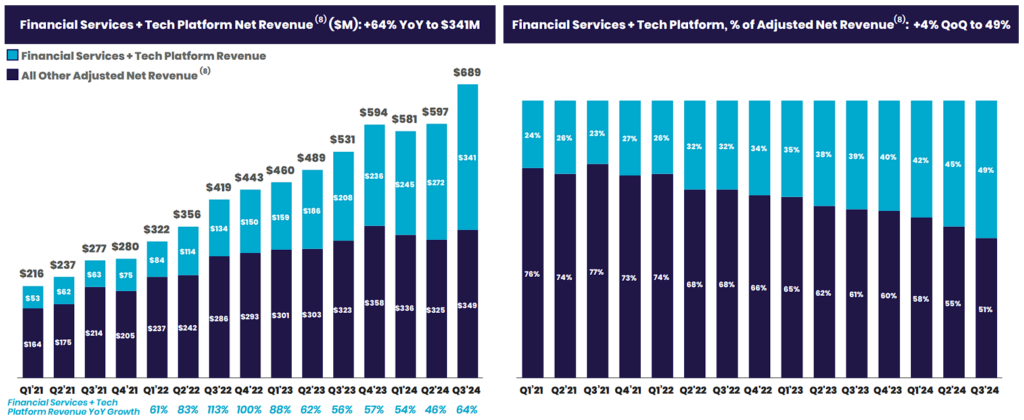

To illustrate SOFI’s tremendous momentum lately, which has been the most significant catalyst supporting my bullish outlook, let me start with its top-line numbers, which are truly impressive. In Q3, SOFI’s net revenues hit a record $689 million, marking a 30% jump compared to last year. This marked a notable acceleration from the 22% growth in Q2 and 27% last year. Once again, the most valuable players were SOFI’s financial services and tech platform segments. Together, they saw a massive 64% revenue boost year-over-year, and these two areas now make up nearly half of SOFI’s total sales, up from about 39% a year ago.

I believe that this shift in the revenue mix reflects SOFI’s ongoing transition from being heavily reliant on lending to a more balanced, fee-based, and capital-light business model. The financial services segment alone posted a staggering 102% revenue increase, supported by growth in high-yield savings accounts, credit cards, and its evolving loan platform, which connects borrowers with third-party lenders. Further, the fact that SOFI continued to attract customers played a pivotal role. Specifically, SOFI added 756,000 new members in Q3, bringing its total membership to 9.4 million—a 35% year-over-year boost.

But beyond acquiring new members, SOFI once again excelled at deepening engagement with its existing customers. For example, its innovative one-stop-shop model encourages “cross-buying,” where members who join for one product, like a personal loan, are offered others, such as investment accounts or credit cards. This strategy led to 32% of new products in Q3 being opened by existing members. Also, 20% of new members added a second product within 30 days of joining, essentially boosting growth by increasing monetization per member with minimal incremental promotional spending.

Margins Keep Climbing

Let’s now shift gears toward profits, where things get really interesting and further bolster my bullish view on SOFI stock. Its adjusted EBITDA margin hit 27% in Q3, up from 23% in the previous quarter and 18% a year ago. That kind of margin expansion in a single year is no small feat. The fact that this is occurring during a period of accelerating growth, which could imply increased promotional spending and, thus, declining margins, is particularly noteworthy. It’s certainly a sign that SOFI is becoming more efficient, too. Hence, SOFI’s adjusted EBITDA rose 90% year-over-year to $186 million, outpacing revenue growth.

As I briefly mentioned earlier, one major factor fueling this margin expansion is SOFI’s shift toward fee-based and capital-light revenue streams. These include loan referral fees and interchange income from SOFI’s credit cards, which are essentially frictionless, high-margin cash flows. In fact, fee-based revenue grew 65% year-over-year, now making up 25% of SOFI’s adjusted net revenue and reaching a run rate of nearly $700 million. This trend suggests that SOFI’s lofty Q3 margin doesn’t represent a one-off benefit but a revenue mix development here to stay and benefit the company for a long time.

Valuation Is Not as Pricey as It Looks

SOFI’s revenue and profits are both thriving, but after a 151% surge in six months, it’s natural to question whether SOFI stock has become too expensive. I don’t think this is the case, as recent analyst revisions suggest otherwise. Over the past six months, Wall Street’s consensus EPS estimate for 2024 has risen by an impressive 55%. SOFI is expected to post $0.13 in EPS this year, climbing from last year’s losses. And that’s just the start, as analysts expect EPS to grow by 112% in 2025 to $0.28 and another 69% in 2026 to $0.47 per share.

So, while SOFI stock trades at 58 times next year’s anticipated earnings, which sounds high at first glance, the strong earnings growth SOFI is achieving makes that multiple appear more reasonable. I view the valuation as a reflection of SOFI’s earnings growth potential rather than a red flag. Accordingly, the stock’s bullish momentum could have more fuel in the tank.

Is SoFi Stock a Buy or Sell?

Despite their aggressive earnings growth estimates, Wall Street analysts appear more cautious regarding SOFI’s actual share price prospects. Specifically, SOFI stock now has a Hold rating among 14 Wall Street analysts who cover the company. This is based on five Buy, six Hold, and three Sell recommendations assigned in the past three months. The average price target on SOFI stock of $11.46 suggests a downside potential of 32.1%, contrasting my bullish outlook.

If you’re wondering which analyst to follow concerning SOFI stock, the most accurate and most profitable analyst (on a one-year timeframe) is Dan Dolev from Mizuho Financial Group (MFG), with an average return of 33.74% per rating and a 74% success rate.

Summing Up

Summing up, it looks like SOFI is firing on all cylinders. Its accelerating revenue growth, driven by a shift to fee-based, capital-light streams, exhibits a positive business model evolution. Meanwhile, expanding margins and impressive earnings potential highlight its operational efficiency. Therefore, although the stock has surged significantly, the current valuation seems to reflect SOFI’s outstanding trajectory rather than market exuberance, implying the potential for further gains ahead.