It has been an inauspicious start for many stocks in 2024, with several of 2023’s highflyers on the backfoot during the year’s opening sessions.

SoFi Technologies (NASDAQ:SOFI) is a good example. The shares might have more than doubled during 2023 but have already shed 15% since 2024 entered the frame.

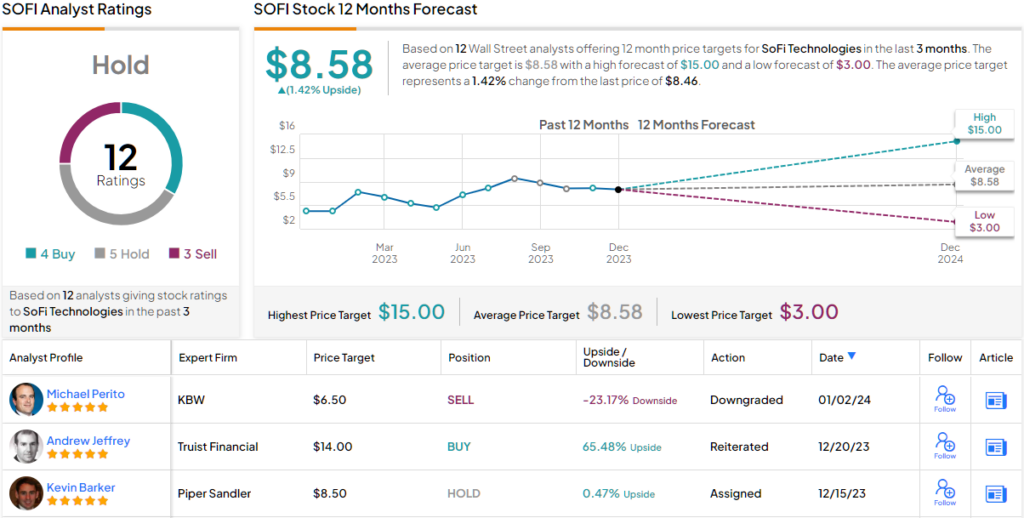

Most of that drop came in Wednesday’s session in the wake of a downgrade from KBW’s Mike Perito. The 5-star analyst reduced his rating from Market Perform (i.e., Neutral) to Underperform (i.e., Sell) and lowered the price target from $7.50 to $6.50. Even after the recent decline, that figure is still 23% below the current share price. (To watch Perito’s track record, click here)

Perito’s downbeat assessment is partly based on the stock’s show of strength, with the shares outperforming since the neobank’s Q3 print, and thereby making its valuation unreasonable. But it also factors in a less appealing outlook than before.

Primarily due to slower origination growth and technology revenues, Perito has lowered his 2024 revenue and adj. EBITDA expectations from the prior $2.4 billion to $2.3 billion and from $499 million to $492 million, respectively. These new figures are about -10%/-17% below consensus estimates.

Perito also thinks the perception that SOFI stands to gain from a lower rate environment is wrong. Since the Fed meeting on December 13 suggesting rate cuts were possible in 2024, the stock had participated in the “broader risk-on relief rally” but while Perito believes rate relief and a steeper curve will overall be a positive for the banking/fintech sectors, in SOFI’s case, its “unique loan accounting positions them differently.”

“With >100% betas on coupon rates per the company disclosures on the way-up, we believe there is risk for lower coupon rates to work against fair value marks in 2024 should rate cuts materialize,” the 5-star analyst explained. “While the company has some pricing power given their near 25% market share of super prime personal lending, the company’s earnings and capital position is heavily levered to the cumulative fair value adjustments, and any downward pressure on marks could be a significant earnings/capital headwind.”

And even though Perito thinks achieving (and sustaining) profitability in 4Q23/2024 is not out of the question, the analyst sees more “downside scenarios to this outcome than upside,” which combined with a premium valuation, results in Perito taking a “more cautious stance.”

Amongst Perito’s colleagues on Wall Street, 2 others join him in the bear camp and with an additional 4 Buys and 5 Holds, the stock receives a Hold consensus rating. At $8.58, the average target makes room for only modest gains of 1.42% in the year ahead. (See SoFi stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.