The ongoing distraction caused by trade wars due to tariffs imposed by the Trump administration is weighing on growth stocks. Also, competition from China’s DeepSeek and concerns about a possible reduction in spending are also impacting growth stocks that gained in 2024 from the optimism about the AI (artificial intelligence) boom. However, several growth stocks are expected to navigate the ongoing challenges and deliver solid performance with strong execution. Using TipRanks’ Stock Comparison Tool, we placed Super Micro Computer (SMCI), Tesla (TSLA), and Micron Technology (MU) against each other to find the best growth stock, according to Wall Street analysts.

Super Micro Computer (NASDAQ:SMCI)

Super Micro Computer, a provider of application-optimized server solutions, continues to see significant volatility in its stock due to broader factors like tariffs and company-specific news. SMCI stock has declined 67% in the past year but has risen about 22% so far in 2025.

SMCI gained popularity as investors consider it to be one of the major AI plays. However, the stock was under pressure last year due to accusations by short-seller Hindenburg Research, growing competition, accounting issues, the delay in the filing of financial statements, and the threat of a delisting from the Nasdaq exchange. The company recently became current with its SEC filings.

Looking ahead, SMCI is now focused on boosting the demand for its block liquid-cooled solutions for AI factories and the HPC (high performance computing) market. It has announced plans to establish a third campus in Silicon Valley to expand its U.S. manufacturing capacity.

Is SMCI Stock a Good Buy?

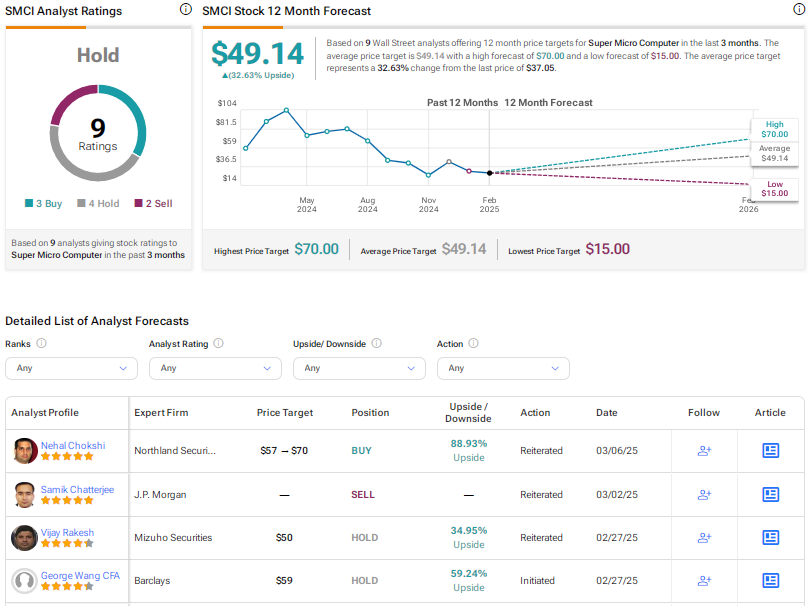

Recently, Mizuho analyst Vijay Rakesh reinstated a Hold rating on SMCI stock with a price target of $50. The analyst noted that the company regained compliance with Nasdaq with the filing of its 10-K and 10-Q filings. Rakesh feels that while SMCI avoided delisting, the company still needs to work on its internal controls. He added that the outlook for calendar year 2025/26 looks positive with Nvidia (NVDA) liquid cooling NVL72+ racks. He also expects the company’s liquid cooling business to ramp up to 30% in the near term with Blackwell deployments.

Overall, Rakesh believes that Super Micro Computer is well positioned with “priority allocation for Enterprise/sovereign NVL72+ racks” in 2025. However, he stated that this growth expectation is already priced into SMCI stock’s valuation. Plus, the company is facing a more competitive landscape with rivals like Dell Technologies (DELL) and Wistron.

Overall, Wall Street is sidelined on Super Micro Computer stock, with a Hold consensus rating based on three Buys, four Holds, and two Sell recommendations. The average SMCI stock price target of $49.14 indicates 32.6% upside potential.

Tesla (NASDAQ:TSLA)

Tesla stock has declined about 35% so far this year, reflecting concerns about the slowdown in EV (electric vehicle) demand, intense competition, margin pressures, and CEO Elon Musk’s political activities under the Trump administration. In fact, on Thursday, TSLA stock plunged about 6% as analysts at Baird slashed the price target to $370 from $400, saying that Musk’s involvement with the Trump administration “adds uncertainty to the demand-side” and raises concerns about the Q1 delivery outlook.

Notably, recent data has indicated that Tesla has been losing market share in key markets like China and Europe. There have also been worries about the lack of innovation, especially amid intense rivalry from emerging players.

Despite multiple pressures, Tesla bulls continue to be optimistic about the company’s full self-driving tech, Cybercab robotaxis, and Optimus robotic humanoid.

Is TSLA a Buy, Sell, or Hold?

