In the road race to build out the electric vehicle (EV) future, the Lucid Group (NASDAQ:LCID) is working to carve out a niche as a top-end producer of luxury vehicles and cutting-edge technology. The Lucid Air, in particular, has earned rave reviews and was even named Motor Trend’s Car of the Year in 2022.

While industry plaudits are wonderful, the real question for investors is whether the company can accelerate into sustainable profits. On this plane, the current road remains a bit bumpy for the American EV maker. The company burned through roughly $950 million last quarter alone, with almost $2.4 billion in losses in the first nine months of the year.

All told, shares are down almost 30% in 2024 amidst concerns over shareholder dilution (the share count has practically doubled since 2021) and the mounting losses. Still, the luxury EV maker can point to its improving delivery numbers (up 91% year-over-year), a massive influx of cash from Saudi Arabia’s PIF, and, of course, its technological advantages, such as best-in-class mileage per gasoline-equivalent.

Though acknowledging Lucid’s top-of-the-line tech, top investor Gary Alexander is worried that the company will not be able to keep up with the competition when it comes to the greater EV-buying public.

“Investors should be warned that Lucid’s mass-market product will lag behind its major rivals,” writes the 5-star investor, who sits in the top 1% of TipRanks’ stock pros.

To that end, Alexander casts doubt on whether Lucid’s technology will be enough to help it succeed in making inroads with the masses. The investor continues that technological superiority will be far less important to most consumers, who are more interested in an affordable price tag.

Alexander cites mass-market offerings from other EV makers, such as Tesla’s Model Q (scheduled for launch next year) and Rivian’s R2 vehicles (expected to arrive in early- to mid-2026). In contrast, Lucid’s high-volume, mid-sized vehicle is only expected to arrive in late 2026.

Another red flag for Alexander is Lucid’s runway, and whether or not the company has enough cash on hand to see it through to profits.

“Despite the appearance of billions on its current balance sheet, Lucid isn’t sufficiently capitalized to support its goals and will likely have to raise additional dilutive capital next year,” adds the investor.

Though a major partnership or licensing deal could change the investor’s bearish view, Alexander currently rates LCID a Sell. (To watch Alexander’s track record, click here)

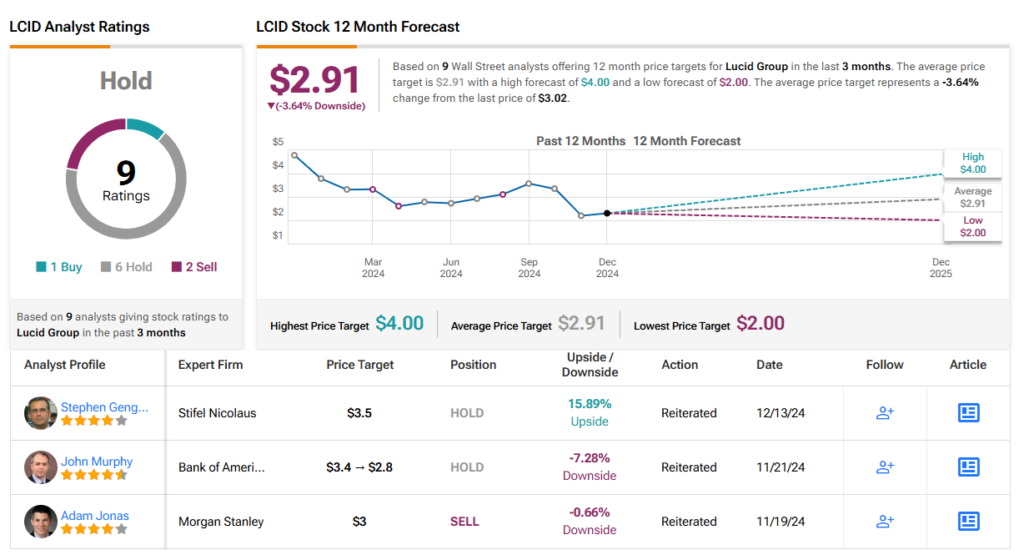

Optimism does not exactly abound on Wall Street either. With 1 Buy, 6 Hold, and 2 Sell ratings, LCID holds a consensus Hold (i.e. Neutral) rating. Its 12-month average price target of $2.91 implies minimal downward movement of ~3.6%. (See Lucid stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.