Earlier this week, Goldman Sachs analyst Mark Delaney lowered the price target for Tesla stock to $320 from $345 and reiterated a Hold rating. The analyst reduced his below-consensus delivery estimates for Tesla to reflect the quarter-to-date data for key regions like China, Europe, and the U.S. and the broader demand trends, including data from consumer surveys from HundredX.

Delaney believes that FSD v13 (the latest version of the full self-driving tech) has shown meaningful improvement from v12, which he thinks would drive better monetization in the U.S. over the medium to longer term. That said, the analyst noted that multiple Chinese rivals are also offering hands-free ADAS (Advanced Driver Assistance System) solutions without the need to purchase an incremental software package. Consequently, Delaney thinks that Tesla will have a tough time monetizing FSD in China, especially if it continues to require driver supervision.

With 14 Buys, 11 Holds, and 10 Sell recommendations, Tesla stock scores a Hold consensus rating. The average TSLA stock price target of $351.48 implies 33.4% upside potential.

Micron (NASDAQ:MU)

Micron is one of the leading providers of memory and storage solutions, including high-performance DRAM, NAND, and NOR memory products. The AI boom has created robust demand for high bandwidth memory (HBM) solutions. AI workloads require servers having GPUs with larger and faster memory, creating solid growth opportunities for Micron’s offerings.

In December, MU stock plunged as the company’s Q1 FY25 earnings beat was overshadowed by a dismal guidance for the fiscal second quarter. Micron cautioned that it is seeing slower growth in some parts of the consumer devices market and witnessing “inventory adjustments.” However, the company is confident about leveraging AI-driven opportunities. MU’s data center revenue jumped 400% in Q1 FY25, mainly due to AI-led demand.

At a Wolfe Research conference held last month, CFO Mark Murphy reaffirmed the second-quarter outlook but cautioned investors about a sequential decline in Q3 gross margins due to a shift in the customer mix and broader industry pressures. However, he added that the Q3 might be the bottom for margins due to improving business conditions.

Micron is scheduled to announce its results for the second quarter of Fiscal 2025 on March 20. Wall Street expects the company’s EPS (earnings per share) to jump 243% year-over-year to $1.42, with revenue projected to grow 36% to $7.9 billion.

Is Micron a Good Stock to Buy?

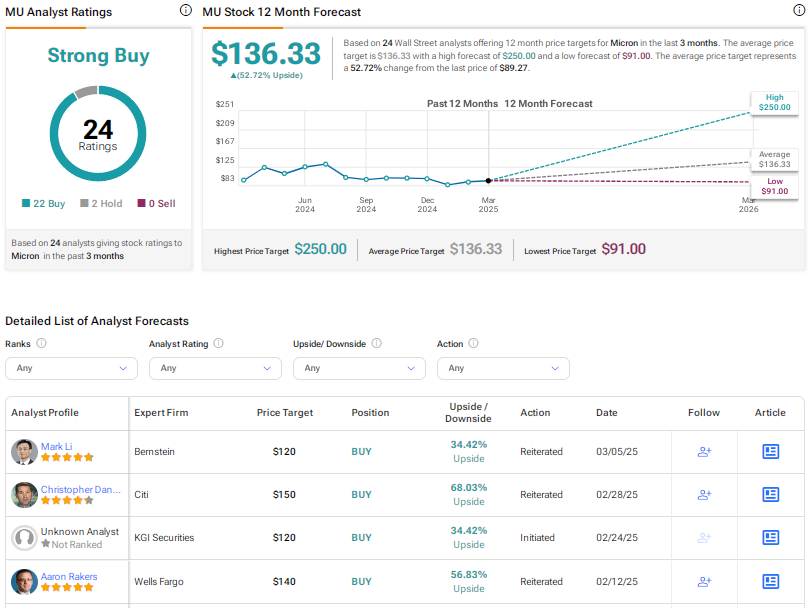

Following Micron’s warning about the Q3 gross margin, Wells Fargo analyst Aaron Rakers reiterated a Buy rating on MU stock with a price target of $140. Despite the weak gross margin outlook, the analyst noted that Micron still anticipates an increase in bit shipments and revenue growth. Rakers thinks that this indicates resilience in the company’s operational strategy, even amid weak NAND industry conditions.

Rakers highlighted that Micron sees improvement in the second half of the year as better industry conditions are expected to enhance margins. He stated that the company is making notable progress in the HBM sector, with plans to boost 12H stack production, which could contribute positively to its financial performance. These positives, coupled with stable DRAM data center demand, reinforce Rakers’ optimistic outlook for Micron stock.

With 22 Buys and two Holds, Wall Street has a Strong Buy consensus rating on Micron stock. The average MU stock price target of $136.33 implies about 53% upside potential from current levels. MU stock has risen about 6% year to date.

Conclusion

Wall Street is highly bullish on Micron stock but sidelined on Super Micro Computer and Tesla due to the ongoing challenges. Analysts see higher upside potential in Micron stock than in the other two growth stocks, backed by robust demand for its memory solutions amid the ongoing AI wave.